NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Whilst President Trump was self-aggrandising at Davos, US equities stalled.

https://soundcloud.com/user-291029717/trump-talks-it-up-but-equities-stall?in=user-291029717/sets/the-morning-call&

When something caught his eye he’d measure his need, And then very carefully he’d proceed – Bruce Springsteen

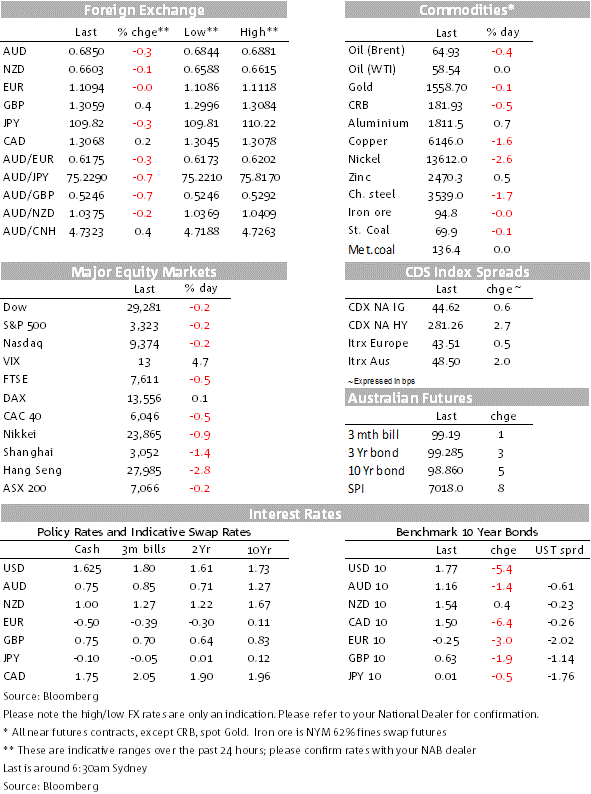

Market sentiment has turned mildly negative as investors become cautious following news of growing spread of a SAR-like virus. European equities indices ended the day with small declines and after initially treading water, US equities have turned south later in the session on the back of reports of a virus case in the US. The risk off mood has triggered a rally in core global bonds with UST yields leading the decline while in FX, JPY is one the outperformers, reflecting its safe have attributes. GBP is the other outperformer after a better than expected labour market report. AUD is down 0.3% to 0.6844 and NOK (-0.58%) remains under pressure amid domestic political uncertainty.

After initially showing some resilience, US equities have turned decisively negative following news reports of a virus case in the US. The news broke out around the same time as President Trump’s impeachment trial formally opened in the Senate, but with an eventual acquittal almost a sure thing, is probably safe to say that the dampening in the market’s mood is largely due to concerns over the risk of a new deadly coronavirus outbreak.

China has confirmed more than 300 cases of the virus, including six deaths, and there is the potential for further spread of the virus as people travel for Chinese New Year. While it is still early days, there is a risk that any outbreak could depress consumer sentiment and spending, including tourism as well as travel and transport related business. Asian equity markets fell yesterday on the back of these reports, with the Hang Seng dropping 2.8% and the Shanghai Composite down 1.4%. The CNY fell 0.6%.

Back in 2002/3, according to the World Health Organization (WHO), the outbreak of SARS in southern China caused an eventual 8,098 cases, resulting in 774 deaths reported in 37 countries, with the majority of cases in China and Hong Kong (9.6% fatality rate). In addition to the sad and devastating human cost, the epidemic also had an economic impact with epicentres such as Hong Kong enduring a short lived recession. This time the epicentre is in China, so the economic growth impact could be more severe and thus this is certainly a theme to watch for markets.

The risk-off mood has a triggered a demand for traditional safe haven assets with a rally in core global bond yields led by a move lower in UST yields. The 10y UST note is down 5.2bps to 1.7691% while 10 Bunds closed 3bps lower at -0.2480%.The move also triggered a bull flattening if the UST curve with the 2y10y slope down 3bps to 23.84 bps.

True to form, JPY has been the major beneficiary from the risk off mood in FX land, aided by the move lower in UST yields and pull back in equity markets. USD/JPY now trades at ¥109.84, 0.33% lower. GBP is also the other notable USD outperformer with cable up 0.30% to 1.3047 following a better than expected labour market report. The employment growth was much higher than expected (Employment change 3m/3m, Nov: 208k vs. 110k exp.), leaving the unemployment rate at its lowest level since the mid-1970s (3.8%).The market pared back its probability of a BoE rate cut next week to 60%, from 70% previously. That said, worth noting here that the labour market figures are for November, thus before the election and renewed Brexit concerns post Bojo’s re-election. The January services PMI out on Friday is the one to watch ahead of the BoE rate decision later in the month. The EUR reversed earlier gains it made after the upside surprise to the ZEW and is back to unchanged on the day, just below 1.11.

The AUD has fallen 0.33% over the past 24 hours to 0.6845. The underperformance of the AUD may be related to concerns that the Australian economy is vulnerable to further spread in the coronavirus, given the close economic relationship with China. One man was placed in quarantine in Brisbane yesterday, after recently returning from Wuhan, although health authorities later said he wasn’t a risk to the public. The move in the AUD is still small in magnitude, but given concerns over how dangerous the virus is and the rapid rise in cases, the AUD is likely to remain under pressure as China’s equity market and CNY are likely to struggle.

AUD losses have been comfortably eclipsed, by NOK (-0.58%) which has extended yesterday’s decline on a combination of lower oil and the Norwegian government’s loss of its majority after its Populist coalition partner quit over the repatriation of an ISIS member’s wife to Norway.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.