Online retail sales growth slowed in May following a fairly strong April

Insight

US jobs data on Friday helped the equities market to regain a little composure as it fell for the second day.

https://soundcloud.com/user-291029717/us-jobs-coming-back-but-harder-from-here?in=user-291029717/sets/the-morning-call

This Week

Harder than you think, its a beautiful thing

(Hard) Get up, Just like that, (Hard) Get up, Just like that – Public Enemy

US and European equities posted a second day of negative returns, although losses were paired after US payrolls print inline with expectations, but the unemployment rate falls by more than expected. Speaking late in the session, Fed Chair Powell gave a sobering assessment of the recovery, improvements from here will be harder to come by and interest rate will stay low for a long time.

Following the US Labour market report and ahead of big issuance this week, the UST curve bear steepened aggressively, the USD appreciated on the report, but as equities recovered, the greenback gave back its gains. AUD and NZD ended Friday little changed, after and up and down session. Over the weekend the WSJ reported the Trump administration is considering imposing export restrictions on China’s semiconductors, a move that would further intensify tensions between the two nations.

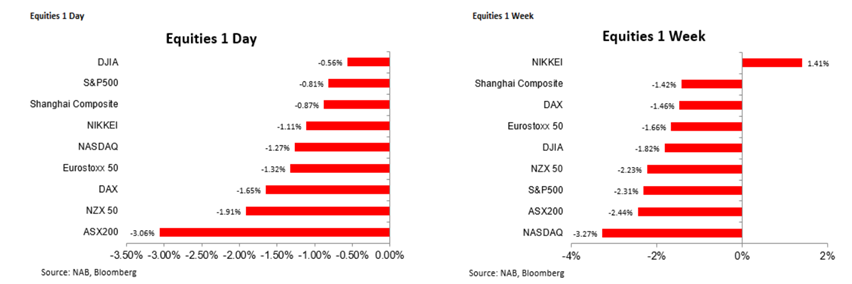

Last week’s Thursday’s and Friday’s declines for S&P 500 and NASDAQ were too much, with both indices ending the week on the red. The S&P 500 closed Friday down 0.6% and the NASDAQ fell 1.3% and for the week the aggregate losses were 2.31% and 3.27% respectively. Things could have been worse with Thursday’s sell off extending aggressively early on Friday session, the S&P500 was down over 3.5% at on stage while the NASDAQ was down over 5%.

A better than expected US labour market report and comments from Fed Chair Powell (more on both below) supported the U turn in sentiment while buying the dip mentality probably also helped. The FT reported that this previous run-up had been exacerbated by large-scale purchases of call options in single-name tech stocks by Japanese investor Softbank, which in turn led to buying of these stocks from dealers looking to hedge their exposures.

The notion that the recovery is on a strong footing and that monetary policy will remain accommodative for a “loooong” time were reinforced on Friday.

US payrolls printed in line with expectations, but the unemployment rate fell by more than expected. August payrolls rose 1.37m, a smidge above the consensus, 1.35m and the unemployment rate dropped to 8.4% from 10.2%, well below the consensus, 9.8%.

Details of the report were not as encouraging as the headline, the payrolls number included 344K jump in government employment, mostly delayed hiring for the Census while private payrolls disappointed coming at 1.027m vs 1.352 expected. The fall in private hiring from 1.5m jobs in July was seen as a sign that employers remain wary with the virus still not under control.

The unemployment rate comes from a separate survey of households, which tends to be more volatile than the payrolls survey of employers, so it likely exaggerates the improvement in the labour market, specially once we consider the slowing in the rate of decline of jobless claims.

This idea of a slowdown in the momentum of the recovery (also evident in real time indicators) was highlighted by Fed Chair Powell. Speaking to National Public Radio after the payrolls report, Powell welcomed the labour market report as a positive outcome, “Today’s jobs report was a good one,” he said, but then cautioned that “to get us back to full employment, we’re going to have to get the disease under control.” Adding “The recovery is continuing; we do think it will get harder from here,”. Powell reiterated that interest rates would remain low for a long time (“it will be measured in years”), adding that “it’s likely we will need to [take more stimulus measures] over time.” .

While politicians may see solid data releases as easing the pressure on the need for further stimulus, the Fed is not about to let down its guard if data turns out stronger than expected. The Bank’s focus remains on getting inflation above 2% and the labour market back to full employment, both of which remain a long way off.

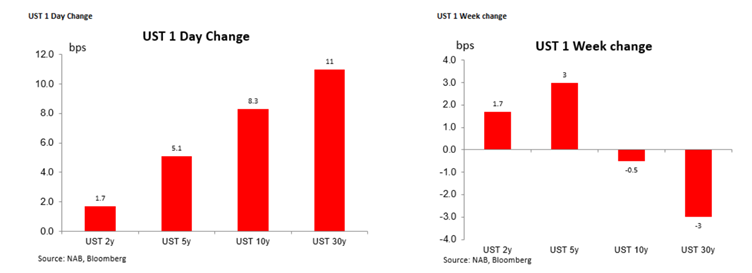

The UST curve endured an aggressive bear steaming following the solid labour market headlines. The late recovery in the equity market along with Fed Powell’s comment added further fuel to the move while there may have been some positioning taking place given the big issuance expected for this week.

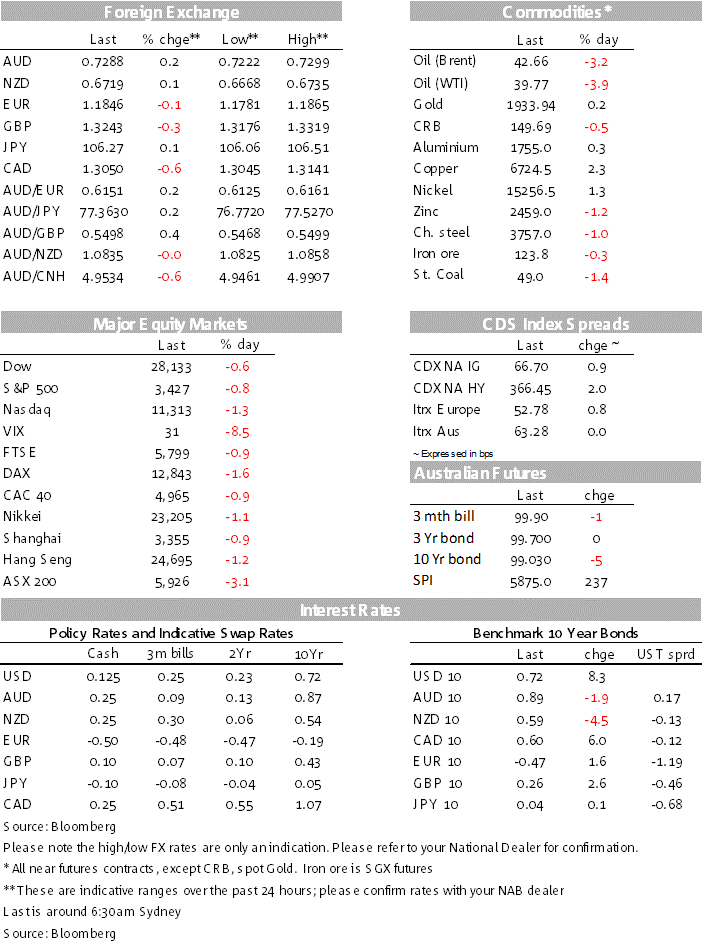

The US Treasury auction schedule includes $50bn 3-year notes (+$4bn vs previous), $35bn 10-year and $23b 30-year reopenings (+$6b and +$4b vs previous reopenings). Bloomberg noted IG corporate issuance is also expected to be large, including a wave of jumbo trades that may weigh on Treasuries via hedging flows. The 10y Note climbed 8.3bps on the day, ending the week at 0.7180% while the 30y Bond was 11bps higher, closing the week at 1.47%. Highlighting what was a volatile week, the 10y Note was little changed on the week while the 30y bond ended 3bps lower.

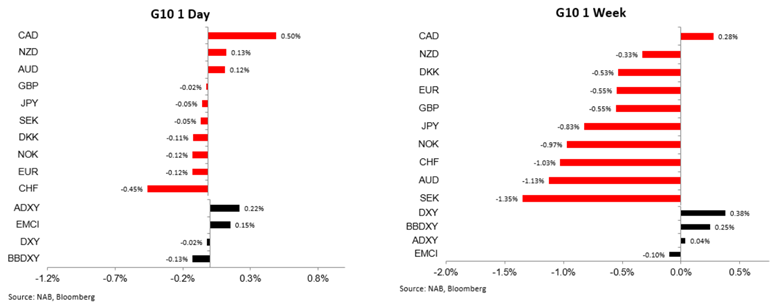

A look at the FX performance board depicts a deceiving picture with G10 pairs little changed on Friday. However the intraday charts depict a different picture with the USD making decent gains post the US payrolls report and then giving them back as the equity market recovered.

In index terms the USD ended Friday pretty much where it started, but it still had a good week, up 0.25% in BBDXY terms and 0.31% for the DXY.

Up 0.50% against the USD (USD/CAD at 1.3050) following a solid labour market report. Canada’s economy added 245.8k jobs in August, a fourth-straight month of gains that has recouped almost two thirds of employment losses from the pandemic.

The AUD traded to a low of 0.7222 after the US payrolls report and now starts the new week at 0.7288.

The NZD fell to 0.6670 after payrolls and now trades at 0.6720. Both antipodean currencies remain true to form losing ground on equity markets weakness and recovering as risk sentiment improves.

GBP has opened lower this morning following reports over the weekend highlighting the lack of progress in the UK-EU trade negotiations. UK’s chief Brexit negotiator has said the government is not “scared” of walking away from talks without a trade deal ready to come into force in 2021. David Frost told the Mail on Sunday the UK would leave the transition arrangement – which sees it follow many EU rules – “come what may” in December. EU negotiator Michel Barnier has said he is “worried and disappointed” about a lack of concessions from the UK.This morning the FT has also reported that the UK government is planning new legislation aimed at overriding key parts of the Brexit withdrawal agreement in a move that could threaten the progress of trade talks with the EU. Cable has fallen about 20pips this morning and now trades at 1.3265. The euro is little changed at 1.1847.

Notwithstanding the big moves in longer dated UST yields. The market may be pondering Japan’s current political uncertainty. The LDP will elect a new leader on September 14 to replace Prime Minister Abe, who abruptly resigned on August 28 due to health reasons. Japan’s next prime minister could call a snap general election shortly after taking office next week, a senior member of Japan’s ruling Liberal Democratic Party (LDP) said on Sunday, according to Kyodo news.

The market may be gearing up for a quiet start to the new week, but this expectations could be rattled with an increase in US-China tensions. The WSJ reported over the weekend that the Trump administration is considering whether to place export restrictions on China’s most advanced manufacturer of semiconductors, a move that could hurt China’s ambitions to become self-reliant on critical technologies and no doubt would intensify tensions between the two countries. A theme to watch at the start of the new week.

Victorian premier Andrews said Melbourne’s lockdown would be extended for another two weeks, from 14th September. From 28th September, restrictions would be eased in stages if new cases continued to decline.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.