Long-term signal vs. Short-term noise

Insight

The US President has been on Twitter in the last few hours threatening to lift tariffs on China by the end of the week

https://soundcloud.com/user-291029717/trumps-week-end-tariff-spat

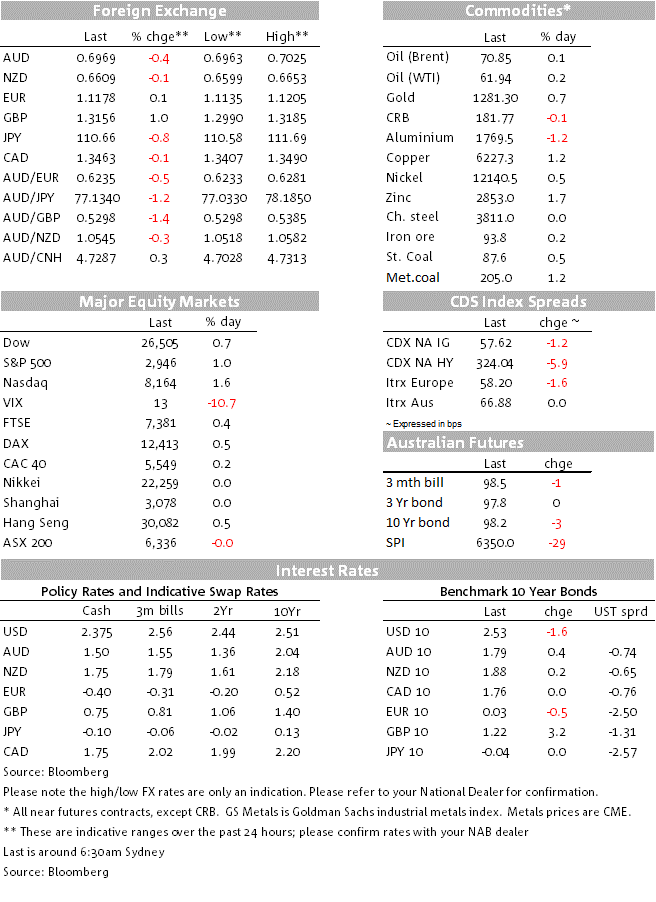

A few hours ago President Trump set the tone for the new week expressing dissatisfaction at the pace of China trade negotiations amid Beijing’s attempt to renegotiate. The President has threatened to lift trade tariffs from 10% to 25% as talks are due to reach their final stage this week. An increase in tariffs would be bad news for risk assets and would threatened the prospect of a global growth recovery. AUD and NZD are 20 pips lower at the open as we await for Asian markets to open and China’s response.

Friday night’s price action was all about the US labour market report which revealed a very solid set of new job, but the lack wages pressures carried the day with US equities loving the goldilocks scenario of a Fed going nowhere in a hurry while the USD and UST yields drifted lower. GBP was the outperformer after poor local election performance by Conservatives and Labour was interpreted as yet more pressure on politician to get a Brexit deal over the line.

The pace of US job creation picked up again in April with 263k non-farm payroll jobs created, significantly more than the 190k market consensus, but more or less in line with Nab’s 260k – a number we suspected could be influenced by weather and possible Census hiring. The April jobs report was further strengthened by a 2/10 drop in the unemployment rate to a 49-year low of 3.6% – below the 3.8% unchanged consensus (Nab 3.7%). However wage inflation of +0.2% m/m for 3.2% y/y was a tenth below forecast. So the key take way then is that the US jobs market remains in rude health, but the lack of material wages pressures is likely to keep the Fed comfortably at bay.

Equities loved the US labour market report with not only US but European indices closing in positive territory. The Stoxx Europe 600 gained 0.4%, the most in a month, the US NASDAQ led the charge in the US closing 1.58% higher and at a new record high. The S&P500 closed almost 1% stronger and the Dow was not too far behind, climbing 0.75% on the day.

Friday night also included a fair bit of Fed speakers and while the general message was broadly consistent with Powell’s patience missive, Chicago’s Fed President Evans sounded a bit more cautious noting that the risk that underlying inflation may be stuck below the central bank’s 2 percent target raises strategic concerns. Evans said he is “uneasy” about the outlook for inflation after recent declines in core price measures adding that “We don’t want to be too dismissive of this development.”. The USD and UST yields took note of Evans’ comments, but then those move reversed following more upbeat comments from Vice Chari Clarida. The Vie Chair remarked that he regards inflation as “muted” and inflation expectations as “stable” and described the US economy as being in “a very good place,” thus affording policymakers time to assess incoming data before deciding on any additional changes to federal funds rate.

The solid US jobs prints in April resulted in further unwind of Fed rate cut expectations following Fed Chair Powell patient comments and huis view of transitory downward pressure. The probability for a Fed rate cut in December is now just under 50% having been around 68% erarly l;ast week before the FOMC meeting.

Ahead of the non-farm payrolls report, the ISM Non-Manufacturing figures for April revealed a retreat to 55.5 against expectations for a small rise to 57 from 56.1. Although the April number suggests the US service sector remains in expansion territory, this was the lowest print since August 2017 with all major sub-indices pulling back from their March reading.

The USD was weak across the board after the employment report, with the key USD indices down 0.3-0.4%. GBP was the top performer, up over 1% to 1.3170. The Conservatives and Labour party both did poorly in local elections, taking their shared vote to 56% (down from 82% in the 2017 general election). PM May and Labour leader Corbyn both agreed that the message from the election was to sort out Brexit. The market took the view that the poor election for both parties gives added incentive to come to an agreement on Brexit when talks resume this week.

According to the Sunday Times, PM May will outline plans for a comprehensive but temporary customs arrangement with the EU that would last until the next general election. The PM is seemingly willing to compromise on three areas: customs, goods alignment and workers’ rights, but it remains to be seen whether this proposal will be enough to get Labour on side. Meanwhile newspaper commentaries by Brexitiers over the weekend suggest this proposal is set to create further divisions within the Conservative party. If an agreement is reached, this would pave the way for further GBP gains, although the risk of further political tension and prospect of a general election are also likely to rise.

Both the AUD and NZD had a good Friday although the two antipodean currencies were the G10 underperformers for the week. Trump tweets overnight has seen the AUD gap lower from 0.7024 to 0.6975 currently and the NZD from 0.6645 to 0.6610. Focus now turns to Asian markets reaction and any response from China, but if recent history is any guide, we suspect we are unlikely to see a swift response from China today. That said as noted by our BNZ colleague Jason Wong, an aggressive response from China (threat of retaliation?) that halts current negotiations, with higher tariffs by the end of the week would be a disaster for risk assets. Even without the US-China war overhanging the market, it was always going to be a pivotal week for the NZ and Australian rates market and the AUD and NZD, with the RBA’s meeting on Tuesday followed a day later by the RBNZ.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Long-term signal vs. Short-term noise

Insight

Welcome to NAB’s newsletter on the Sustainable Finance market from an Australasian perspective.

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.