Online retail sales growth slowed in May following a fairly strong April

Insight

The inoculation program in the US has ambitious targets.

https://soundcloud.com/user-291029717/us-in-warp-speed-whilst-uk-dithers?in=user-291029717/sets/the-morning-call

“Run, run Rudolph, Santa’s gotta make it to town; Santa, make him hurry, tell him he can take the freeway down; Run, run Rudolph ’cause I’m reelin’ like a merry-go-round”, Chuck Berry 1958

What does “Run Rudolph Run ” share with “Johnny Be Goode” aside from both being Chuck Berry classics? Both allude to very favourable weekend events that should see a very positive open in what is a big week for data and events as we head into Christmas (only 11 days to go!). PM Johnson and the EU’s von der Leyen agreed to extend their Sunday deadline following “genuine progress” with GBP up some 1% this morning and more than reversing the weakness seen on Friday. Also adding to the mix was the US FDA granting emergency use authorisation to the Pfizer/BioNTech vaccine on Friday. 2.9m doses are set to be shipped across the US with some available for use as soon as Monday. Rounding out the trifecta are signs compromise emerging last minute in US fiscal negotiations with some Democrats willing to drop their insistence on state and local aid (a key Republican deal breaker; see Politico for details).

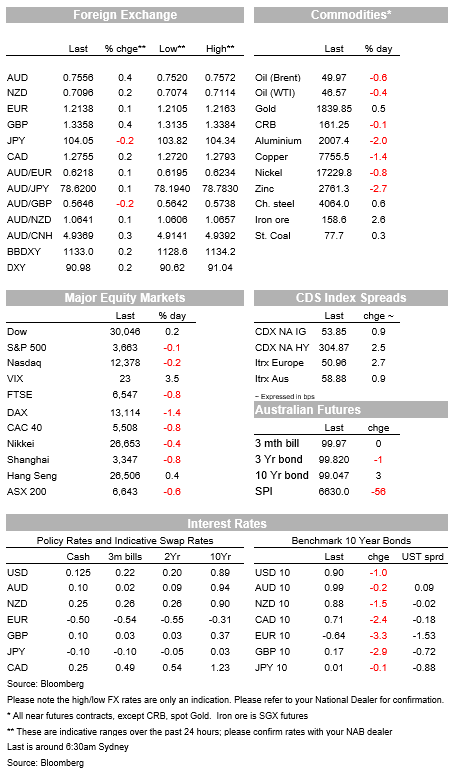

Market moves on Friday largely pre-date the positive news flow (apart from the vaccine approval). Equities on Friday fell marginally with the S&P500 -0.1% given the uncertainty on a fiscal stimulus plan. GBP fell as much as 1%, before paring losses to be down some -0.6% with Sunday’s deadline approaching. EUR fell -0.2% in sympathy with the USD up (BBDXY +0.25%), though the secular trend remains overwhelmingly of US dollar weakness. JPY outperformed amidst the softer tone to equities, while US Treasury yields fell 1bps to 0.90%. All those moves will likely change direction given the more positive risk tone, though markets are still likely to be cautious ahead of key risk events, including the FOMC on Wednesday and on whether Congress can agree to a US fiscal stimulus package by Friday (see Coming Up for details).

The AUD continues to leap, trading above 0.7570 during Asia on Friday, helped along by the rise in commodity prices over the past week and the surge in the iron ore price due to a number of factors including weather in Port Hedland. Iron ore spot prices rose above $160 a tonne on Friday. The AUD was the top performer over the week, up 1.5%. Like the AUD, NZD made a new post-2018 high on Friday afternoon, above 0.71 before turning lower in London. As trading opens for the week, the AUD is back marching higher, currently at 0.7555.

As for US fiscal stimulus news, last minute signs of compromise are emerging despite little progress having been made on Friday. Politico reports House Democratic Majority Leader Hoyer has flagged dropping a key Democratic proviso of providing aid to the states and local authorities in favour of getting a deal done (or in the words of that well-worn cliché: “you can’t let the perfect be the enemy of the good . Last week Republican Senate Majority Leader McConnell has said he would be willing to drop his instance of a proposed liability shield for businesses. If a deal can be reached by Friday, that will provide a further boost to risk appetite and build the bridge to what is a more optimistic medium-picture given the rollout of a vaccine in the US.

The other political risk for markets (particularly for rates) that we won’t know about until the New Year are the Georgia Senate run-offs, where the run-offs will decide which party has an effective Senate majority (Democrats need to win both races). Polls are pointing towards a close race with FiveThirtyEight marginally having both Democratic candidates in the lead (see FiveThirtyEight for details ), while betting markets are still favouring Republicans to win (PredictIT has Democrats at a 32% chance). Also in politics, the Electoral College meets today and should formally elect Joe Biden as the next President.

As for vaccine news, the US FDA on Friday gave emergency use authorisation for the Pfizer/BioNTech vaccine with 2.9m doses being shipped across the US with some available for use as soon as today (another 2.9m doses will come 21 days later for patients to get their second shot). Operation Warp General Perna said around 40m doses could be available by the end of the year (meaning 20m could be vaccinated), while also noting an aim to vaccinate 75-80% of the population by June. More positive news flow is likely on this font with Moderna’s vaccine likely to receive emergency use authorisation by Friday. Closer to home, Australian Health Minister Hunt has indicated approval could be given to the Oxford/AstraZeneca vaccine in early January (the AFR reports 3.8 million does would be available in early 2021, while a further 50m would be produced onshore by CSL). Such a rollout would be around 6 months earlier than projected in the October Budget and would present an upside risk to the economy, especially if international tourism and education could be more comprehensively restarted.

The final piece to the trifecta of positive news was the EU and the UK agreed to extend trade talks (again), averting near-term risks of a hard exit, though it still not clear what the chances are of a deal. PM Johnson is still cautioning that the “most likely” scenario was still a no-deal outcome, while UK media have taken a more optimistic interpretation amidst reports that compromises had been made on the longstanding issue of “level playing field” conditions. The Telegraph quoted EU sources as claiming that “genuine progress” had been made in weekend negotiations. GBP has opened sharply higher this morning, up around 1% to 1.3366. The GBP fallen by as much as 1.2% before paring about half that loss. The GBP was the clear underperformer last week, losing 1.6%.

Finally, data on Friday was mostly second tier, US Core PPI missed by a tenth with Core PPI up 0.1% m/m against 0.2% expected. US Consumer Sentiment on the other hand bounced more strongly than expected, possibly due to vaccine-fuelled gains in the stock market and election certainty, with the headline index rising to 81.4 v. 76 expected and up from 76.9 previously.

A big week ahead with Aussie Jobs, MYEFO and RBA Minutes, while offshore there is the FOMC, BoE, BoJ, New Zealand Q3 GDP, and China activity indicators. Details below:

A quiet day today with little in the way of market moving data scheduled. NZ has the Performance of Services Index, Japan the Tankan and Industrial Production.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.