A major global investment fund is using NAB’s financial innovation for derivative portfolios to help incentivise sustainability goals in a new deal for the Australian market.

Article

The Trump administration announces an end to waivers for nations buying Iranian oil.

https://soundcloud.com/user-291029717/trumps-blanket-ban-on-iranian-oil

Now don’t be sad ‘cause two out of three ‘aint bad – Meat Loaf

Quite a lot of economic news has flowed under the bridge since we departed for Easter or Passover, and tragically more appalling terrorism news as well.

In the middle of last week we had unequivocally good news from China via evidence of a sizeable rebound in industrial activity and retail sales in March and which followed on from earlier reported strong credit data and PMIs readings. Then on Thursday night the US produced some eye-popping retail sales figures (as did the UK earlier in the night). US retail sales printed 1.6% in headline terms and 1.0% m/m for the so-called ‘control group’ that feeds directly into the consumption component of GDP. The latter is due out of Friday and together with smaller than expected US trade deficits reported thus far in Q1, has seen analysts leaping to upgrade forecast for the Advance estimate of GDP. Bloomberg currently have 2.2% for the consensus, which incidentally would match the Q4 2018 actual outcome despite the fact the US government was shut for virtually the whole of January. Meanwhile the Atlanta Fed’s GDPNow estimate was ratcheted up to 2.8% after the retail sales report and is still there after Friday night’s residential construction report.

In contrast to the evident pick up in US and China activity since the turn of the year, the news out of the Eurozone continues to be little short of depressing. Thursday saw preliminary PMI data covering both services and manufacturing for Germany, France and pan-Eurozone, none of which painted a pretty picture. France and Germany’s composite readings crept up but only to 50.0 (from 48.9) and 52.1 (from 51.4) respectively, but the pan-Eurozone PMI actually fell back, to 51.3 from 51.6, implying that other parts of the Eurozone – likely Spain and Italy to name but to – went backwards. “The Eurozone is not Germany” as my research partner in crime Rodrigo Catril frequency reminds me. And in Germany, incidentally, the auto sector continues to be singled out for weakness within the manufacturing PMI. New diesel car anyone?

Local news on Thursday we headed for the door was the March labour force survey, that saw a strong 25.7k headline employment print but tick up in unemployment to 5.0% from 4.9% – and a ‘high’ 5.0% at that, being 5.0475% unrounded. Still, not high enough to have the ABS determining that unemployment was anything other than still steady at 5.0% in trend terms, while the uptick was in part due to more folks entering the labour force last month (the participation rate printed 65.7% from 65.6%). As such, one of the RBA’s two stated preconditions for lowering rates – a rise in unemployment in trend terms – has not been met, even if the other – lack of progress towards achieving the 2-3% inflation goal – may well be tomorrow when Q1 CPI is reported.

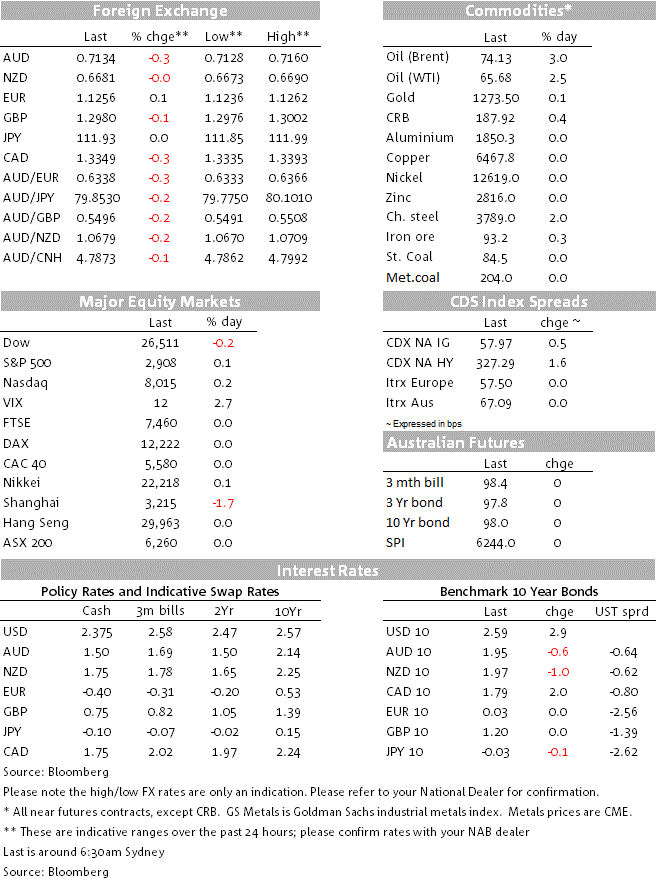

The other big economic news since we broke up is oil related, President Trump announcing on Monday that the waiver from sanctions against countries importing Iranian oil will not be renewed come May 2nd. The waivers, that apply to a swathe of prior importers of Iranian oil include China, India, Japan and South Korea, have allows Iran to continue exporting some 2.7 million barrels of oil a day as of March and Trump now want to reduce this to ‘zero’. On top of the ongoing decline in Venezuelan production and fears of Libyan supply disruptions, the risk of supply shortfalls have so far outweighed the apparent pledge from other OPEC+ producers to make up any shortfalls created by loss of Iranian supply. Brent crude is up over 3% at $74.14 as I write and WTI crude by 2.66% to $65.70.

Were it not for the boost to the energy sub-sector (+2.05%) the S&P500 would have finished in the red, rather than the meagre 0.1% gain it has otherwise chalked up. Earlier, European bourses were all still shut. Japan was open yesterday of course where the Nikkei finished close to flat, but Shanghai was off 2. 3%. Japan CPI was out of Friday, and again how scant evidence of progress toward the 2% target. The core (ex-fresh food) measure ticked up to 0.8% from 0.7% and headline to 0.5% from 0.2% (as expected) but the ex-fresh food and energy (‘core-core’) measure stuck at 0.4%. The BoJ meets on Wednesday and Thursday.

In FX, the AUD has been among the poorest performing G10 currencies on Monday having essentially flat-lined on Friday, off 0.25% to 0.7133 (so continuing the weaker trend evident on Thursday afternoon after a fleeting gain on the headline Oz employment print). In contrast CAD and NOK have fared best on the back of the oil price pop, CAD + 0.33% and NOK +0.17%. There’s very little to note elsewhere, save that the USD is still higher, benefiting from Euro weakness after the Eurozone PMI data and the strength of US retail sales on Thursday, albeit now back a little from Thursday night’s highs.

In bonds, US treasury yield have retraced the 3bp loss seen on Thursday (market was shut on Friday) so back to 2.59%. This is mostly a real yield rise, with 10 year break-evens up less than 0.5bp despite the jump in oil prices.

GE: Markit manufacturing PMI, Apr: 44.5 vs. 45.0 exp.

GE: Markit services PMI, Apr: 55.6 vs. 55.0 exp.

EC: Markit manufacturing PMI, Apr: 47.8 vs. 48.0 exp.

EC: Markit services PMI, Apr: 52.5 vs. 53.1 exp.

UK: Retail sales x auto fuel (m/m%), Mar: 1.2 vs. -0.3 exp.

US: Retail sales x auto, gas (m/m%), Mar: 0.9 vs. 0.4 exp.

US: Philly Fed business outlook, Apr: 8.5 vs. 11.0 exp.

US: Markit manufacturing PMI, Apr: 52.4 vs. 52.8 exp.

US: Markit services PMI, Apr: 52.9 vs. 55.0 exp.

JN: CPI ex fresh food (y/y%), Mar: 0.8 vs. 0.7 exp.

US: Housing starts (k), Mar: 1139 vs. 1225 exp.

US: Building permits (k), Mar: 1269 vs. 1300 exp.

US: Existing home sales (m), Mar: 5.21 vs. 5.30 exp.

Today, nothing of note in our time zone and tonight Just US house prices (FHFA version), US new home sales and the Richmond Fed manufacturing index.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

A major global investment fund is using NAB’s financial innovation for derivative portfolios to help incentivise sustainability goals in a new deal for the Australian market.

Article

Price growth edges lower despite reasonable economy

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.