Online retail sales growth slowed in May following a fairly strong April

Insight

China’s burst of confidence, irrespective of trade talks, is helping the Aussie dollar, but will it continue if the uncertainty continues?

https://soundcloud.com/user-291029717/trump-and-china-prepare-for-the-long-game

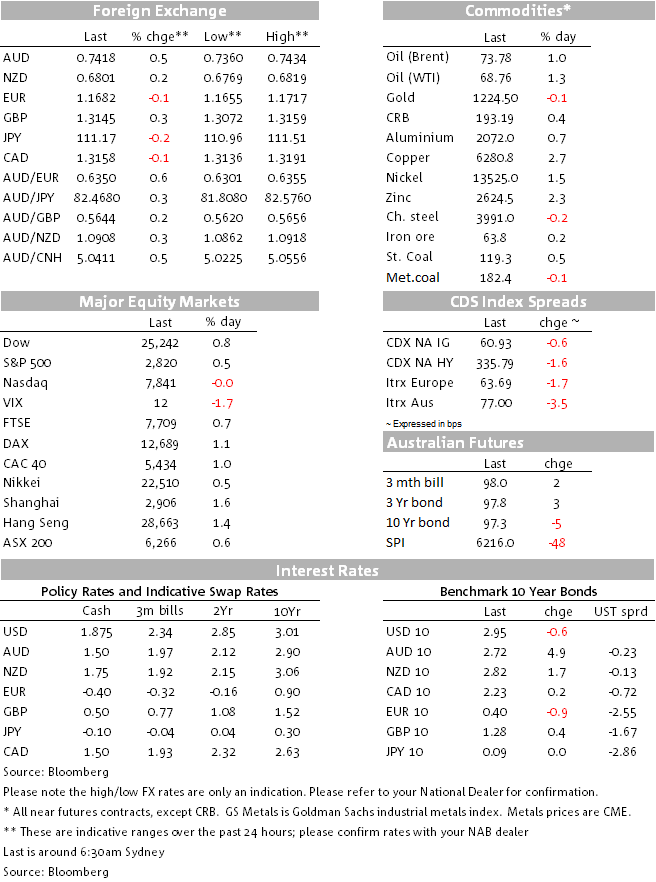

Global equities recorded gains overnight boosted by a positive lead from Asia with the Shanghai Composite leading the way following the announcement of additional stimulatory measures from China late on Monday. US earnings results also boosted US equities, although after a solid start the tech heavy NASDAQ closed flat for the day. China’s news also boosted commodities and helped the AUD climb to the top of the G10 leader board. Core global yields had a stable night, but longer dated JGBs remain under pressure.

The improvement in risk appetite that began during our session yesterday came off the back of news late on Monday that China had unveiled a package of targeted policies to boost domestic demand intended to form a more flexible response to “external uncertainties”. This when combined with recent policy easing steps suggest China is undertaking a co-ordinated stimulus in response to trade tensions. Meanwhile, overnight the Trump administration announced an emergency-aid package of $12bn for farmers aim as an offset from China’s trade retaliation. Ahead of the farmers relief news, President Trump toughens his trade stance in a series of tweets noting that “Tariffs are the greatest! Either a country which has treated the United States unfairly on Trade negotiates a fair deal, or it gets hit with Tariffs” . Then speaking in Kansas and ahead of trade talks with Europe tonight the president said that “What the European Union is doing to us is incredible, how bad,” , “They sound nice but they’re rough.”

So although equities and risk assets in general enjoyed a good night, like Bob Dylan would sing, it seem that the masters of war are gearing up for battle. China on the one hand looks to be playing the long game, introducing stimulatory measures while also showing tolerance to CNY weakness. China’s equity markets is starting to show some stability and the negative side effects from CNY weakness are seemingly contained for now as there is no evidence of capital outflows typically associated with a currency crisis. Meanwhile president Trump is not only amping up the rhetoric, he has now also introduced offsetting measures against China’s retaliation. The threat of even larger tariffs is keeping the market weary and it doesn’t seem like anyone will be blinking any time soon.

After a positive lead from Asia (Shanghai Composite 1.61%) and Europe, the S&P 500 gave up some of its early session gains, but still managed to close the day up 0.48%. The NASDAQ made a new record high, supported by better than expected earnings from Alphabet (Google) after the bell yesterday, but it was unable to sustained the move retreating half way through the session and closing flat for the day. All major European equity indices recorded gains overnight with the DAX leading the way, up 1.12%

USD indices are little changed after recovering following the Trump’s administration offer to help US farmers. AUD is the outperformer in G10, +0.47%, following China’s news and a decent night for commodities. AUD now trades at 0.7424 and is still within its 0.7311-0.7484 range held since mid-June.

The CNY itself is also marginally stronger on the day, with the USD/CNY just below 6.80, although it remains near its weakest levels since June last year.

The EUR is slightly lower than this time yesterday, with the European manufacturing PMI increasing slightly while the Services equivalent showed a small fall. The manufacturing PMI remains well below the levels reached late last year, indicative of the European economy losing some momentum, but it remains at healthy levels overall. ECB meeting tomorrow will be the focus for the euro.

Core bond yields were reasonably stable overnight, after relatively large rises over the preceding two days. The 10 year Treasury yield is down 1bp at 2.95%. The 10 year JGB remained at 0.075% although the 30 year JGB moved another 3bps higher to 0.798%.

Copper and Zinc have led the gains in commodities, both up more than 2% with Aluminium and oil prices up just under 1%. Iron ore was essentially unchanged and gold was a smidgen softer, down 0.11%.

EC: Manufacturing PMI, Jul: 55.1 vs 54.7 exp.

EC: Services PMI, Jul: 54.4 vs 55.1 exp.

US: Manufacturing PMI, Jul: 55.5 vs 55.1 exp.

US: Services PMI, Jul: 56.2 vs 56.5 exp.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.