Total spending grew 0.9% in June.

The US Fed announces unlimited QE.

https://soundcloud.com/user-291029717/unlimited-qe-in-a-world-of-radical-uncertainty?in=user-291029717/sets/the-morning-call

Risk asset markets remain under pressure despite ever more dramatic scaling up of central bank or government fiscal support programmes – but on the latter not yet in the US where the Administration and White House are still bickering. Policy makers are nevertheless unable to get ahead of the race to counter ever more dire warnings about the depth to which economic activity globally is in the process of sinking and the potential loss of equity or corporate debt values, whether from full-scale or partial nationalisations, or corporate bankruptcies.

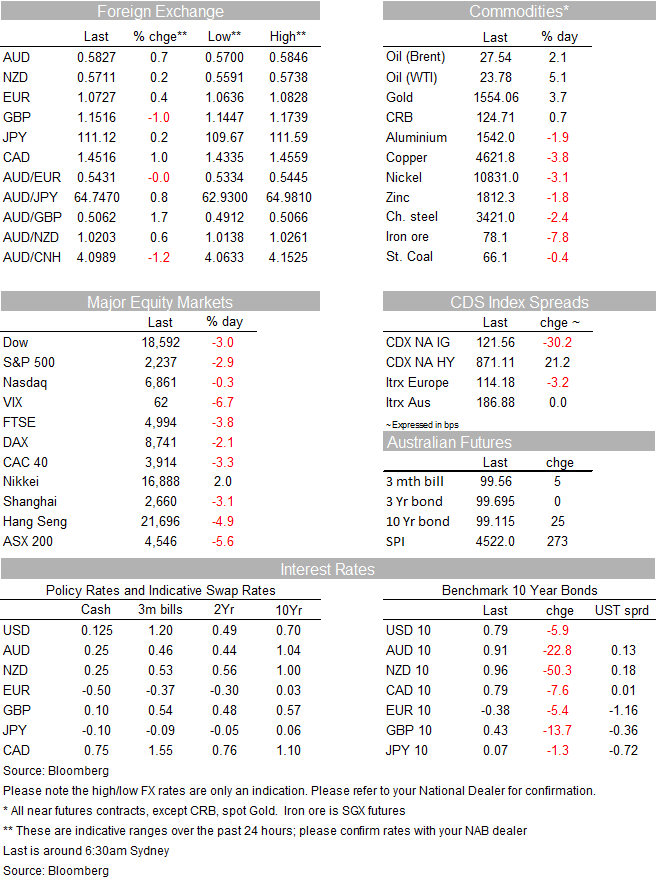

Equity markets have just seen the S&P500 close down 3%; earlier the Eurostoxx 50 closed down ‘just’ 2.5%, in part because Germany is finally recognising the scale of fiscal and monetary support required not just domestically but across Europe, Italy in particular – a far cry from their attitude less than two weeks ago (see below).

Bond markets are back finding support from apperception of how much debt central banks will be buying in coming months, for now trumping the concerns about forced sales by both public and private asset managers in need of liquidity or cash to shore up budgets (think oil producers) and the certainty of massively scaled up bond supply down the track. 10-year Treasury yields are currently -6bps on the night to 0.78%

The USD remain extremely well supported , the Bloomberg BBDXY index up another 0.25% to a new record high AUD at least is little changed on this time yesterday, USD gains being led by falls of just over 1% in GBP and CAD, the latter in conjunction with oil prices showing as yet no signs of being abl to get up off the floor. Base metals are lower again led by a near 5% fall for copper.

The scale of monetary policy support, in all its guises and which is already being described in some quartesr as de facto Modern Moentary Theory – in short, central banks printing cash without their being a government liability on the other side – is already going well beyond anything we saw during the GFC. In the meantime Congress gave just failed for a second time to approve a near US$2tn coronavirus economic support plan, reminiscent of the 2008 TARP. This morphed into $450bn+ worth of support for the partial nationalisation of the US auto industry and which the government eventually sold back to the private sector at a profit. TARP was initially rejected by Congress on 29 September 2008 before being passed on 3 October, under acute interim market pressure and at the loud public urgings of folk such as Warren Buffet.

The Fed has committed to buying debt, not just government and residential mortgage backed securities but now for the first time commercial mortgages (paper backed by office buildings and the like). Unlike during the post GFC period when there were quantitative limits on how much the Fed would buy each month, purchase amounts are now unlimited. There is also a plan to utilise a $30bn equity line of credit from the Exchange Stabilisation Fund (in effect FX reserves) to juice a $300bn corporate lending program, On top of this there is the resurrection of the TALF (Troubled Asset Loan Facility) that will facilitate the purchase of securities backed by student, car and credit card loans. The list here isn’t exhaustive.

The good news out of Germany is that the government has announced plans for supplementary budget that suspends the constitutional balanced budget law and allows for more than €750bn of new debt, with a €600bn rescue fund to provide troubled companies with loans and guarantees and taking on equity stakes if required. Another £156b will be set aside for social spending and company aid. Also, Bloomberg reported that Germany is ready to back a rescue plan to help Italy weather the crisis, with an emergency loan from the euro area’s bailout fund (with minimal conditionality). This could pave the way for unlimited purchases of Italy’s debt via the Outright Monetary Transactions (OMT) programme, designed during the GFC but never used. Germany now gest it. Hurrah. Incidentally, chancellor Merkel has reportedly tested negative for COVID-19.

‘Flash’ Markit Phi’s from Germany, France, pan-EZ, UK and the US will give us the first tangible indication of the depths to which manufacturing activity has already crunched before Q1 is over (with particular interest in what order books look like). Germany is forecast at 40 from 48 in February, EZ at 41 from 49.1; UK 49 from 51.7 and US 45 from 50.7 but no one will be surprised if the reality is much worse than this. If nothing else, this helps policy makers further frame the extent of the policy responses required as more nd more countries go into lock-down. UK PM Boris Johnson is about to speak in this. regard.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.