Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

US equities have had a third session with substantial falls.

https://soundcloud.com/user-291029717/us-equities-hit-again-boris-and-donald-play-tough-guys?in=user-291029717/sets/the-morning-call

Oh when it all, it all falls down, I’m telling you oh, it all falls down

Oh when it all, it all falls down, I’m telling you oh, it all falls down – Kanye West

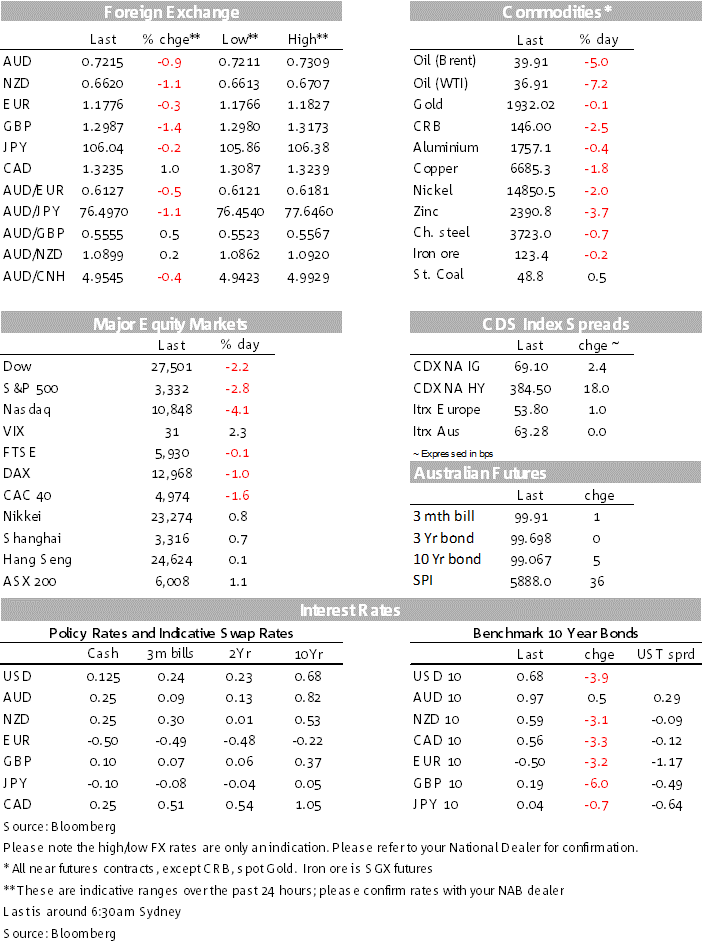

The US tech led equity rout has extended into a third day, wrong footing European equity investors that had began the new week with a spring in their step. Big slip up in oil prices added to the negative vibes with the energy sector feeling the pain.

The broad risk off environment supports the USD and bull flattens the UST curve. NOK the big G10 underperformer, AUD (-0.9%) and NZD (-1.15%) also under pressure.

Well after President Trump’s hard rhetoric on China (and Biden) late on US Labour Day, yesterday US equity futures did not show much of a reaction to the President’s comments during the APAC session. In the end that proved to be a red herring,

European equities opened the overnight session with a cautious tone while weakness in oil prices also weighed on the energy sector. By the time US equity investors were getting ready to start the new week, the Euro STOXX 50 index was down more than 2% and so amid a rude awakening, US equity shares gapped lower at the open.

The S&P 500 has ended its Tuesday session down 2.78% with the IT sector down 4.59% while the energy sector was not too far behind down 3.71%. Apple ( -6.73%) and Microsoft (-5.41%) shares were amongst the big losers, but Tesla took the price amongst the current equity darlings, down 21%.

GM shares jumped 7.9%, following news the car maker will take a $2bn equity stake in Nikola aiming to engineer and manufacture electric pickups. The NASDAQ close the day down 4.11% while the Stoxx Europe 600 Index ended 1.2% down, paring a slump close to 1.9% early in the session.

Falls in energy shares can be largely attributed to a collapse in oil prices. After chunky falls in oil prices last week, WTI crude is down another 7.37% to USD36.84 and Brent crude down 5.19% to USD39.83. Demand has fallen away after a period of Chinese re-stocking, US gasoline demand is down about 10% y/y and at the same time OPEC production is lifting.

President Trump stepped up the rhetoric against China and Biden. Giving us a flavour of what his second term could entail, the President said he intends to unwind the US economic relationship with China, contrasting himself with Joe Biden by threatening to punish any American companies that create jobs overseas and to forbid those that do business in China from winning federal contracts. “If Biden wins, China wins because China will own this country,” Trump said. “It’s the most important election in our history, right now, most important election in our history. Under my administration we will make America into the manufacturing superpower of the world and we’ll end our reliance on China once and for all.”

This morning Bloomberg reports the Trump administration has banned imports from three companies in the Xinjiang region of China over Beijing’s alleged repression of the Uighur Muslim minority group, and it plans to add curbs on six more firms and target cotton, textiles and tomatoes from the area. Orders against the six will come by the end of this fiscal year, the CBP said

Core global bonds have been well bid overnight with UK Gilts leading the decline in Europe, down 6bps to 0.186% while 10y Bunds fell 3bps to -0.497%. The move lower in UST yields has been led by the back end of the curve, the 30y Bond is down 5bps to 1.422% while the 10y Note is -3.8bps to 0.68%.

The broad risk aversion sees the USD stronger across the board with JPY (0.23%), the preeminent safe haven the only pair to outperform the USD (USD/JPY now trades at ¥106.02).

The big slide in oil prices sees NOK (-2.21%) at the bottom of the G10 board with other commodity linked currencies down about 1%. AUD opens the new day at 0.7214 while NZD is at 0.6619, both antipodean currencies are trading close to their overnight lows.

Sandwiched between NOK and other commodity linked currencies underperformance, GBP is down 1.37% and back trading below the 1.30 mark. In addition to the risk off environment, cable has also come under pressure amid heightened uncertainty over the future of the UK and EU trade relationship following the UK PM’s evident willingness to “move-on” next month if there is no break-through in negotiations.

The key sticking point seems to be the UK government’s vision to turn the UK into an attractive base for tech companies by easing regulation, taxation and subsidising promising businesses (ie. “picking winners”). The EU doesn’t want Britain subsidising businesses that then get tariff-free access to its market. Talks continue this week to break the deadlock.

But for the record, the NFIB small business optimism index rose to 100.2 in August, from 98.8 in July, above the 99.0 consensus. The hiring plans component was 21, versus 18 in July and 21 in February; it averaged 19 in 2019.

The US reported fewer than 25,000 new cases of COVID-19, the lowest daily total in nearly 12 weeks, while the 7-day average was around 38,000, the lowest since late-June. In contrast, France and Spain are witnessing close on 10k new daily cases, while the UK has 6k over two days, prompting warnings from the WHO and UK government scientists. But it is India, which is seeing circa >80k new cases per day, to a total of over 4mn, that is the global worry.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

Conditions ease as slow growth weighs on firms

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.