We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

US stocks are on the rise as optimism for a trade deal intensifies.

https://soundcloud.com/user-291029717/us-stocks-flying-high-on-hope?in=user-291029717/sets/the-morning-call

We’re gonna be a sailin’ on the funky, funky sound (till I reach the highest ground)

Bustin’ out and I’ll break you out, ’cause I’m sailin’ on (Till I reach the highest ground) – Red Hot Chilli Peppers

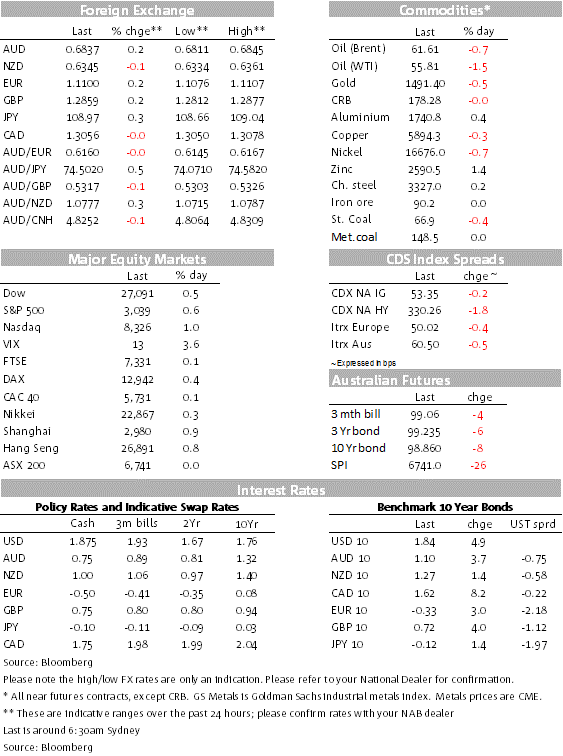

The stage was already set for a good start following US-China positive vibes over the weekend, but not to be outdone President Trump overnight gave the feel good vibes an extra lift after he suggested US-China negotiations were ahead of schedule. The equity board is a sea of green with the S&P 500 index trading at a new record high while UST have led the move higher in core global bond yields, as investors unwind some of their safe haven positions. The USD is little changed in index terms, softer against EM FX and pro-growth currencies such as the AUD ( NZD an exception) and stronger against safe haven currencies such as JPY.

Speaking overnight before leaving to Chicago, President Trump said he expected to sign the so called Phase One part of the trade deal with China ahead of schedule but did not elaborate on the timing. The President said that the Phase One signing was planned for the November 16-17 APEC summit in Chile, but also noted the political unrest in the country adding that he believed something could be worked out. Unclear whether his comment means a signature could happen sooner.

So far the soundings coming from both the US and China point to the likelihood a significant progress in trade negotiations. The two sides have seemingly reached consensus in areas including standards used by agricultural regulators, but is probably worth noting that so far neither party has officially said anything about the contentious issue surrounding China’s demand for a pullback on US Tariffs. The market appears to be interpreting the improvement in trade talks as a positive sign that the US will suspend its planned tariffs on ~$160b of Chinese imports due to take place in December and potentially even pull back some of the tariffs impose in September. This is a big assumption as talks could easily fail again if both parties don’t find a compromise.

Regardless of this small, but very important detail, global equity markets have begun the new week with a spring in their step. Notably, the S&P500 looks set to close above 0.5% and at a new all-time high. The NASDAQ is up around 1% and sits a fraction below its all-time high, while the price-weighted Dow Jones has lagged a little, although it too remains within vicinity of its all-time high. Earlier, European indices were mostly up between 0.1% to 0.4% and the Eurostoxx 600 index was approaching its highest level since mid-2015 while the Nikkei had yesterday reached a more than one-year high. Despite a long list of potential negative risks lurking, the VIX index of implied volatility on the S&P500 has drifted down to below 13, a low level on a historic basis.

Bond yields have risen in tandem with equity markets as growing hopes of a US-China trade truce have led markets to pare back central bank easing expectations and investors have rotated out of safe-havens (amidst reduced downside risks to global growth). The UST curve has bear steepened with the 2y rate up 2.4% to 1.645% while the 10y note is up 5.2% to 1.842%. The move up in bond yields has occurred despite continued expectations that Fed will cut rates by another 25bps this week to 1.75% (the market prices a roughly 90% probability of a 25bp cut). However, future rate cut expectations have been pared back with futures markets now implying only around one further 25bp rate cut by the Fed by the end of 2020. Market pricing suggests the balance of risks around future Fed policy is still towards easing, but less so than previously and investors will look to the FOMC statement this week for further guidance.

The improvement in risk sentiment sees the USD unchanged in index terms against other majors but softer against EM FX. TRY +0.75% and ZAR 0.68% have led the charge in EM FX while the USD is also weaker against pro-growth G10 pairs such as the AUD (+0.25%) and CAD (+0.08%), but somewhat surprising the NZD ( -0.05%) has been unable to join the party. The AUD/NZD may be playing a part here as the AUD is more exposed to China’s economic fortunes and the cross has again found good buying interest just below the 1.07 mark (the cross now trades at 1.0778).

GBP is the G10 outperformer, +0.26% and now trading at 1.2857. Overnight the EU approved a “flextension” that could last as long as the end of January, but the UK can also leave the bloc beforehand if it is able to ratify the Withdrawal agreement. PM Johnson, albeit reluctantly, formally accepted the extension offer and then moved to call an election on December 12th. As expected the UK Parliamentary rejected the PM’s call for an election and now Bojo will aim publish a bill that would only need a simple majority to pass – not two thirds as required in today’s failed attempt, a new vote is expected to take place tomorrrow. The Liberal Democrats and the SNP have suggested they might be prepared to support the new bill as long as the election is set for the 9th and not the 12th of December. A December 9th election in theory prevent the PM from attempting to pass his Withdrawal Agreement Bill before Parliament is dissolved.

As we’re about to press the send button US House Speaker Nancy Pelosi has confirmed that the House will vote this week on resolution formalizing impeachment inquiry. The vote is expected to take place on Thursday.

Alphabet reported operating income for the third quarter that was 2.9% below the average analyst estimate. Share fell 2.1%inpost market trading.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.