NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Equities in Europe are on the rise. Equities in the US are on the slide.

https://soundcloud.com/user-291029717/us-and-europe-two-sides-of-the-same-coin?in=user-291029717/sets/the-morning-call

You’re not the only one with mixed emotions

You’re not the only ship adrift on this ocean – Rolling Stones

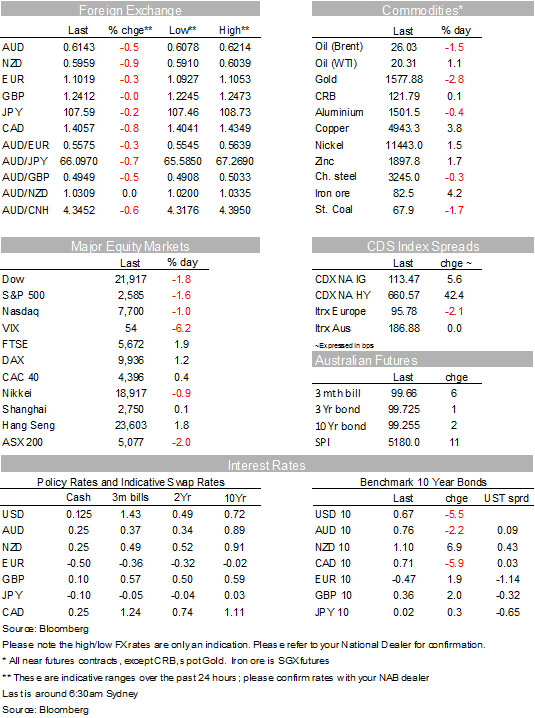

While calmer relative to recent days, it has certainly been a night of mixed signal from markets. European equities have ended the month higher despite talks of an extension of COVID-19 containment measures and US equities are lower notwithstanding President Trump push for infrastructure package and deferral of tariffs. UST yields are a bit lower while core EU yields are higher. The USD is little changed in index terms but NZD and AUD are the big underperformers, down 0.9% and 0.5% respectively. Meanwhile Commodities and Credit markets are signalling a risk positive mood, Month/Quarter end rebalancing flows have likely played into the overnight mixed emotions from markets.

US stocks are down between 0.9% and 1.35% as I type while European equities closed higher with the Stoxx Europe 600 index up 1.7% on the day. Looking at the quarter performance however the Stoxx Europe 600 index is down 23% while the S&P is close to -20%. Market moves have been a bit more subdued relative to recent days, the VIX index, a measure of volatility, has fallen to its lowest level in 3 weeks, just above 50. So still at a pretty elevated level and with COVID-19 uncertainties likely to linger for some time we should expect market volatility to remain high for some time too.

There have been further signs of stabilisation in the number of new cases in Italy, suggesting that the lockdown implemented by the Italian government is starting to work. There were 4,053 new cases in Italy over the past 24 hours compared with 4,050 the previous day. However, Spanish numbers have continued to rise, the number of new cases increased by 9,222 — the most in a single day — to bring total confirmed infections in the country to 94,417. Sadly Europe’s death toll is also depicting a grim story, meanwhile from an economic perspective Italy and the Netherlands are discussing prolonging measures to limit personal contact, and German officials warned that it’s too soon to ease restrictions as things could still get worse . Italy’s PM said the government may extend restrictions through the May 1 holiday weekend, with a gradual opening of the country from May 4.

COVID-19 cases continue to rise sharply in the US, although Dr Fauci, the US medical specialist, said “we’re starting to see glimmers … just the inklings” that the social distancing measures were limiting the rise in new cases. But he cautioned that “we’re not seeing (a turnaround) yet.”. Overall there seem to be an increasing risk that markets are underestimating the length containment measures will be implemented across the globe. China and now Italy are also showing that the removal of these containment measures will be slow. Finally anecdotal evidence from China also shows the Consumer has turn increasingly cautious, the uptick in activity as shown in the official China PMIs yesterday are good news, but without a buoyant consumer, it is unlikely that we will get a strong and swift recovery.

So bearing that in mind the good news is that more monetary and fiscal stimulus is on its way. The US Federal Reserve has unveiled yet another new liquidity measure, called the FIMA Repo Facility, which provides US dollar funding to foreign central banks and international monetary authorities in exchange for US Treasuries. The measure appears most useful for those central banks with large stockpiles of US Treasury foreign reserves, which can then lend the cash to their businesses and financial institutions needing USD funding. USD Libor-OIS has shown signs of stabilising at a still-high 136bps, although the market expects this spread to contract rapidly over the coming quarters, to 46bps by mid-June and 26bps by the middle of December. The cost of borrowing USD via EUR/USD and USD/JPY FX swaps continues to fall, in a further sign that funding pressures are abating.

Trump is pushing for more stimulus, tweeting that the US should implement a $2 trillion infrastructure bill (~10%/GDP). Democrats have, for some time, pushed for more infrastructure spending so Trump’s proposal could get bipartisan support. In Japan, the government proposed a ¥60 trillion stimulus package (11%/GDP), including more than ¥10 trillion allocated towards cash, subsidies and coupons handed out to households. ¥40 trillion would be used to provide subsidies and funding to firms. The proposed Japanese stimulus would be bigger than its GFC response.

Tthe New Zealand Government updated its 2019/20 Bond Programme Increased to NZ$25bn, that is NZ$12 billion higher than the forecast NZGB programme, updated on 17 March 2020. Bloomberg also reports that the New Zealand government has tasked a group of industry leaders to seek out infrastructure projects that are ready to start as soon as the construction industry returns to normal to reduce the economic impact of the COVID-19 pandemic. This programme is in addition to the NZ$12b infrastructure plan announced previously.

Despite the prospect of even greater fiscal spending (and with it, huge amounts of government bond issuance), US Treasury yields have fallen overnight. The 10-year rate is down 7bps to 0.65%. Fed QE purchases continue to provide an important support to the market. The current pace of Fed purchases ($75b per day) is enormous. For context, the Fed purchased $85b per month (across US Treasuries and MBS), when it last implemented QE in 2013. Meanwhile core European bond yields also drifted lower with the 10y Bund and 10y Gilts, both down 3bps to -0.477% and 0.349 respectively.

News that the Fed increased repo funding for foreign central banks didn’t have much of an impact on the USD, after an u and then down session the USD is little changed in index terms. Month/Quarter end flows have likely played their part in the price action overnight blurring the picture and thus making it hard to discern whether macro news have influenced currency movements. USD/JPY is a tad lower at 107.55, after trading to an overnight high as 108.73. The euro has ended the day a bit lower at 1.1025, but that is after trading down to1.0927 just before midnight.

The NZD (@0.5959) and AUD (@0.6143) are the big underperformers, down 0.9% and 0.5% respectively. This despite the fact the commodity complex had a pretty good 24 hours with copper (3%), metal prices (2.2%) up while gold is down 2.5%.Yesterday both antipodean currencies were pretty stable post some volatility at the Tokyo fix, both decline after the European open ( NZD low of 0.5910, AUD low 0.6023) and have regained a bit of grown over the past couple of hours.

Bloomberg has reported that President Donald Trump has approved a proposal for by some businesses to delay payment of certain tariffs by three months.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.