We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Markit PMIs show US manufacturing has contracted, whilst in Europe it remains in a slump but hasn’t fallen as far as anticipated.

https://soundcloud.com/user-291029717/all-eyes-on-powell-manufacturing-weak-in-us-and-europe?in=user-291029717/sets/the-morning-call

Ahead of a very keenly anticipated opening keynote speech from Fed chair Jay Powell at midnight AEST from Jackson Hole, billed as “Challenges for Monetary Policy” but which is merely the title of the symposium itself, incoming Fed speak is increasingly at odds with market pricing which continues to see 100bps of additional Fed easing between now and the end of 2020.

Philadelphia Federal Reserve President Patrick Harker said in an interview on CNBC from Jackson Hole that “I think we should stay here for a while and see how things play out” and that he supported the Fed’s July 31 rate cut “somewhat reluctantly”.

Earlier, Kansas Fed President Esther George (the host of the Jackson Hole symposium and who did support the July Fed cut) told Bloomberg TV, “As I look at where the economy is, it’s not yet time. I’m not ready to provide more accommodation to the economy without seeing an outlook that suggests the economy is getting weaker”.

And earlier in the week, recall, Boston Fed President Eric Rosengren – who dissented against the July cut – said he didn’t support additional rate cuts, while San Francisco Fed President Mary Daly said her support for the Fed’s July rate cut did not reflect concern about an impending economic downturn, rather it was aimed at extending the expansion.

Against this backdrop, and where a September 25-point rate cut remains fully priced, interest in the Powell speech will be in whether he maintains the line that last months’ action represented no more than a “mid-cycle” adjustment or “insurance” cut, following the escalation in the trade war – the ‘10% tariffs on $300bn” hasn’t been announced at the time – and flattening/inversion in the US yield curve. We presume Powell will want to convey an open-minded view about the outlook for monetary from here without pre-committing to any set course, but whether he will be suitably dovish enough for the market will be key to the market reaction.

In the meantime POTUS continues to rail against the Fed, Tweeting “Germany sells 30 year bonds offering negative yields. Germany competes with the USA. Our Federal Reserve does not allow us to do what we must do. They put us at a disadvantage against our competition. Strong Dollar, No Inflation! They move like quicksand. Fight or go home!”.

Usual bluster you might say, but it serves as reminder that the potential for Trump announcing intent to impose tariffs on auto and/or other European imports later this year is far from trivial.

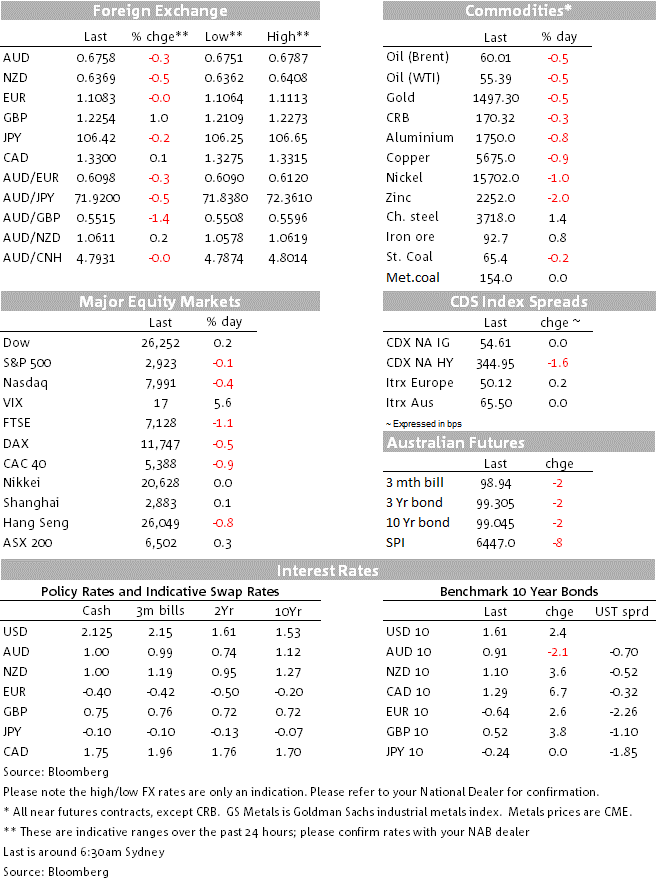

Latest Fed speak hasn’t been completely lost on the US bond market, the Treasury curve undertaking some fresh bear flattening, 2-year yields +4bp to 1.61% and 10s + 2s +2.5bps to 1.615%. In Europe, we’ve seen a further reaction to yesterday’s less-than-stellar 30-year bond offering, the yield here up another 4bps to -10.5bps. It was closer to -30bps in the lead up to the sale.

There’s been a bit of EUR volatility in the FX market, first up then back down, following first the ‘flash’ Eurozone PMI data. This came in fractionally better than expected, albeit in the case of the German manufacturing index the 43.6 reading (up from 43.2) means no more than that the sector is continuing to implode at a marginally less rapid rate. German services at 54.4 was better than the 54.0 expected but still down on July’s 54.5. France was appreciably better on both manufacturing and services (51.0 from 49.7 and 53.3 from 52.6 respectively) and because of this, the pan Eurozone Composite measure rose to 51.8 from 51.5.

EUR/USD rose from 1.1075 to above 1.11 on the PMI data, before more than fully retracing the gains on the publication of the record of the ECB’s 25th July meeting. This included a line that “the view was expressed that.. various options should be seen as a package, i.e. a combination of instruments with significant complementarities and synergies, since experience had shown that a policy package — such as the combination of rate cuts and asset purchases — was more effective than a sequence of selective actions.”

Whether or not this is broadly held view on the Governing Council and consistent with Finnish central bank governor Ollie Rein’s WSJ interview last week that the Journal depicted as “ECB Has Big Bazooka Primed For September”, remains to be seen. Current market consensus appears to be for a 10bp cut to the (currently -0.4%) Deposit Rate and a new QE asset buying programme of around €40bn per month. It will now need to be more than this if the Euro is to come to much (intended) harm on September 12th.

Elsewhere in FX, the NZD made a new post-January 2016 low yesterday (to 0.6363) and AUD fell from 0.6780 to a low of 0.6751, both in direct response to latest slippage in the Chinese Yuan. The offshore CNH has risen from 7.07 to 7.10 in the last 24 hours (7.09 now) and USD/CNY from 7.06 to a high of 7.095. So both to new highs after the Yuan started dropping shortly before Trump announced the intent to impose 10% tariffs on all remaining Chinese imports not currently subject to tariffs. There has now been a cumulative depreciation of about 3.5%. Expectations of additional Yuan weakness is the bedrock for our recently downgraded forecast for AUD and NZD. We have no strong reason to question them at this stage.

GBP is the biggest G10 currency mover of the past 24 hours, GBP/USD up over 1% to 1.2260. UK PM Johnson continued with his European tour, this time meeting with French President Macron, who didn’t sound convinced that a new EU Withdrawal Agreement could be drafted, saying that any renegotiation would leave it little changed from the original. However, he did say that he was “confident we can find something intelligent in 30 days”, referencing the timeline given by Chancellor Merkel yesterday for Johnson to find an impasse to the Irish Border issue. Merkel clarified her comments and said overnight that “One should say it can be done by 31 October…it can be done in a short time period, because the UK have said they want to leave the EU by 31 October”. The market has seized on these comments as a positive development, showing a will to negotiate and GBP leapt higher and has sustained that move. Heavy short positioning probably explains the move, which magnifies any hint of positive Brexit news.

US equities fell away in early day trade following poor US PMI data – the Markit version, less favoured than the ISM series but no less potent as a leading indicator of activity. Manufacturing fell to 49.9 from 50.4 (the first sub-50 read of the cycle) and services to 50.9 from 52.6. These are significant falls. Stocks nevertheless recovered to close little changed (S&P flat, Dow +0.2% and NASDAQ -0.4%).

As well as Powell at Jackson Hole, RBA’s Governor Lowe is appearing on a panel from 2:35 AEST Saturday

Data wise today, its just Japan CPI, Canada Retail Sales and US New Home Sales

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.