NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

In a few hours Joe Biden and Donald Trump go head to head in the last election debate.

https://soundcloud.com/user-291029717/trumps-last-stand-pmis-galore-today?in=user-291029717/sets/the-morning-call

“Oh, once in your life you find someone; Who will turn your world around; Bring you up when you’re feelin’ down; Yeah, nothing could change what you mean to me; Oh, there’s lots that I could say; But just hold me now; ‘Cause our love will light the way”, DJ Sammy/Do 2002

Odd couples don’t come much stranger than DJ Sammy and Bryan Adams, and yet Heaven went on to become the Eurodisco smash hit of 2002 with its uplifting energy a staple for any spin class.

So it was overnight with hopes of US stimulus remaining high after House Leader Pelosi said “we’re just about there”. Importantly for markets, a few Republican senators have also said they would be willing to pass a $2 trillion package, increasing the probability that a stimulus package can be approved prior to the election that is now less than two weeks away.

Stimulus hopes offset the negative vibe from Europe (Eurostoxx50 -0.3%) and Asia (CSI 300 -0.3%) that came in the wake of allegations of US election interference by Iran and Russia, and rising COVID-19 cases in Europe.

Earnings have also been broadly supportive of sentiment with CNBC reporting 83% of companies that have reported so far have topped expectations by an average of 19%.

Equities rose on the stimulus headlines with the S&P500 +0.5%.

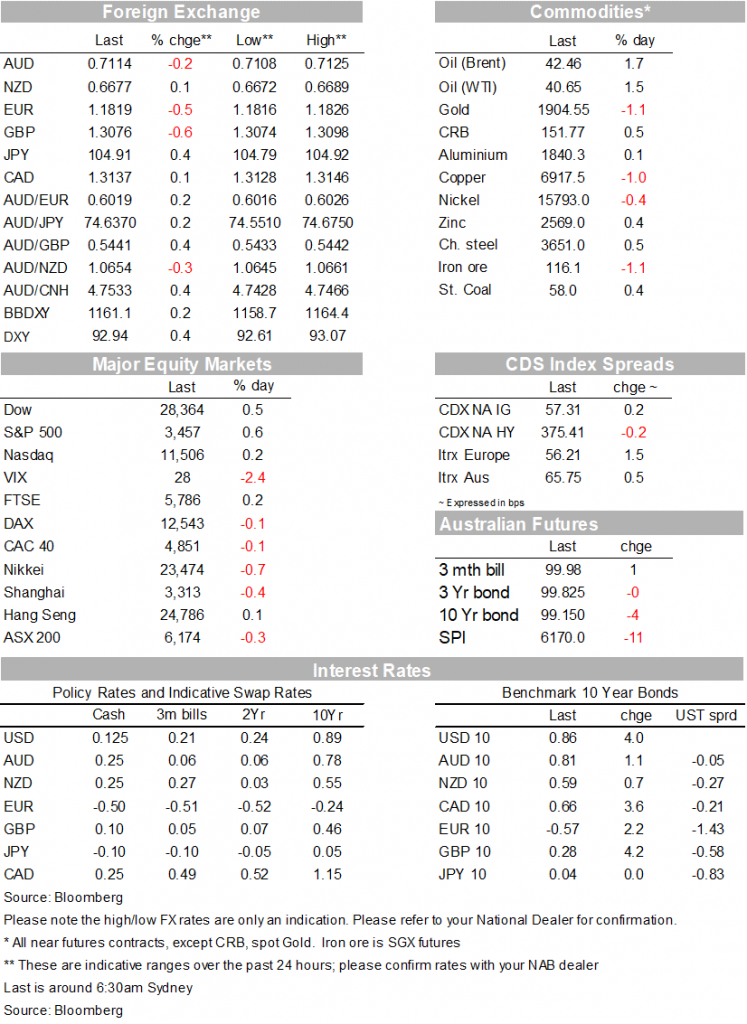

Rates markets have also reacted with the US 10yr yield +4.0bps to 0.86%.

Over the past week there appears to have been a significant change in the way bond markets are assessing the outlook and how probable a US fiscal ramp is with 10yr yields having put on 12.9bps since last Thursday (note implied breakeven inflations have contributed 6.5bps of that move – US 10yr breakeven is at 1.76%).

Part of that reassessment has come on the back of US politics with more commentators talking about the likelihood of the Democrats taking the Senate. To date it seemed a close call on whether Democrats would indeed take the Senate, but interestingly FiveThirtyEight has put a Democratic clean sweep at 72% (see link).

Expect more talk about how high yields could go under a fiscal ramp and what the Fed would do to stem a rise in yields.

But remain hard to interpret. US Jobless Claims at the headline came in much lower than expected and at levels not seen since March (Initial Claims at 787k v. 870k expected and 842k previously; Continuing Claims 8.373m v 9.625m expected and 9.397m previously). California though submitted revised numbers which also saw revisions to recent history.

The Pandemic Emergency Unemployment Compensation saw its numbers rise by 0.51m to 3.3m in early October, suggesting some of the drop in continuing claims reflects unemployed people shifting onto another program after the 6 month period. According to the press release, in non-seasonally adjusted terms there were 23m people in total receiving unemployment benefits in some form as at October 3 (see BLS for details), and suggests despite the mild improvement in headline claims the levels remain uncomfortably high.

One data piece that was not hard to interpret was Existing Home Sales which beat (9.4% m/m v. 5.0% expected), and illustrative of the strength seen in the housing market to date.

It was a story of USD strength with DXY up 0.4% with EUR (-0.5%), GBP (-0.6) and JPY (USD/YEN +0.4%) all on the softer side.

There was no clear catalyst of the moves, though it is worth noting the rise in COVID-19 infections in Europe and the imposition of more restrictions have the potential to weigh on growth.

Headlines are not pretty with supermarket hoarding occurring again in Germany, likely in anticipation of another lockdown.

A likely update of the impact on activity will come with the flash PMIs later today which only sees a very mild impact on the services sector according to the consensus.

GBP will continue to remain sensitive to EU-UK trade headlines, fishing rights are said to remain one of the key sticking points in a deal.

It was a story of mild outperformance with AUD down just -0.2% and NZD +0.1% and both outperforming on the crosses.

The strength seen in the CNY and CNH recently reversed course yesterday after allowing domestic funds to invest more insecurities overseas (USD/CNH is +0.5%).

A mostly quiet day domestically with only the CBA/Markit PMIs which have a limited time history in Australia.

NZ has Q3 CPI figures, which may also give some steer towards Australia’s CPI figures next week.

The PMIs take prominence and will be closely watched for any impact on activity from rising virus numbers. Details below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.