NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

US-China trade talks and Brexit negotiations both look like some sort of deal could be reached.

https://soundcloud.com/user-291029717/two-big-slugs-of-positivity?in=user-291029717/sets/the-morning-call

Sweet as sweet as sweet can be, You don’t know whatcha do to me

Oh we’re gonna groove, yeah groove, Yeah we’re gonna groove baby- Led Zeppelin

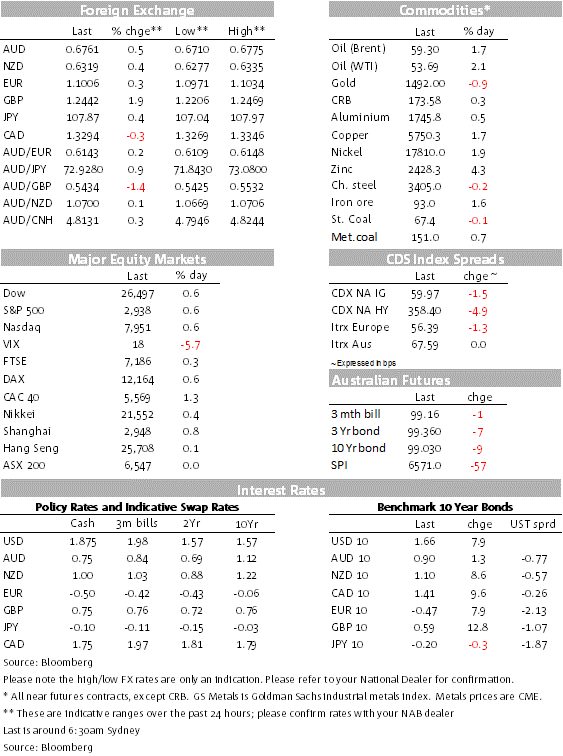

In what has been a jittery past 24 hours, amid initially conflicting headlines, markets have moved into a pretty groovy mood boosted by positive Brexit headlines and improved prospect of a US-China détente. EU and US equities have enjoyed a second day of decent gains, US Treasury yields are higher in an almost parallel fashion with a soft US CPI print going straight through the keeper, given markets’ focus on trade headlines. The USD is broadly weaker with GBP leading the charge in G10 while ZAR and TRY are the big winners in EM FX. The improvement in risk sentiment and higher commodity prices also sees the AUD and NZD stronger, up around 0.5%.

Well after some conflicting headlines yesterday suggesting Chinese negotiators were looking to head on Thursday rather than Friday, the mood music changed for the better with initial early departure denials followed by “leaked commentary” suggesting the US was aiming at reviving a currency pact with China in exchange of suspending the plan increase in tariffs next week. Prospect of an interim deal were also boosted overnight following reports that President Trump was planning to meet Vice Premier Liu He on Friday.

Once the conflicting headlines were digested, the mostly positive headlines that followed boosted risk sentiment and helped EU and US equities closed with decent gains for a second day in a row. The Euro Stoxx 600 index closed 0.65% higher with all major regional indices showing gains between 0.58% (DAX) and 1.27% (CAC 40). On the other side of the Atlantic the S&P 500 closed 0.64% higher with energy (+1.40%) and Financials (1.14%) leading the charge. The Dow ended 0.57% and NASDAQ was 0.60%.

The prospect of US-China trade truce that results in the suspension of further planned tariffs increases is rightly a welcome news. But as it is often the case, the devil will be in the detail. If the current groovy vibes are to become longer lasting, a meaningful de-escalation in tensions is required. Freezing tariffs at current levels are unlikely to reverse the current trade driven slowdown in economic growth and the uncertainty around unresolved structural issues such IP theft and subsidies to state own enterprises are likely to remain deterrents for a pick-up in much needed capital expenditure.

On this score details on a potential currency pact will be important. On the one extreme if China was to agree to let the yuan to be completely driven by market forces, arguably we could see USD/CNY easily head above 7.50. Clearly not something the US would like. On the other extreme, it is also difficult to see China agreeing to forcing an appreciation of yuan.

Similarly in terms of the structural tensions, kicking the can down the road is unlikely to benefit President Trump’s election prospect. So at a minimum, we suspect that a US-China détente needs to come with clear deadlines (dates) for a resolution plan to these structural tensions. China so far has shown no appetite to even address these issues, so for the market groovy vibes to persist these uncertainties need to be resolve.

The risk-on mood sees US rates higher across the curve in an almost parallel fashion with the 2y tenor up 5.1bps to 1.518% and the 10y note up 6.7bps to 1.6646%. Notably the rise in yields occurred despite US CPI data coming in softer than expected. The core rate rose by just 0.1% m/m after a run of three monthly increases of 0.3%. The soft CPI alongside underwhelming ISM prints, suggest hawks within the FOMC are losing important ammunition in order to push back at the prospect of further Fed easing. The late October FOMC meeting remains live with upcoming data and reaction to trade news pivotal. The market now prices a 78% chance for a 25bps Fed funds rate cut at the end of the month.

The other risk-positive event over the past 24 hours has been Brexit news. UK PM Johnson and Irish Premier Varadkar met and issued a joint statement saying “they agreed that they could see a pathway to a possible deal”. Varadkar later told reporters that while obstacles remain he hopes the progress will be enough for formal negotiations to restart in Brussels. The Irish Times reported that there was “very significant movement” from Johnson on the customs issue, with no further detail provided. The positive vibe has raised some hope for a chance of a Brexit deal ahead of the EU summit at the end of next week.

GBP is up strongly on this development and is currently up 1.88% to 1.2441. As usual, GBP remained more sensitive to Brexit news than UK economic data, which weren’t market moving. UK GDP data were strong enough to suggest that the economy likely avoided recession – after the contraction in Q2, the Q3 figure is on track for a small positive – but industrial production was much weaker than expected in August, highlighting the struggles for the manufacturing sector.

The risk-on mood sees the safe-haven currencies CHF and JPY weaker, while USD indices are down around 0.4%. The AUD is up 0.58% from this time yesterday to 0.6770, in addition to the improvement in sentiment, broad gains in commodities have also helped the AUD with Brent oil +1.17% and LMEX index +1.60%. The NZD’s tight range evident this week extended a little, as it reached a high of 0.6335 last night, helped by a slightly stronger yuan. Overall, currency markets have been less sensitive than equity indices/futures to the oscillating trade war news headlines. The NZD currently sits at 0.6319, up 0.46% over the past 24 hours, but little changed from where it ended last week.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.