Online retail sales growth slowed in May following a fairly strong April

Insight

The UK has started injecting people with the COVID vaccine. If only they could inject compromise in the UK and EU negotiators who remain a long way from reaching a deal.

https://soundcloud.com/user-291029717/uk-trade-talks-to-get-an-injection-but-the-prognosis-is-not-good?in=user-291029717/sets/the-morning-call

“Little darling, it’s been a long cold lonely winter; Little darling, it feels like years since it’s been here; Here comes the sun, do, dun, do, do; Here comes the sun, and I say; It’s all right”, The Beatles 1969.

William Shakespeare became one of the first people in the world to be vaccinated with the Pfizer/BioNTech vaccine as the UK commenced its vaccine rollout overnight. The Bard’s name brought much light-heartedness to the occasion with social media erupting in a cascade of puns (the best your scribe saw was “Is this a needle which I see before me ?”). The US is also expected to give emergency use authorisation with the US FDA publishing briefing documents that concluded it had “a favourable safety profile” and the FDA’s vaccine’s committee is meeting on Thursday. Such positive headlines saw equities pull into the green with the S&P500 +0.4% overnight. Meanwhile UK-EU trade negotiations continue, though cable so far is still trading as if a deal is likely (GBP 1.3360), while across the pond US fiscal negotiations continue and again with little in the way of a breakthrough.

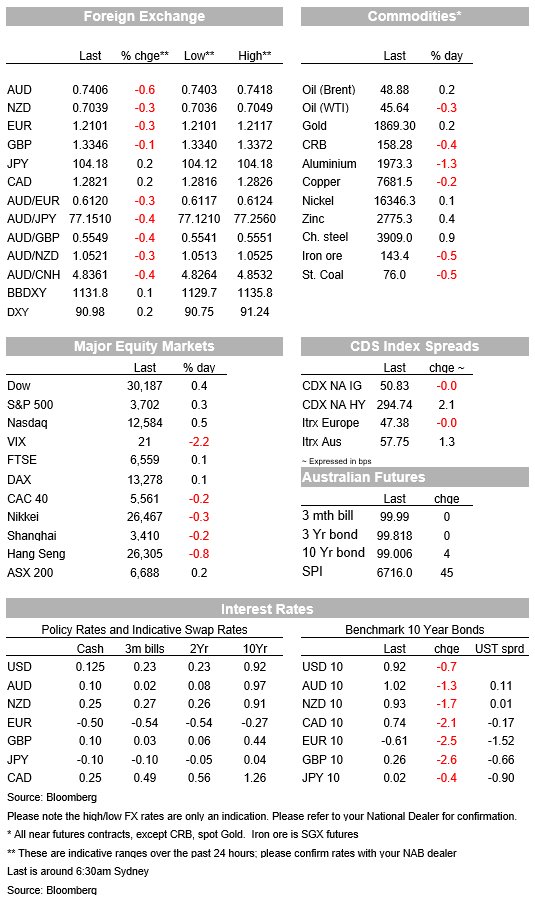

The USD DXY rose 0.2% with EUR (-0.3% to 1.2104 ) and GBP (-0.1% to 1.3346) weaker on UK-EU trade headlines, though initial moves were largely reversed after news of PM Johnson being set to meet with leaders on Wednesday ahead of the EU Summit on Thursday, and as the UK dropped one of the controversial clauses in the UK Internal Markets Bill that would have broken international law and have allowed ministers to override parts of the UK-EU Withdrawal Agreement. The main sticking points for a trade deal remain around fisheries, ensuring a level playing field and enforcing the agreement. The EU’s Chief Negotiator Barnier said that a deal was now “very slim”, so it remains unclear whether an agreement can be reached this week.

It underperformed overnight down -0.6% to 0.7406 with no specific driver apart from USD strength. The underperformance of the AUD sees the AUD/NZD fall 0.3% to 1.0521.

Republican Senate leader McConnell is still pushing for a slimmed down $500bn package, whereas the Democrats are backing a larger bi-partisan $908bn package. Two roadblocks are said to be around the proposal of providing aid to the states, as well as whether to give business liability protection from COVID-19 related lawsuits. McConnell is meeting with Trump Administration Officials later today. Democratic House Leader Pelosi for her part remains optimistic about getting a deal, but also emphasised that a deal would merely be a supplemental to a larger package was President-elect Biden is inaugurated.

There was little in the way of data overnight with only the German ZEW and the US NFIB of note. The German ZEW survey surprised on the expectations components (55.0 v 46 expected and 39 prior) and plays to the view of a very positive medium-term picture given vaccine hopes. In contrast the ‘current situation’ component remained deeply in negative (-66.5 v -66 expected and -64.3 previously). The US NFIB Survey fell as largely expected (101.4 v 102.5 expected and 104.0 previously). Interestingly though, the selling prices index rose 3 points to its highest level since May 2019. The rise in selling prices aligns with the rise in the prices paid indexes seen in the US ISMs recently and is likely to keep the debate around whether inflation is set to pick up alive.

Implied inflation breakevens though continue to rise with the 10yr inflation breakeven +0.9bps to 1.8967%. Some in the market still conceivably wanting to hedge against the risk of inflation, while the lift in nominal yields is being watched by the Fed with expectations of some sort of QE twist at the upcoming FOMC meeting next week. That dynamic is putting downward pressure on real yields, one of the factors behind the weaker USD recently.

Yesterday’s NAB Business Survey showed a sharp bounce back in confidence and conditions and suggests a rapid rebound in the economy is occurring as restrictions are eased and as borders open up. Conditions rose to +9 from +2, while Confidence bounced even stronger to +12 from +3. The one soft bit in the survey was the Employment sub-Index which remained in negative territory at -5. In contrast Trading Conditions (at +17) and Profitability (at +15) were up strongly. The lack of a bounce in the Employment sub-index might reflect a rise in hours worked rather than new employment. Nevertheless, separate SEEK Job Ads continue to point to a strong rebound in labour demand with job ads above pre-pandemic levels in five states and territories.

Domestically it is quiet with only the monthly consumer sentiment index. Offshore it is also quiet with mostly second tier data and no central bank speeches scheduled. Details below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.