Total spending grew 0.9% in June.

You might have expected a positive market response as the US politicians reach agreement on a fiscal stimulus bill, particularly as Europe became the latest region to approve a vaccine.

https://soundcloud.com/user-291029717/us-pays-out-whilst-uk-digs-in?in=user-291029717/sets/the-morning-call

Old England is dying, Still he sings an empire song, Still he keeps his navy strong, And he sticks his flag where it all belongs, Old England is dying – The

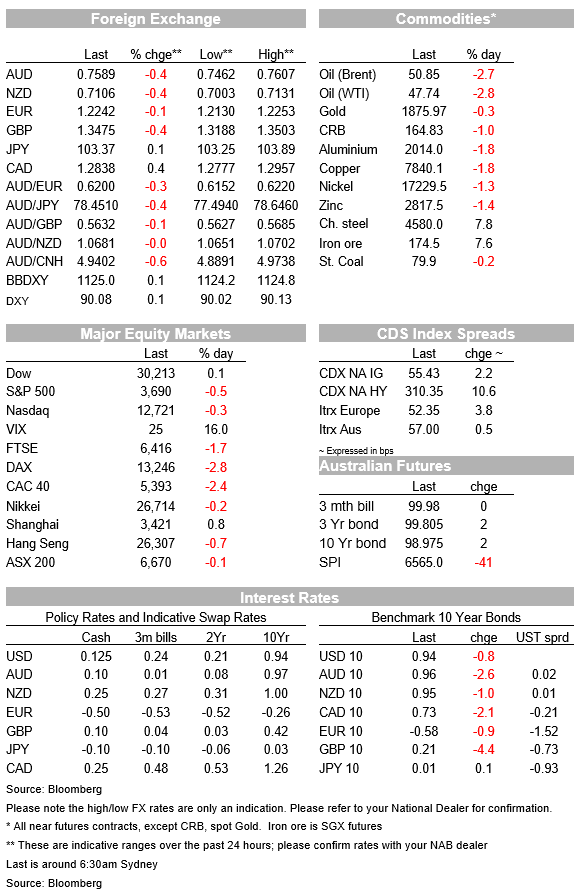

Apologies for the sombre title to round out our 2020 song choices, but unfortunately apt given latest UK developments, not so much the continued absence of a UK-UK post-Brexit trade deal as the reportedly ‘out of control’ new COVID strain in the UK and resulting severe lockdowns that impact more than 16 million people in the south of England and have all but ruined Christmas for many of them. Besides, It’s one of the best songs from one of my favourite bands – I’d been singing it to myself on numerous occasions for the 20 years since it was first recorded in 1985 and prior to escaping the Old Dart in 2005. The vinyl copy still gets the odd airing in Sydney 15 years on. Certainly UK development have overshadowed the positive news of agreement to a ~$900bn US fiscal support bill to see a sizeable sell-off in risk assets, lower commodity prices (oil especially), support for the USD and weaker currencies across the board, including time spent back below 0.75 on AUD/USD – albeit we have seen a pretty significant intra-day turnaround across most markets in the last few hours,

To currencies first for a change and while the AUD got off on the wrong foot at the Wellington market open yesterday, it was notable as we went through the day that the NZD was faring equally badly; indeed the AUD/NZD cross has spent a little time above 1.07 overnight, its best since 9th November. So while the weekend new of covid outbreaks Sydney’s northern beaches was very unwelcome news, its market impact has so far been minimal. Bear in mind in this respect that the northern beaches population of some 280,000 represents little more than 1% of the Australian population, compare to over 5 million or 20% of the population in Melbourne. That said, it’s possible to argue that the news was also negative for the NZD in so far last week’s optimism towards a trans-Tasman travel bubble being established early in the new year and which would be something of a boon to the New Zealand tourism industry, have evidently suffered a significant setback (even if, as our BNZ colleagues like to remind us, Aussie tourists are particularly tight-fisted compared to other international tourists whenever they visit bro’Town.

In truth, the origins of the bulk of the weakness in both currencies yesterday probably lay outside both of Australia and New Zealand’s borders, the grim news regarding COVID infections in the UK – and elsewhere it has to be said, including the US, has forced markets to question prior optimism that with vaccines starting to be rolled out, they can readily look through the near term economic damage being wreaked by latest social distancing strictures and which of course may now last longer than previously discounted.

Elsewhere in currencies GBP has been Monday’s biggest lower, GBP/USD spending time below $1.32 having been above $1.36 as early as last Thursday. Virus news aside, the passing of another weekend without news of a post-Brexit EU-UK trade deal has had a depressing impact and where the (public) rhetoric from UK PM Johnson continues to suggest the government in nonplussed as to whether there is or isn’t a deal by 31st December, Johnson lamenting differences over law enforcement mechanisms as well as fishing rights in his latest utterances. We (and for the most part markets) continue not to take Johnson at his word here, and indeed GBP/USD has just revisited $1.35 as we type, albeit this looks to be part of a broader resumption of USD selling and where the Bloomberg BBDXY index is now almost back to flat on the day.

Equity markets are also enjoying a turnaround, with loss for the S&P500 pared to just 0.3% having been down over 2% early in the New York session. Washington is currently in process of approving a $900bn fiscal relief package which includes $600 payments to most people (excludes high income earners), $300 per week aid for the unemployed who don’t ordinarily qualify for benefits, rental assistance for tenants in arrears and a whole host of other spending initiatives. The package id due to be voted on today by the House, Senate and signed into law by the President if all goes to plan. Being largely discounted at the end of last week, follow-through support for risk asset Monday has been notable by its absence, though it will doubtless be getting some of the credit for the progressive recovery in US stocks off their opening losses. Earlier Monday, the Eurostoxx 50 ended with a loss of 2.7% with similar sized losses for both the German Dax and France’s CAC40 while the UK FTSE suffered a smaller 1.7% loss, probably because of the currency fall.

Bond market have seen yield lower cross the board, US 10-yr Treasuries down to 0.88% at one point from close to 0.85% on Friday, but along with the broader market rebound are now almost back to unchanged on the day. UK gilts finished their day 4.5bp lower t 0.25 and German Bunds down 0.7bp at -0.58%.

Finally commodities saw oil take a sizable hit (4% or close to $2) in conjunction with a whole host of fights from the UK to Europe and elsewhere being cancelled, though have recovered about 70 cents of these losses since. Base metals were also lower (copper and aluminium both by around 1.7% in LME trade).

Preliminary Australian retail sales figures for November (11:30 AEDT) are expected to show 2% rise according to the median economist estimate, fuelled in part by the fuller re-opening of the Victorian economy, but note that forecasts range from 0.9% to 7.0% (NAB 5.5%) so the chances of a significant surprise relative to the medium are obviously high.

Plenty of data points elsewhere in the world but not of it top tier. The US has the Conference Board December Consumer Confidence readings (expected 97.0 from 96.1) November Existing Home Sales seen -2.2% after +4.3% in October, the Richmond Fed December Manufacturing Index (expected at 12 from 15) and the third reading of Q3 GDP (seen unchanged at 33.1% saar).

Europe has German consumer confidence(of some note given the recent spike in infection rates and renewed distancing restrictions) while the UK has its final estimate of Q GDP (last at 15.5%) and November data for public finances, expected to show a monthly budget deficit of GBP26.8bn.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.