Total spending grew 0.9% in June.

Even an executive order declaring more sanctions against Iran did little to influence markets.

https://soundcloud.com/user-291029717/trump-warns-iran-lowe-warns-against-global-monetary-easing?in=user-291029717/sets/the-morning-call

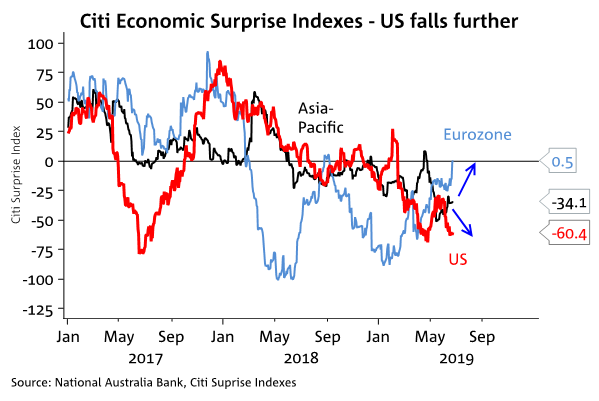

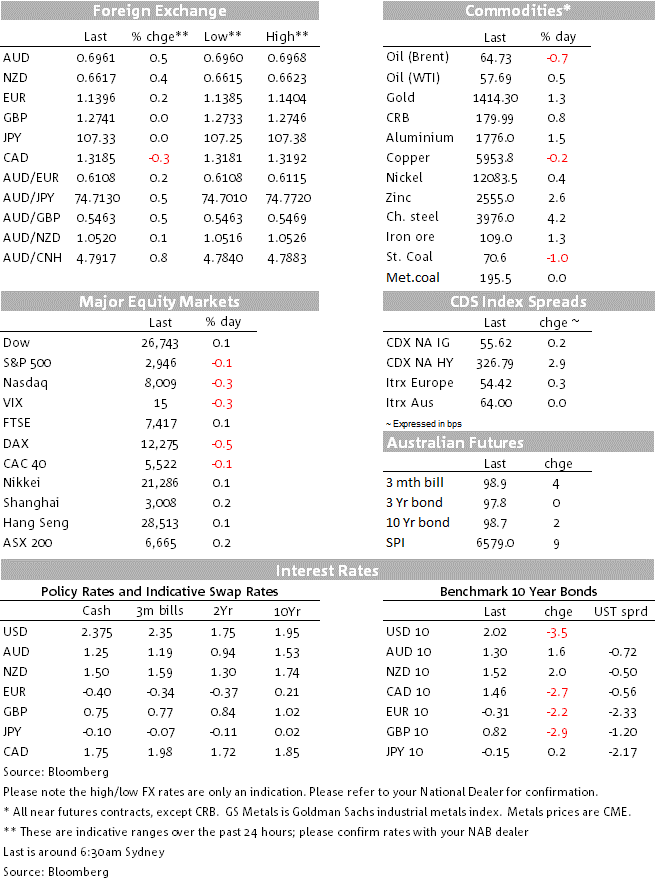

The USD decline remains the dominate theme with DXY -0.2% overnight to 95.983 (if it continued today, the dollar will have its fifth consecutive daily decline). The decline is also inspiration for today’s song title, “Way Down we Go” by Kaleo. The USD DXY is now looking it like will break through the March low of 95.76 and below there 95.0. The drivers here continue to be heightened expectations of the Fed cutting rates (now 3.1 cuts priced by years’ end), while data surprise indexes show the US data flow is now disappointing more than for Europe (see Chart below). One word of caution though remains that both EUR and GBP could struggle to break ranges amid continued Brexit uncertainty and trade headwinds (note German exports make up 47% of German GDP compared to 12% in the US and 14% in Japan). Overnight EUR was +0.2% to 1.1396 while GBP was flat at 1.2741. The outperformer in the USD weakness play remains Gold which is up some 12% since early May and closing above $1,400 an ounce for the first time since 2013.

AUD was one of the bigger movers overnight, up +0.5% to 0.6961 after following RBA Governor Lowe’s warning that the AUD might not fall with rate cuts due to a global easing cycle: “But if everyone is easing, there is no exchange-rate channel” “We trade with one another, we don’t trade with Mars, so if everyone’s easing, the effect that we get from exchange-rate depreciation via the transmission mechanism isn’t there.” Lowe continues to jawbone the government into greater fiscal spending given there are limits to monetary policy. While the AUD rose, the comments did not greatly affect pricing for a July cut; markets now price a July cut at an 89% chance with 2.1 cuts fully priced by the end of the year. Note all four major Australian banks now tip a July rate cut (NAB brought forward our call last week).

Top news overnight was that Trump levied new sanctions on Iran, but they appear sanctions appear to be more gloss than substance given US sanctions are already very harsh: latest is that the US will bar Iran’s supreme leader from access to the international financial system and also impose of sanctions on eight military commanders. Oil prices haven’t really reacted to the move with Brent lower (-0.7% to $64.73) and WTI slightly higher (+0.5% to $57.69).

Yields continue to hold onto their lows ahead of the weekend’s G20 meeting: US 10s -3.7bps to 2.01%; German 10yr Bund Yields -2.2bps to -0.309%. Equities too with the S&P500 down only slightly overnight -0.2% to 2945. Prospects are not high for a breakthrough with press in China maintain their strong rhetoric. The People’s Daily led with “China will not make concessions” while the Global Times Editor (who is seen by markets as channelling Beijing) tweeted: “current atmosphere between China and the US is not good. What I have learned about China’s stance now is: holding constructive and positive attitude toward upcoming China-US summit, but fully preparing for its failure and an escalating trade war” (see link).

The US Dallas Fed Manufacturing Index was much weaker than expected, falling to -12.1 against -2.0 expected and -5.3 last. The anecdotes were telling in that tariff and trade uncertainty is now causing US businesses to act: “it is hard to quantify, but we’ve taken steps to prepare for a slowdown even though we’re not seeing it yet…we’ve cancelled or reduced orders for inventory and are lowering inventory levels substantially. Debt reduction is a very high priority now”. Last month’s Payrolls showed trade-sensitive sectors of the labour market such as manufacturing, construction and transportation have experienced little-to-no jobs growth in 2019 – which we interpreted then as a flashing amber signal for what an escalation in trade tensions may bring.

German IFO was a tad lower, and while at expectations at 97.4 from 97.9 in May, it is now at its lowest level since November 2014. Interestingly it was the expectations component that deteriorated further (to 94.2 from 95.3), while the current assessment was slightly more positive (100.8 from 100.6). While the later possibly hints at some stability in activity as seen in Friday’s PMI’s, it is worth remembering that German Exports make up around 47% of GDP – so any further escalation in trade tensions has the potential to hit the German economy.

Datawise, it is a quiet APAC session ahead, with all focus on the US Fed Chair later tonight. First up is the NZ’s Trade Balance for May where consensus looks for +250m after last month +433m; our BNZ colleagues are looking for a smaller +55m surplus. Then the AU Roy Morgan Consumer Confidence, RBA’s Bullock speaking on “Modernising the Australian Payments System” in Berlin (both unlikely market moving), and then the BoJ has the Minutes of the April Policy meeting.

Focus then turns to Fed Chair Powell, who speaks at 3am AEST (1pm NY time; 4pm London) on the “Economic Outlook and Monetary Policy” with Q&A at the Council on Foreign Relations in New York. There is also a plethora of other Fed speakers including voters Williams and Bullard, as well as non-voters Bostic and Barkin. With markets now pricing more than a 25bp cut at the July meeting (140% priced now), all focus will be on whether Fed officials hint a July rate cut is likely and whether the Fed would move in a magnitude greater than 25bps (i.e. a 50bps cut).

Data-wise the US has the Richmond Fed Manufacturing Index with likely downside risks following the Dallas/Philly/Empire surveys (consensus looks for a +4 read, but a negative read could be likely). New Home Sales and the Conference Board Consumer Confidence measure is also out overnight (Confidence 131 expected, down from last month’s 134.1).

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.