Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

Markets are looking through the prospect on any unrest on inauguration day, but the more immediate question is what will the President do today?

https://soundcloud.com/user-291029717/trumps-last-day-how-much-will-biden-undo?in=user-291029717/sets/the-morning-call

“Sweet dreams are made of this; Who am I to disagree; I travel the world and the seven seas; Everybody’s looking for something” Eurythmics 1983

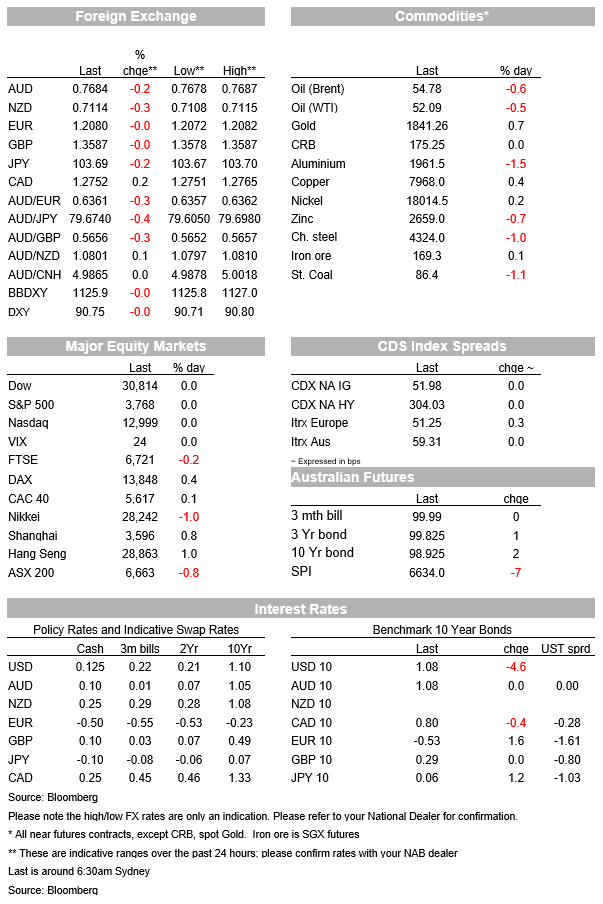

As song titles go, Sweet Dreams by the Eurythmics probably sums up overnight price action the best. It was a night of limited market moves given the Martin Luther King Jr Public Holiday, along with key risk events being later in the week (BoC Wednesday, ECB and BoJ on Thursday, and PMIs on Friday). European equities managed to close in the green with the EuroStoxx50 +0.1% and DAX +0.4%. Yields were mostly higher with 10yr German Bund yield +1.4bps to -0.53%. FX saw commodity currencies underperform (AUD -0.3%, NZD -0.3%, USD/CAD +0.2%) despite the Chinese GDP beat, with a slight risk-off tone following Sunday’s reports of Trump notifying Huawei’s suppliers that it was revoking their licences to work with the company (USD/Yen -0.2%). On net though the USD (DXY) is little changed.

Chinese GDP figures yesterday surprised to the upside with growth of 6.5% y/y v 6.2% expected. Total calendar year 2020 growth was 2.3%, making China one of the few major economies to have a v-shaped recovery. The details though were more mixed, particularly on the monthly activity data with some softness emerging in retail sales (4.6% y/y v. 5.5% expected) and more recently in fixed asset investment (2.9% y/y v. 3.2% expected), while industrial production continues to drive growth (7.3% y/y v 6.9% expected). In contrast, Japanese industrial production in November fell 3.9% y/y, highlighting China’s outperformance.

The USD is also under focus with former Fed Chair Yellen said to affirm the US’ commitment to market-determined exchange rates in her testimony on Tuesday. The approach will be in sharp contrast to the Trump Administration which has attempted to talk down the USD for some time. The WSJ reports: “ Ms. Yellen also doesn’t find it useful to regularly comment on the value of the dollar, and she wants to make clear that the U.S. Treasury, under her leadership, wouldn’t seek to weaken its value, according to the officials. Under the incoming administration, no other cabinet official or White House staff will talk about the dollar, the officials said.” (see WSJ for details ). There have been a few reports highlighting that the USD may see a short-term correction higher. CFTC data shows speculative bets against the USD have built up to their highest level in nearly three years, signalling the vulnerability to a short-term correction higher in the USD. Such a move would likely be only a temporary with structural factors such as the budget deficit and aggressive Fed QE still likely to put downward pressure on the USD.

Domestically we have Weekly Consumer Confidence along with Weekly ABS Payrolls. Neither should be particularly market moving. Offshore it is very quiet with only the German ZEW, Earnings reports (BofA, Goldmans, Netflix) and in the US former Fed Chair Yellen’s confirmation hearing for Treasury Secretary in Biden’s Administration of note. Details below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

Conditions ease as slow growth weighs on firms

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.