On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

Even though a hard deadline has been set for Sunday for the UK-EU trade deal, there’s no guarantee it will all end there.

https://soundcloud.com/user-291029717/uk-eu-no-deal-looms-aussie-breaks-75-cents-ecb-to-buy-more-bonds?in=user-291029717/sets/the-morning-call

“(You) You don’t really want to stay, no; (You) But you don’t really want to go-o; You’re hot then you’re cold; You’re yes then you’re no; You’re in then you’re out; You’re up then you’re down”, Katy Perry 2008

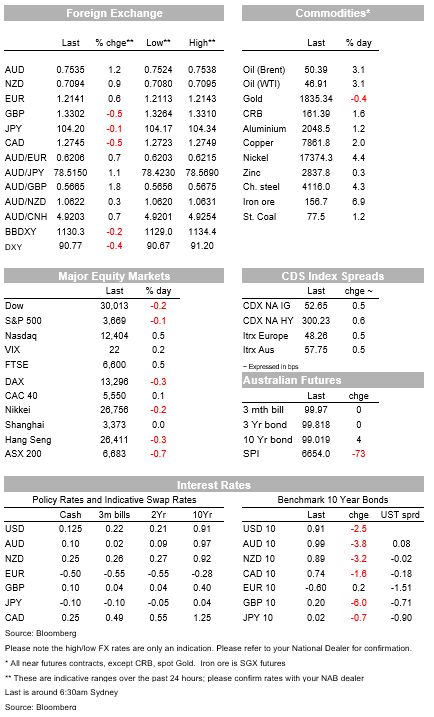

Katy Perry’s 2008 hit ‘Hot N Cold’ neatly sums up the stance of UK-EU trade negotiations, which overnight ran cold and saw GBP fall -0.6% to 1.3280 despite widespread USD weakness (DXY -0.3%).

EU President von der Leyen said both sides remained “far apart”, while UK PM Johnson said there was a “strong possibility” that a deal will fail; the next deadline is this Sunday (“firm decision should be taken about the future of the talks by Sunday”), though in reality negotiations could go all the way up until December 31.

Numerous analysts have now downgraded their chances of a deal to around 50-60%.

US fiscal stimulus negotiations also have not progressed with key differences remaining over a legal liability waiver for businesses and aid to the states. This intransigence coming despite signs of renewed weakness in the labour market with Jobless Claims overnight more than expected.

Markets though are having to balance a weak short-term picture against a much rosier medium-term as vaccines start to be rolled out (note the US FDA’s vaccine committee is meeting now with emergency use authorisation widely expected for Pfizer/BioNTech given the UK has already started vaccinations).

In this environment equities have largely held onto recent gains, with the S&P500 down -0.1% overnight.

The USD though continues to weaken (DXY -0.3%), while EUR ascent goes unabated (EUR +0.4%) despite the ECB injecting further stimulus (as widely expected) and as EU leaders finally signed off on the already flagged €2.2tn EU Recovery Fund backed by jointly held debt.

The Pandemic Purchase Programme was increased by €500bn to €1850bn (largely expected) and extended by nine months through to March 2022. The ECB also offered three more cheap long-term loans to banks for an additional year, through June 2022.

The one possible hawkish line was the ECB President suggesting that the full €1850bn might not be used if growth is rebounding strongly by mid-2021 as the forecasts currently imply.

Meanwhile the inflation outlook was downgraded, rising only to 1.4% in 2023

Commodity prices are lifting with Brent above $50 a barrel (+3.1%), Copper +2.0% and Iron Ore Futures lifting strongly to $156 a tonne (albeit supply issues in Brazil and the Chinese Winter a factor).

Commodity currencies are outperforming with the AUD +1.2% overnight and breaking 0.75 to be at 0.7530.

NZD was also up 0.9% overnight to 0.7089, while Aussie outperformance saw AUD/NZD lift 0.3% to 1.0621.

US Jobless Claims rose more than expected (853k v. 725k expected and 716k previously).

The rise looks like it is partly due to seasonal adjustment issues associated with Thanksgiving given the prior week saw an unexpected decline.

Despite that, it is clear US labour market has deteriorated given the rise in COVID-19 cases and the re-imposition of restrictions.

Also out overnight was the US CPI, which was one-tenth more than expected on both the Core and Headline. Core CPI rose 0.2% m/m and 1.6% y/y (v. 0.1%m/m and 1.5% y/y expected).

The rise in core was broad-based, with the most notable increases being seen in the services sector, including airline fares (+3.5% m/m after last month’s 6.5%) and lodging (3.9% after falling last month by -3.2%).

The lift in the CPI is likely to continue to see the buying of inflation protection by some in the market.

Treasury Secretary Mnuchin gave some positive spin, suggesting that progress had been made after further talks and Senate Majority Leader McConnell was on board with his plan.

The Democrats are still working on the original bipartisan plan, seeing that as the best path forward. So there is some argument between the original $908bn plan and Mnuchin’s $916bn plan, but the key sticking points are around a business liability waiver for COVID-19 lawsuits and state aid.

Domestically it is quiet with no data scheduled.

Offshore it is also quiet with only US Consumer Sentiment and PPI of interest. Details below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

Firmer consumer and steady outlook

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.