Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

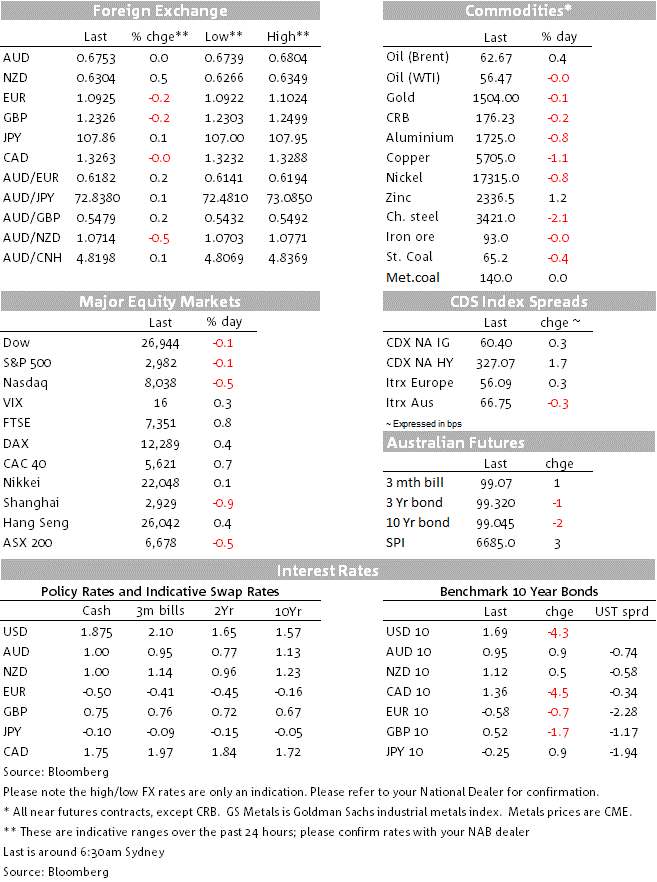

The US dollar index (DXY) reached over 99.3, close to a two-year high.

https://soundcloud.com/user-291029717/the-us-dollar-close-to-two-year-high-despite-everything?in=user-291029717/sets/the-morning-call

Tell me, baby, what’s your story, Where you come from And where you wanna go this time? – Red Hot Chilli Peppers

European equities enjoyed a decent day with all major regional indices recording gains, but the release of a whistle-blower complaint on the Trump Ukraine saga weighed on US equities at the open with news that the US is unlikely to extend waivers for US firms to supply Huawei not helping sentiment either. On Tuesday, news of Trump’s impeachment enquiry weighed on the USD, but 48 hours later the political uncertainty alongside unfriendly trade headlines are benefiting the USD. Meanwhile, US data also continues to support the narrative that the US economy is still the least dirty shirt in the laundry basket. The UST curve has bull flatten and in G10, NZD is the outperformer, retaining its gains post RBNZ ‘s Orr comments yesterday.

US political drama is a gift that keeps on giving this week, so much so that the Brexit drama has been kicked into the back pages. After the release of the Ukraine call that technically did not reveal a smoking gun, overnight a whistle-blower’s complaint (an unidentified US intelligence official) has been made public claiming White House officials “were deeply disturbed” by the call and attempted to “lock down”. The whistle-blower alleges that White House officials said internal lawyers debated how to handle the details of the call, due to the “likelihood… that they had witnessed the president abuse his office for political means”. The whistle-blower recounted being told that White House officials restricted access to details of the presidential call by storing the information in a specially classified storage system.

So while the Ukraine call has not revealed any explicit wrong doing from a legal perspective (a debate is ongoing whether between the lines there was some coercion intended to gain some domestic political advantage), the whistle-blower now throws another angle into the whole drama. May be there has been no wrong doing, but the attempt to concealed what happened could be a problem. Trump and his supporters are questioning the credibility of the whistle-blower’s account, but House Speaker Pelosi has been quick to call the Trump administration’s actions a “cover-up” (remember Watergate and Nixon?).

If that wasn’t enough to put a dampener on markets, soon after the US open, hopes for better US-China trade relations remained low after a US government official said that the US is unlikely to extend a waiver allowing American firms to supply Huawei. Furthermore, the government isn’t ruling out additional punishments for allies that refuse to ban Huawei equipment in 5G networks, in addition to potentially cutting them off from intelligence-sharing agreements.

European equities indices closed higher across the board after trading in the green from the onset. The Stoxx Europe 600 Index climbed 0.6% with most sectors ending the day in the green. The whistle-blower story weighed on US equities from the open, US data (more below) instigated a small recovery half way through, but in the end trade and political uncertainty was too much with the S&P 500 closing 0.24% lower and the NASDAQ was -0.58%.

US data releases overnight didn’t really have a lasting effect on markets, but in the whole they have done nothing to dissuade the view that the US economy is still doing better than other majors. The August advance trade deficit in goods rose marginally to $72.8bn from $72.5bn, but the number was better than the $73.4bn expected by consensus. Q2 GDP growth was unrevised at 2.0%, as expected, but the core PCE deflator was unexpectedly revised up to 1.9% from 1.7%.

As noted in the opening paragraph, on Tuesday, news of Trump’s impeachment enquiry weighed on the USD, but 48 hours later the political uncertainty alongside unfriendly trade headlines are benefiting the big dollar. It seems that when push comes to shove, the USD remains the safest place to be at the moment. In addition to its prime reserve currency status, the greenback is still benefiting from a yield supremacy and a US economy that is still performing relatively well. The DXY index traded to an overnight high of 99.276, nine pips below its year to date high and essentially only a few pips away from two year highs. USD gains were broad based with NZD (+0.48%) the only G10 outperformer and TRY (0.07%) the winner within EM FX.

The gains in the kiwi largely reflect yesterday’s pop on the back of upbeat RBNZ Governor Orr’s comment. Orr said that he was pleased with the outcome of August rate cut. Whereas in August he was keen to play up the possibility of negative rates and unconventional monetary policy, he gave a more circumspect perspective, saying “we are currently thinking hard about these questions…as a precaution. Our current view is that we are unlikely to need ‘unconventional’ monetary policy tools. “. NZD traded to an overnight high of 0.6326 and now sit just under the figure at 0.6298.

Jason Wong, our BNZ Market strategist notes that the NZD bounce should be seen in that context of the extreme NZD short positioning (based on CFTC data) that we have been highlighting since Monday. The “news” content of both the OCR Review and Orr’s speech was both fairly minimal, but heavy short positioning is apt to create some additional volatility. The course of the NZD over the rest of the year is more likely to be determined by developments in the US-China trade war than any NZ monetary policy tweaks.

Meanwhile the AUD is unchanged on the day, currently trading at 0.6749, after reaching an overnight high of 0.6781. Technically after trading to a high of 0.6895 on September 13th, the AUD has been in a downtrend and remains vulnerable to the downside. Yesterday, the ABS measure of job vacancies, which is the measure preferred by the Reserve Bank, fell again in Q3, down another 2% to be 2% lower than a year ago. Our economists note that the decline in this measure of job vacancies is not surprising given other measures of job ads are falling while NAB’s summary measure of the demand for labour continues to point to unemployment edging higher, as well as a lower cash rate. The market is now pricing a 77% chance of an October RBA rate cut, after briefly recording a probability of 60% following (what we judge to be) a misinterpretation of Governor Lowe’s speech on Tuesday night.

Of the majors, GBP and EUR are on the softer side of the ledger, with the latter making a fresh multi-year low of 1.0922. Speaking in New York, ECB Chief Economist Lane said there’s still room to cut interest rates further and described a stimulus package that split policy makers as “not such a big package.”, his comments played into the euro softness overnight. Meanwhile Brexit circus continues with little progress made as to its likely resolution. GBP threatened to break below 1.23 overnight, before recovering and now trades at 1.2327.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

Conditions ease as slow growth weighs on firms

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.