Coming in for landing in a heavy cross wind

Insight

The markets were spooked overnight by threats of further tariffs from the US President if a trade resolution isn’t reached.

https://soundcloud.com/user-291029717/trump-threatens-more-tariffs-as-chinas-manufacturing-grows-us-slows?in=user-291029717/sets/the-morning-call

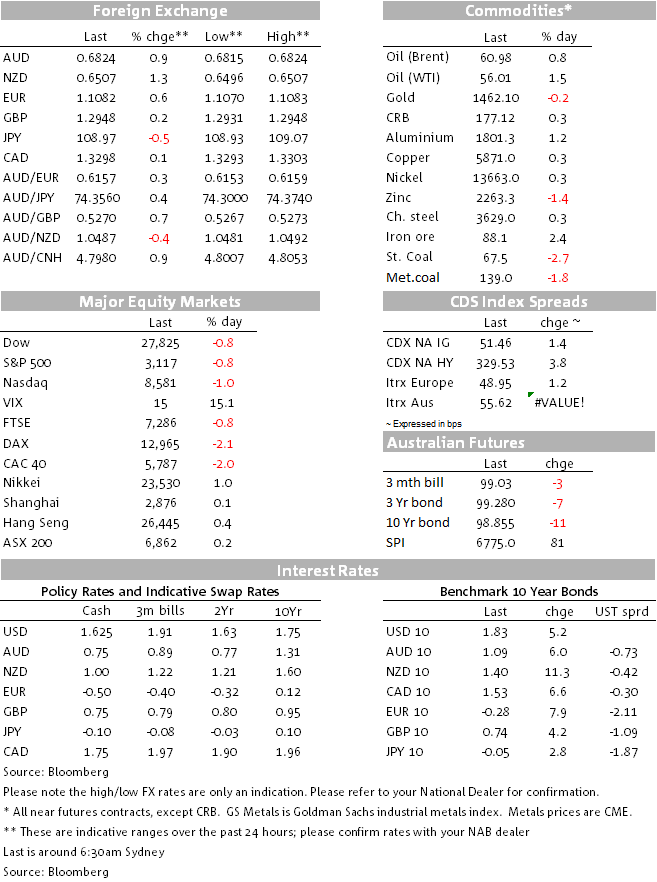

Volatility returned to markets with better than expected global PMIs juxtaposed by a weak US ISM Manufacturing print – the former suggests global manufacturing may be stabilising, the later suggests US growth outperformance is ebbing. Add to the mix President Trump tweeting the removal of tariff exemptions for Brazil and Argentina, and a reminder to markets that the US isn’t bluffing about further tariffs on China if an interim deal is not agreed to and you get volatility. No surprises then to see global yields higher on the global PMIs with US 10yr yields +5.7bps to 1.83% and German 10yr yields +7.9bps to -0.28%. Equities in contrast are lower with the S&P500 -0.6%, spooked by tariffs, the ISM and selling in the tech sector from momentum funds. FX took its cue from the better global PMIs and a notion that US growth outperformance is ebbing with the USD (DXY) -0.4% to 97.89. The big gainers were the NZD (+1.3% to 0.6506, fiscal stimulus helping), AUD (+0.8% to 0.6819, better China PMIs) and EUR (+0.5% to 1.1075). Other major pairs saw more moderate moves with GBP +0.1% and USD/Yen -0.5% to 108.99.

First to the global PMIs. The JPMorgan global manufacturing PMI composite posted a seven-month high of 50.3 in November, moving above the 50 line dividing expansion from contraction for the first time since April. Throughout the Asian time zone yesterday a string of better than expected PMIs had the markets thinking whether the global manufacturing downturn was starting to bottom. It kicked off first with the China’s Caixin PMI which came in at 51.8 against the 51.5 consensus and 51.7 previously. The rise took the index to its highest since December 2016 and followed the surprising bounce in the official manufacturing PMI on the weekend. Yields moved sharply higher at the get go with US 10yr yields climbing some 8.1bps initially to hit a peak of 1.86%, before paring moves after a weaker than expected US ISM Manufacturing report; 10yr yields in the end are up 5.7bps to 1.83%.

The weaker than expected US ISM manufacturing report had little impact on rates, though for FX it did open up the question of whether US data outperformance was likely to continue. The ISM itself was 48.1 against 49.2 expected and 48.3 previously, making it the fourth straight month below the 50 level. The key New Orders index fell to 47.2 from 49.1 and suggestive that activity could weaken further in the months ahead. Nevertheless the index is still consistent with GDP growth of around 1.5%. The Atlanta Fed GDP Now for Q4 was shaved to 1.3% from 1.7% following the data. More worrying for the outlook, the ISM Institute states: “Even if the tariff issue gets resolved, people aren’t going to want to make investments, because they don’t know whether the tariff issue can come back. So people are going to wait now for the election period, and make some decisions after that“. If that were to play out and businesses were to be on hold until after the election, that likely sets up the coming year to be very subdued.

Business seems to be correct in their view that “they don’t know whether the tariff issue can come back”. President Trump overnight removed tariff exemptions on steel and aluminium imports from Brazil and Argentina. Trump justified the move by stating “Brazil and Argentina have been presiding over a massive devaluation of their currencies. which is not good for our farmers”. Given Brazil was seen as a close friend of Trump and even they could not be exempt from tariffs, there is a notion that every country regardless of what they do could have tariffs imposed, which creates a lot of uncertainty of businesses. In reality the imposition of tariffs will likely push Brazil and Argentina closer to China and it is worth noting Brazil shipped 10 times the value of steel/iron products sold to the US in farm products to China.

On US-China trade there was little in new development, though Wilbur Ross told Fox news that the US wasn’t bluffing and that “if nothing happens between now and then, the president has made quite clear he’ll put the tariffs in – the increased tariffs.”. China has also said it would put in place retaliatory measures if the US passes a bill related to its Xinjiang province – the editor of the Global Times noted “Source told Global Times that China will release an “unreliable entity list” soon, which includes relevant US entities. US House is expected to pass a Xinjiang-related bill that will harm Chinese firms’ interests, prompting China to speed up the move.”

Trump also called on the Fed to lower the USD: “The Federal Reserve should likewise act so that countries, of which there are many, no longer take advantage of our strong dollar by further devaluing their currencies”. We have noted previously there is little Trump could do directly given the size of Treasury account.

FX moved sharply following the ISM with the USD (DXY) down -0.4% to 97.83. The main driver here being the notion of US outperformance ebbing – for some time we had been emphasising the US economy was the least dirty t’shirt in the global laundry basket and even if you thought the USD was overvalued. We will have to see how the US data flow plays out relative to the rest of the world in the coming months to see whether this assumption has truly changed.

In terms of moves the biggest mover was the NZD, +1.3% to 0.6506. Increased prospects of major fiscal stimulus in NZ was the initial driver, and as my BNZ colleagues note fiscal stimulus should reduce the risk that the RBNZ needs to cut the cash rate for domestic reasons. The AUD/NZD cross also moved lower by -0.4% to 1.0491 with fundamentals supportive of the kiwi outperformance with NZ commodity prices having risen by around 11% in NZD terms, while Australian commodity prices have fallen by 11.5% in SDR terms.

Other big movers were the AUD, +0.8% to 0.6819, initially driven by the better than expected Chinese data and then boosted by USD weakness after the ISM. The Euro also rose with EUR +0.55 to 1.1075. Over the past couple of days the possibility of German fiscal stimulus has gained some traction given two grass-roots leftist members of the junior ruling coalition party were elected as co-leaders. German economy should also benefit should global manufacturing conditions be stabilising given German exports make up around 47% of German GDP.

Weaker than expected Australian data had little enduring impact on markets. Residential building approvals declined in October by 8.1% against expectations of a mild decline after last month’s 7.2% bounce. Importantly for the outlook total approvals are now 23.6% lower than a year ago and point s to further declines in residential construction ahead. ANZ Job ads fell -1.7%, while Q3 profits were worse than expected along with inventories. For Q3 GDP on Wednesday though, the change in inventories will make a modest 0.2ppt contribution. Overall the partials to date suggest the private sector is weaker than expected and points to downside risks to the RBA’s Q3 implied GDP forecast of 0.6-0.7% growth q/q.

A big day domestically with the last of the pre-GDP partials of Net Exports and Government Spending, while the RBA also meets. It is likely to be quiet internationally, though President Trump’s visit to the UK has the potential to create headlines given the proximity of the UK elections:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.