NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

America has been off work for Presidents Day, but that hasn’t stopped markets optimistically looking to a world where COVID-19 isn’t centre stage.

Temperatures in Houston fell to as low as -11C on Monday, with an inability to keep up with energy demand prompting rolling blackouts, production in parts of the shale oil basin in Texas curtailed and now the biggest US oil refinery, in Port Arthur (Texas not Tassie) shut down.

News of the Arctic snap saw crude oil futures up +/ – 2% during our time zone yesterday, WTI rising above $60 for the first time since January 2020 and Brent pushing above $63.

WTI was trading around $52 and Brent $56, gains since then and prior to yesterday supported by anticipation of stronger demand as and when economies more fully re-open, declining oil inventories and confidence that OPEC+ will extend current production curbs.

It’s not just oil that is doing very well in the commodity complex, with ‘Dr. Copper’ rising to a new post-September 2012 high of $8,394 a tonne. BHP (and its advertising agency) must be feeling pretty smug at the moment given its rolling TV commercials extolling the necessity of copper in all manner of green energy initiatives, including electric vehicles and solar power.

NOK and CAD are currently topping the G10 FX scorecard, up 0.8% and 0.5% respectively since the weekend but with AUD not too far behind, up 0.3% to a high of 0.7789.

GBP is the other strong performer, benefiting throughout Monday’s session and rising to above $1.39 against the USD, following weekend news that the UK vaccine roll-out was well ahead of every other developed economy bar Israel. 23% of the UK population have now had their first jab compared to just 5% in Italy and Germany, and 16% in the United States.

U.K. Prime Minister Boris Johnson is drawing up plans for gradually lifting pandemic restrictions on socializing, shopping and traveling to work, and next Monday aims to set out target dates for when the curbs will be eased, saying “We want this lockdown to be the last…we want progress to be cautious but irreversible.” The first priority will be to try and re-open schools as early as March 8, he says.

The USD is no longer deriving any benefit from still-rising US bond yields and increased confidence that something close to President Biden’s $1.9tn covid relief fiscal ambitions will see light of day via the Congressional budget reconciliation process, meaning passage requires only a simple majority in the Senate.

Both the narrow DXY and broader BBDXY indices fell by 0.2% yesterday, even as 10-year US Treasury yields rise above 1.20% in New York on Friday and futures markets in Asia yesterday took the implied yield up to nearer 1.25%. Our observations here are that: 1) Markets have reason to fret about the implications of another massive dose of fiscal support for the United States’ ‘twin deficits’ and where blow-outs have historically produced a weaker USD, and 2) Rising nominal bond yields are being by and large matched by rising inflation expectations (both market implied, from Treasury Inflation Protected Securities (TIPS) and consumer surveys (e.g. last Friday’s University of Michigan one-year ahead inflation expectations reading at 3.3% was last higher than this back in 2012).

Thus the USD is not getting any love from higher bond yields in real terms.

Was USD/JPY given its strong relationship to the 10-year yield spread over the equivalent JGB, USD/JPY up 0.4% to Y105.35. A stronger Nikkei, following better than expected Q1 GDP (see below), ironically also helped weaken the JPY, albeit causality usually runs from a weaker JPY to the stock market via the boost this gives to Japanese exporter earnings.

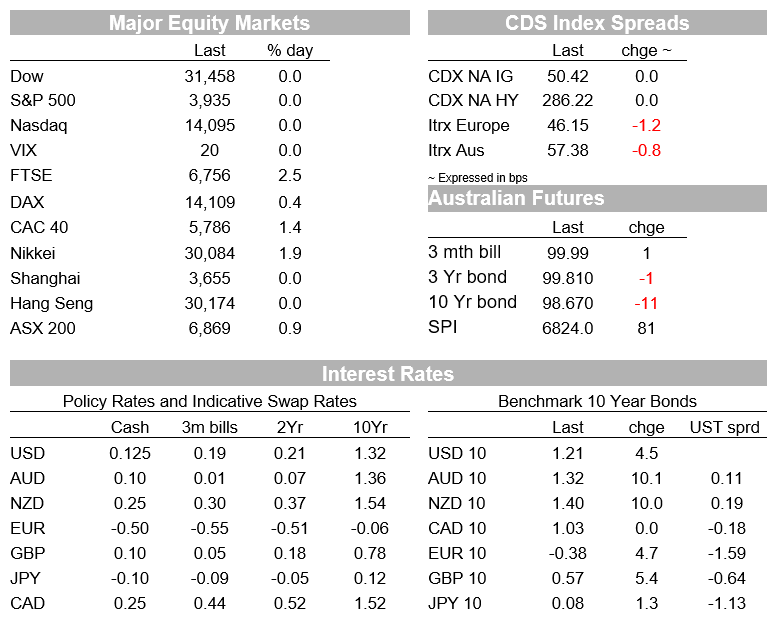

US equity markets were closed for the Presidents day holiday Monday but futures were trading and where the S&P 500 contract added another 0.5% (implying new record highs for the cash index) while the Eurostoxx 50 put on one percent and the UK FTSE 2.5%.

Yesterday, with China, Hong Kong and Taiwan closed, the Nikkei was the start performer, keying off the better than expected Q4 Japan GDP data (+3.0% Q/Q against 2.4% expected) and meaning that over 2020, Japan has fared better than any other major country in terms of having the smallest GDP hit.

Unfortunately Q1 is likely to be negative given the early year lockdowns following renewed virus outbreaks in Tokyo.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.