Long-term signal vs. Short-term noise

Insight

The UK government going halves on lunch if you eat out in the first half of the week.

https://soundcloud.com/user-291029717/uk-government-goes-dutch-on-lunch?in=user-291029717/sets/the-morning-call

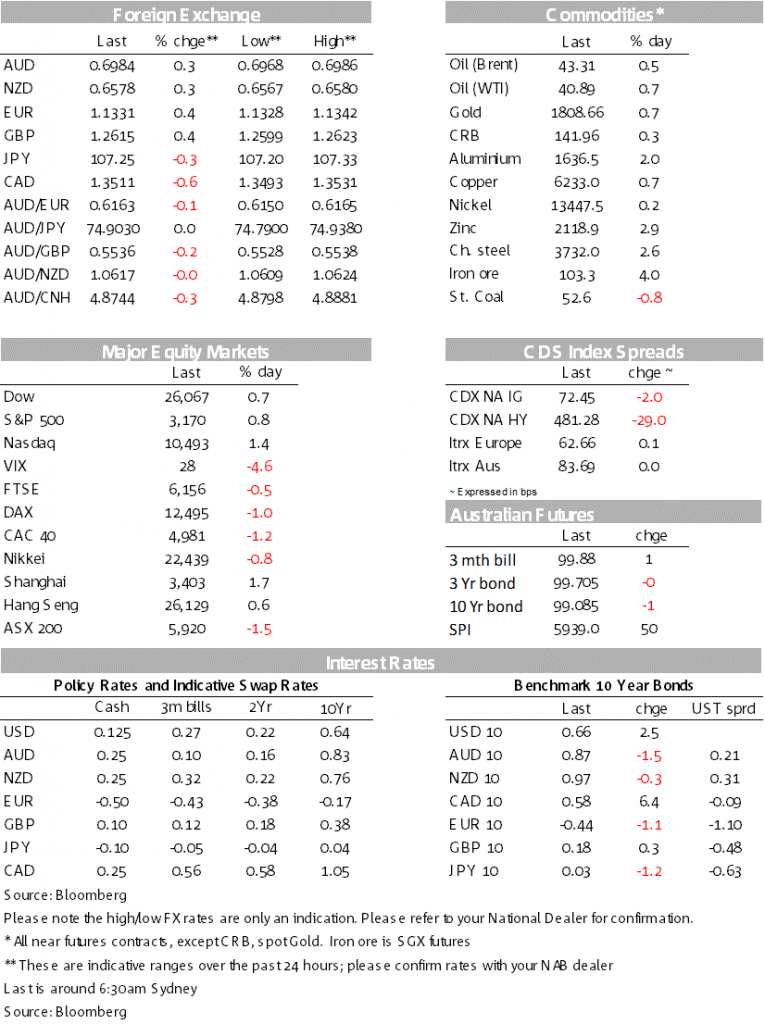

The UK’s latest £30bn stimulus package was well received by markets, helping lift GBP +0.4% and EUR in its wake. The tech rally continued and risk sentiment overall remains resilient to virus and re-opening risks – equities rose (S&P500 +0.8%), yields rose slightly (US 10yr +2.5bps), the USD fell (DXY -0.4%) and the AUD rose (+0.3%).

“Left me sleepin’ in my bed; I was dreaming, but I should have been with you instead; Wake me up before you go-go; Don’t leave me hanging on like a yo-yo”, Wham 1983

Risk sentiment remains resilient ahead of next week’s key earnings reports (note Tuesday sees JPMorgan/Citigroup/Wells, and Thursday the tech heavy weights of Microsoft and Netflix). The S&P500 rose 0.8%, though has largely been treading water in a narrow range since mid-June. Helping drive overall gains is tech with the NASDAQ up 1.4%, driven by Apple (+1.9%) outperformance with Deutsche hiking their price target. Vaccine news flow remains on the positive side with Moderna reporting they are on track for phase 3 trials in July and have completed phase 2 enrolments. Fed talk was also surprisingly bullish with Bullard stating unemployment could fall rapidly without having to wait for a vaccine if we can use simple, easy technology (read wear a mask). Bullard said: “seems to me like by the end of the year you can get down certainly to single digits, probably even below 8%, maybe 7% by the end of the year” (see CNBC interview).

It was the case of the UK Chancellor’s latest stimulus package helping to propel GBP +0.4% higher and is currently near session highs of 1.2615. The move in GBP also helped lift EUR which is up also up 0.4%, which put the USD (DXY) on the backfoot with DXY -0.4%. As for the stimulus package itself, UK Chancellor Sunak unveiled a £30bn (1.4% of GDP) “plan for jobs” which entails tax cuts on home-buying and dining out, and a new bonus program for employers who re-employ staff on furlough. In terms of detail, stamp duty thresholds for property purchases until the end of next March will be raised meaning nearly 9 out of 10 people buying homes will pay no stamp duty at all. Sales tax for restaurants, hotels and attractions will be cut to 5% from 20%. Employers will receive a one-off bonus of £1,000 per employee if they re-employ furlough workers through to January (worth some £9bn). Grabbing headlines (and much chatter in our London office) was the “Eat Out to Help Out” scheme which entitles diners to a 50% discount of up to £10 per head on their meal at any café/pub for the entire month of August! (see the Plan for Jobs for details).

Commodity currencies were also lifted overnight amid the positive risk sentiment and USD weakness, with the AUD +0.3% and NZD +0.3%. The AUD is currently at 0.6981 and continues to shrug off the Melbourne 6 week lockdown that was put into effect at midnight. So long as the virus outbreak in Melbourne remains isolated to Victoria, we do not think it will have an enduring impact given the state government’s willingness to do what it takes to control the virus and historical experience suggesting it takes around 4-6 weeks to supress the virus and Victoria could be back to easing restrictions in the second half of August. Commodity prices also remain a support with Brent oil up +0.5% and gold rallying +0.8% amid reports of record ETF inflows – US$39.5bn billion flowed into gold-backed ETFs in the first six months of the year according to World Gold Council figures.

Yields edged higher with US 10yr yields +2.5bps to 0.66%. Yield moves in Canada though were more erratic and a potential warning for bond markets in terms of the deluge of supply likely to come through the pipeline to fund government stimulus. Following a fiscal update that shows a deficit of 15.9% of GDP in 2020/21, Canadian 10yr bond yields rose 6.4bps to 0.57%. On the other hand UK GILT yields were little changed after the Chancellor’s latest fiscal package. Also in rates news, the New York Fed’s Singh highlighted further tapering of corporate credit purchases given improved risk sentiment and corporate spread: “Fed’s [corporate credit] purchases could slow further, potentially reaching very low levels or stopping entirely” (see Speech).

The number of confirmed cases in the US has passed 3 million, representing more than a quarter of all cases globally. Arizona and Florida both reported increases in cases, but at lower rates than their 7-day averages. The US is ramping up testing in the troubled southern states of Louisiana, Texas, and Florida. This will help clarify the situation as officials weigh how far to go in reopening.

Lastly reports of a proposal by some of President Trump’s advisers to undermine Hong Kong’s currency peg fizzled out as it hasn’t been elevated to senior levels of the administration. But it is yet more signs of the simmering tension between the US and China.

Quiet domestically again with only housing finance approvals which are unlikely to trouble the scorers. Internationally it is more interesting with the ANZ Business Survey for July, Chinese factory price inflation and US jobless claims. Key releases below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Long-term signal vs. Short-term noise

Insight

Welcome to NAB’s newsletter on the Sustainable Finance market from an Australasian perspective.

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.