We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Very soon it’s likely that the UK parliament will take the first step to delaying Brexit, allowing for yet more negotiating time with the EU.

https://soundcloud.com/user-291029717/us-manufacturing-shows-cracks-brexit-delays-and-aussie-gdp-today?in=user-291029717/sets/the-morning-call

The Peter Lee surveys are now taking place. If you have appreciated NAB’s Market Research support please let your company’s representative know

Falling down the mountain, End up kissing dirt, Look a little closer, Sometimes it wouldn’t hurt – INXS

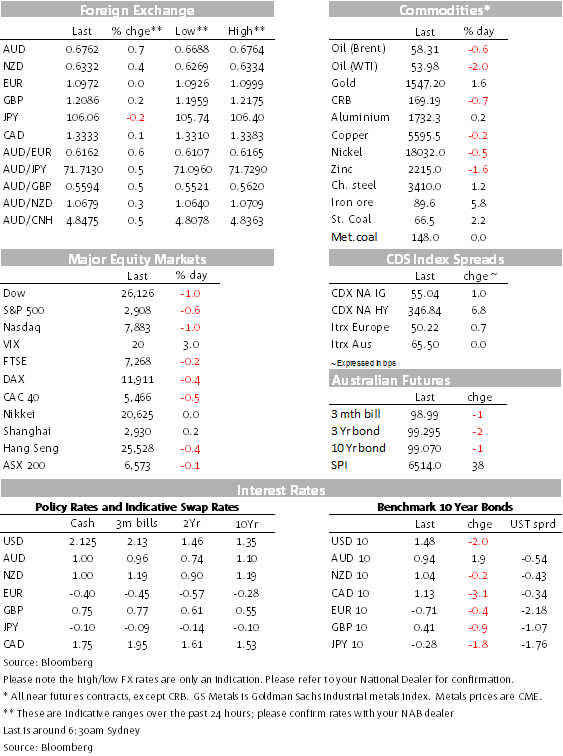

Against expectations for an unchanged outcome the US ISM manufacturing index contracted in August clipping the wings of a rising USD, also dragging equities and UST yields lower. Cable has remained volatile as the UK Parliament takes control of Agenda with a vote on bill to rule out hard Brexit expected tomorrow while PM Johnson threats to call a new election. Oil leads a broad decline in the commodities but iron ore bucks the trend joining gold as the outperformers. After briefly trading sub 0.67 yesterday, AUD is the G10 outperformer overnight with NZD also enjoying a small recovery.

Given trade tariffs news over the weekend, US equity futures were already signalling the potential for US equities to open lower on Tuesday, after a long weekend celebrating Labor day on Monday. Prior to the US open, President Trump also remained defiant on its trade policy stance suggesting that a trade deal with China would be much tougher if he wins the next Presidential election and the EU could also be in the firing line – criticising those who suggest he team up with the EU to fight against China with “EU & all treat us VERY unfairly on Trade also. Will change!” In other trade war related news,Huawei accused the US government of orchestrating a campaign to intimidate its employees and launching cyber-attacks to infiltrate its internal network.

So while the omens were already signalling the need to brace for a soft start to US equities trading, half an hour after the opening bell, stocks were hit by another blow with the August ISM manufacturing index revealing a contractionary reading for the first time since February 2016. The ISM index of manufacturing slipped to 49.1 from 51.2 and so below the boom-bust level, with apparent contraction in all the main sub-components such as new orders, production and employment. Economists had expected little change at 51.2. The slide below 50 means that US manufacturing is moving more in line with an evident global manufacturing recession, as depicted by the JPM Global Manufacturing PMI, which came in at 49.5 for August from 49.3, having fallen below 50 back in May.

How the Fed now responds to the news that a bellwether economic indicator has turned south will be key in whether markets start to price more aggressive easing and in turn whether the higher US dollar – which continues to be an additional headwind to US economies on the global stage – now stabilises or evens pulls back. We have a lot of Fed speakers tonight (see more below) with influential New York Fed Williams speaking at 23.25 AEST followed by a Q&A session.

The other consideration, of course, is whether the soft data forces President Trump to reconsider his negotiating position with China, our suspicion however is that the economy and US equity market has not weakened enough and for now, the President is more likely to increase the pressure on the Fed rather than seek a quick deal with China. Also worth noting that China is gearing up for its 70th anniversary of the founding the People’s Republic of China on October 1st , suggesting China is unlikely to have much appetite to seek any progress on trade in the near-term.

Reaction to the ISM data has seen the USD lose ground across the board, not helped either by the fall in UST yields which have been led by shorter dated tenors resulting in a steepening of the curve. The 2y rate is 4.4bps lower at 1.463% while the 10y now trades 1.473%, down 2.5bps. As an aside, is probably worth noting that while 10y Bunds closed little changed at -0.706%, Italian 10-year BTP yield fell 9bps to a record low at 0.86%, in anticipation (and confirmation after the close) that Supporters of Italy’s 5-Star movement would back plan for a coalition government with rival democrats in an online vote.

Prior to the US equity open, USD indices were moving higher with the DXY index trading to an overnight high of 99.369, post the ISM the USD endured weakness across the board and now DXY trades at 98.52. AUD has been the outperformer, up 0.66% to 0.6760, after trading down to a low of 0.6688. NZD has also endured a nice recovery up 0.46% to 0.6337. Both antipodean currencies remain at the mercy of global growth and trade uncertainties. The AUD recovery can also be attributed to yesterday’s RBA decision to stand pat without giving a strong signal that another rate cut is imminent, notwithstanding the strong likelihood that Q2 GDP will disappoint today (see more below) while soft July retails sales suggest the consumer has remained subdued in Q3. The 5.8% jump in iron ore probably also helped the AUD.

GBP has been the other mover, after trading below the 1.20 mark late in our session, cable now trades at 1.2082. Early in the overnight session Boris Johnson lost his slim majority in Parliament with the defection of one of his Conservative MPs Phillip Lee, who crossed the floor to sit with the Liberal Democrats and few minutes ago the UK Parliament voted 328 to 301 to take control of the agenda, meaning the Commons can now bring forward a bill seeking to delay the UK’s exit date. The vote on the bill is expected to take place tomorrow and PM Johnson said that if the bill passes he will bring forward a motion for an early general election.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.