Online retail sales growth slowed in May following a fairly strong April

Insight

US Treasury yields pushed steadily higher overnight, reaching 1.6 percent for 10 year Treasuries.

You’re not the only one with mixed emotions

You’re not the only ship adrift on this ocean – Rolling Stones

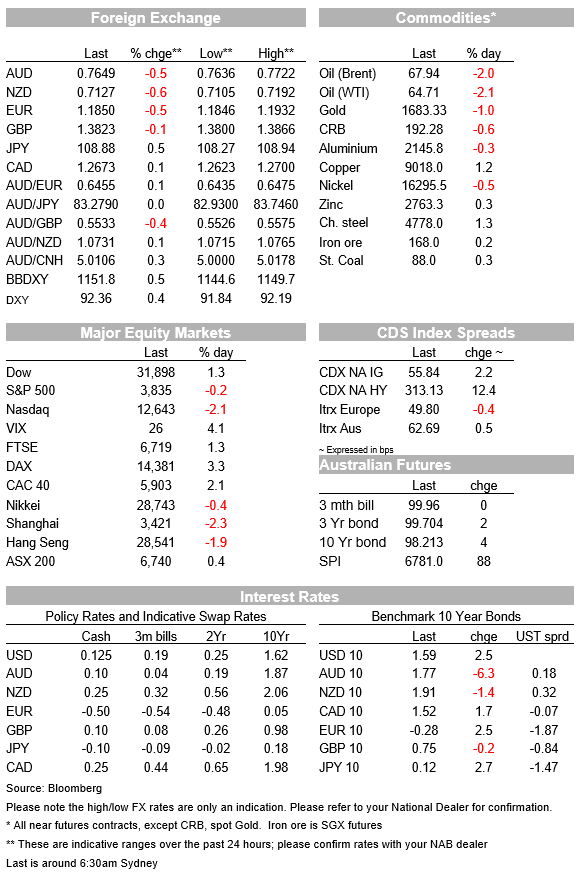

European and US equities have begun the new week on positive mood with pro cyclical shares favoured while long duration/tech shares are sold, NASDAQ down more than 1%.10y UST consolidate just below 1.60%, but the 5y tenor has continued to rise, up 5bps to 0.85%. Move up in UST yields supports the USD, the AUD and NZD are a tad softer with downward pressure on EM FX a risk to watch.

Overnight equity market gains in Europe and the US have been driven by cyclicals and banks, a sign of optimism about the economic outlook and the impact of steeper yield curves . European equities have begun the new week with a spring in their step with all regional indices showing gains between 1% and 3% while the Stoxx Europe 600 Index gained 2.1%, its best day since early November last year. The smaller share of IT and growth stocks, more sensitive to a rise in yields, is now favouring Europe with cyclical sectors like automotive (+3.8%), banks (+3.6%) and miners (+3.4%) leading the charge.

The outperformance or rotation towards industrial and cyclical stocks is also evident in the US with the Dow up 1.73% as I type while the NASDAQ (IT Heavy) is down 1.04%. The S&P 500 is up over 0.5% with Materials (2.07%), Utilities (2.03%), Industrials (1.87%) and Financials (1.76%) at the top of the sector board while IT is down 1.09%.

The positive European equity market start to the week was helped by impressive news from Germany. Late on Sunday, Germany’s Finance Minister Olaf Scholz said that it will drastically speed up its coronavirus vaccination campaign with the aim of getting as many as 10m people vaccinated per week from the end of March ( yes you read that right). That is an outstanding commitment, especially when we consider the country’s underwhelming vaccine rollout so far, just 7.3mn distributed since inoculations started 10-weeks ago. This commitment, however, comes with the condition of vaccine producers picking up the pace of delivery and will be aided by the expectation of Europe approving the Johnson & Johnson vaccine this week.

A ramp up in vaccine roll out is not just limited to Germany, overnight EU Commission spokesman Eric Mamer remarked that the forecast for 300m vaccine roll out in the second quarter takes all available vaccines into account, including those yet to gain regulatory approval, such as the one from Johnson & Johnson.

One of the narratives for the weaker euro this year has been a slow rollout of vaccines across the EU. Thus, on this score, it is interesting to note the lack of euro reaction to the positive vaccine news overnight. Indeed, the EUR underperformed overnight, briefly slipping below 1.1850 a fresh 3½-year low (now at 1.1853). Maybe it is the case that the FX market will have to see the vaccine rollout success before the euro is rewarded.

The USD has started the week on a positive note, in the afterglow of the US Senate signing off on Biden’s massive $1.9t fiscal relief package , with only minor amendments. US Treasury Secretary Yellen dismissed fears that the fiscal stimulus would stoke inflation, saying “if it turns out to be inflationary, there are tools to deal with that”. We’d note that the tool to “deal with that” is higher interest rates, precisely the sentiment the market has been adopting this year. The US 10-year rate is consolidating around the 1.60% mark, a few ticks higher from last week’s close, but just under Friday night’s high of 1.62%.

Of note, however, the 5 year part of the UST curve has continued its ascendency, up 5bps and now trading at 0.85% and from a technical perspective there is not a lot resistance for the tenor to move above the 0.90% mark. After the very soft 7y UST auction last month, which contributed to the recent move up in UST yields, the market will be watching very closely how investors deal with $120bn of new UST bonds this week, starting tonight with $58bn 3y notes auction followed by $38bn in 10 UST notes and $24bn the 30y bond later in the week.

The trend of higher US bond yields that has lifted the USD with USD/JPY again showing a higher degree of sensitivity to the move up in 10y UST yields. USD/JPY is now on the verge of breaking up through 109, having started the month at 106.

The move up in UST yields also continues to put a dampener on sentiment for emerging markets . JP Morgan’s EM currency index has been in freefall since late February, falling over 4% in just over a week, ignoring much stronger than expected China trade data over the weekend. USD/CNY broke up through 6.50 for the first time since early January, while China’s CSI index of stocks fell 3.5%, taking losses from the February peak to 13%, leaving the index in correction mode and technically vulnerable to more downside risk.

The AUD and NZD have struggled a little bit at the start of the new week, the AUD now trades at 0.7647, down 0.44% over the past 24 hours while NZD is -0.53% and at 0.7127. We think EM struggles need to be monitored closely given that history tells us that broad EM corrections tend to weigh on both antipodean currencies.

Moving onto commodities, metal prices and iron ore closed marginally higher while Brent crude has settled back down to just over USD68, after trading as high as USD71.30 yesterday. On Sunday, Saudi-led coalition warplanes bombed Yemen’s rebel-held capital, Sanaa, after Houthi rebels attacked Saudi oil facilities with drones and ballistic missiles. The rebel strikes reportedly did little to no damage to oil storage sites.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.