Housing market sentiment rallied as national housing price growth accelerated in the March quarter.

Insight

Could slowing inflation cause the Bank of England to rethink the prospect of an August rate rise?

https://soundcloud.com/user-291029717/powell-upbeat-uk-rate-rise-slightly-less-certain

Nothing like a Beatles classic to start the day. Equities ex tech shares and commodities have had good night with Morgan Stanley leading the gains in financials. Soft US housing data and a less hawkish Fed Chair Powell combined to drive a small steepening of the UST curve. The USD struggled to retained early session gains with a rebound in commodities helping commodity linked currencies perform. AUD is toying with a move above 74c and NZD is almost back above 68c.Meanwhile GBP can’t find any loving with a soft CPI report dragging the pound to a new year to date low.

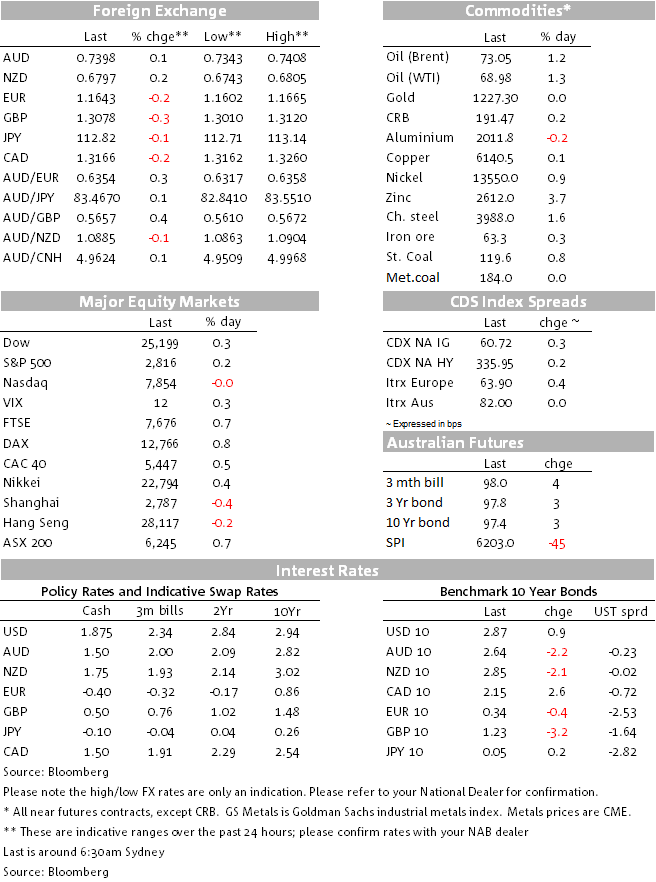

Fed Chair Powell testimony before the House committee overnight was not that dissimilar to yesterday’s appearance before the Senate. At the margin, however, some of Powell’s remarks overnight had a less hawkish tilt relative to the previous day. On inflation Powell noted that although the core reading had converged to the Fed’s 2% target, the Fed was still “slightly more worried about lower inflation”. In another slightly dovish remark, Powell said “we’re close to full employment, maybe not quite there”, which seems a little surprising given the US unemployment rate is 4%.

On trade news we had a couple of good sound bites that have also helped risk sentiment. Following on from similar remarks made by Mexican officials yesterday, President Trump said overnight a US-Mexico trade deal was “getting closer” and the US administration may seek a deal with Canada at a later date. Meanwhile ahead of the 25th July meeting next week with European Commission President Junker, US president Trump said that “if we don’t negotiate something fair, then we have tremendous retribution, which we don’t want to use, but we have tremendous powers”. But on a more upbeat remark, Economic Advisor Larry Kudlow said Junker “is bringing a very important free-trade offer.” Next week Wednesday (early Thursday for us) could bring some important news on the US-EU trade dispute.

So while we have not seen big moves in markets overnight US equities performance continues to provide a positive backdrop for Develop Market (DM) equities. Meanwhile the picture in Emerging markets (EM) remains mixed, EM FX ex Asia for instances is having a good month, the appeal of carry amid a declining volatility environment has seen the MXN and ZAR record gains close to 5% with recent trade sound bites also favouring the MXN fortunes of late. Meanwhile in Asia, the market remains weary of China’s equity market and CNY weakens. The Shanghai composite index had another down day yesterday and USD/CNY is now back above the 6.70 mark. The latter obviously reflect markets concerns over US-China trade tensions and while we wait for a resolution (hopefully a positive one) it is difficult to see the AUD making material gains even if risk appetite remains buoyant in DM markets, but not in Asia.

US Financial led the gains in US equities with Morgan Stanley leading the way after a decent earnings report that beat most estimates. For a change, overnight technology shares were the laggers, the NASDAQ index closed slightly in the red with Microsoft and Apple amongst the underperformers. Early in the overnight session, major European equity indices closed with gains between 0.3% and 0.80%.

Fed Chair Powell testimony and softer US data ( more below) played into a mild steeping of the UST curve. The 2y rate closed a tad lower at 2.61% (-0.5bps) and the 10y year rate edged 1bps higher to 2.87%. A move above to 2.87% has proven to be an unsurmountable test for the 10y tenor in July, that said at 2.87% the 10y UST yields is now at the top of its 2.81%-2.88% held over the past three weeks, a break above 2.88% could open the path for a move above 2.90%,so it’s probably worth keeping an eye on it.

The USD had a night of two halves. DXY climbed to an overnight high of 95.401 early in the session, boosted by a decline in GBP after a soft CPI print, but later in the session gains in commodities helped commodity linked currencies perform forcing the USD to give back some of its early gains. DXY now trades at 95.09.

The pound fell to a new year-to-date low of 1.3010 in the wake of the CPI report, although it has since recovered to 1.3060. Despite the move in the currency, the market still assigns around an 80% chance of a BoE rate hike at its meeting next month. UK parliament is due to go into recess next week, returning in early September, although Brexit and UK politics will remain a headwind for the GBP for some time.

The improvement in risk sentiment following positive trade sound bites and Powell’s less hawkish remarks helped commodities performed (more below) which in turn lifted the likes of NZD, CAD and AUD. The kiwi has led the gains again within G10 (+0.18%) and now trades at 0.6794 and the AUD is up 0.12% currently trading at 0.7398.

Zinc is up 3.50% while oil prices are up close to 1% boosted by an unexpected drawdown in US inventories and a drone attack on an ARAMCO refinery. Gold is unchanged, Dr Copper is ++0.55% and Aluminium is the one exception, down 0.25%.

UK: CPI (y/y%), Jun: 1.9% vs 2.6% exp.

UK: Core CPI (y/y%), Jun: 2.4% vs 2.1% exp.

EZ: Core CPI (y/y%), Jun: 0.9% vs 1% exp.

US: Housing starts, Jun: 1,173 vs 1,320k exp

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Housing market sentiment rallied as national housing price growth accelerated in the March quarter.

Insight

Growth slowing, but less abruptly than Q1 GDP suggests

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.