NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

A wave of positivity seems to have hit the markets.

https://soundcloud.com/user-291029717/us-dollar-equities-and-bond-yields-rise-but-why?in=user-291029717/sets/the-morning-call

My loneliness is killing me (and I), I must confess I still believe (still believe) – Britney Spears

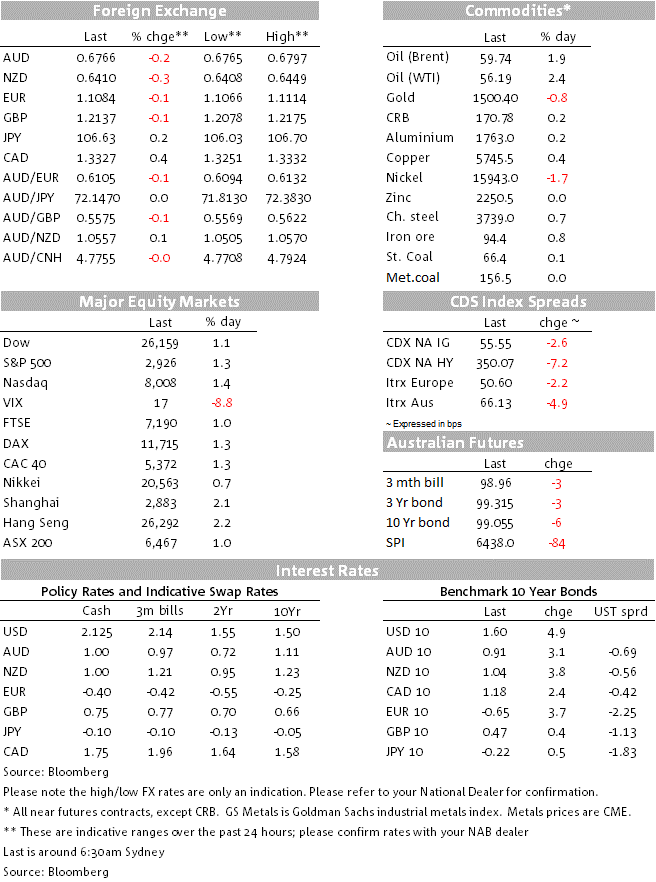

US and European equities had a solid night boosted by confirmation the US commerce department will delay its ban on Huawei for another 90 days. Equity markets were also boosted by further speculation that the German government is preparing to ease fiscal policy with the news also fuelling a rise in core global bond yields. The improvement in risk appetite however has not benefited risk sensitive currencies such as the AUD and NZD with both antipodean pairs losing ground against a broadly stronger USD. The latter is likely to instigate a new round of tweets from President Trump who overnight complained about the strong USD and also urged the Fed, again, to cut by a 100bps.

The S&P 500 has ended the day 1.21% higher, a third consecutive day in positive territory. The cumulatively gain over the past three days have effectively erased the 2.93% declined recorded last week Wednesday, triggered by poor China July activity data and a negative Q2 German GDP print. Gains in the S&P 500 were led by IT companies with the NASDAQ also having a good day closing 1.35% higher. European shares also had a solid night with the Stoxx 600 index ending the session 1.1% higher.

Once you get past the headlines and look at the details it is hard to get too excited about the rebound in equities. For one the temporarily delay on the Huawei ban was expected and according to US Commerce Secretary Wilbur Ross the reason for the extension was to allow US companies “a little more time to wean themselves off” their dependency on Huawei. The equity market has treated the news as a positive sign of progress in the trade negotiations (still believe like Britney!), but in addition to Wilbur Ross comments, in its announcement the Commerce Department also added another 46 Huawei affiliates to its trade blacklist. Thus details don’t necessarily suggest the US is making too many concessions on the China trade negotiations.

The other positive news has been more headlines around the possibility the German government may be looking at opening its purse in order to stimulate its ailing economy. Overnight, Bloomberg reported that the government is preparing fiscal stimulus measures that could be triggered by a deep recession, designed to bolster the domestic economy and consumer spending. But consistent with Chancellor Angela Merkel comment last week that the economy is “heading into a difficult phase” and that her government will react “depending on the situation.” It’s worth emphasising the conditionality of any German fiscal stimulus, the economy needs to be in a recession first before the government triggers a fiscal stimulus. So an imminent fiscal spending plans is not in the offing, politically the appetite to spend money is not quite there, Germany’s labour market is still in rude health while main political parties are still very supportive of the Schwarze Null (black zero) or balanced budget policy that has been in place for nearly a decade. Finally, worth noting too that government requires the lower house of parliament to declare a crisis in order to issue debt beyond the normal guidelines.

On that note, overnight the Bundesbank said in its monthly report that German output will remain “lackluster” in the third quarter and “could continue to fall slightly”. That would be a second straight quarter of contraction — the typical definition of a recession — after a 0.1% decline in the April-June period.

The Huawei news and speculation around German fiscal stimulus also boosted core global yields overnight. 10y Bunds closed up another 5bps, to minus 0.65%. The US 10-year rate rose to as high as 1.62%, and currently trades up 5bps at 1.60%. The Fed’s Rosengren ( a known hawk), who dissented against a rate cut at the last FOMC meeting, said that he wanted to see “evidence that we’re actually going into something that’s more of a slowdown” to justify any easing monetary policy.

Meanwhile in currencies, the big news has been the strength in the USD with the BBDXY index recording a new year to date high (1212.77) closing the session 0.274% higher while the DXY index closed at 98.35 (+0.21%). Pro- growth risk sensitive currencies such as the AUD and NZD have not benefited from the feel good vibes in equity markets, perhaps reflecting the high degree of uncertainty that still lingers in the air. The AUD now trades at 0.6766, down -0.19% on the day and technically it remains in a downtrend, although its decline has lost some momentum over the past couple of days.

The NZD has traded mostly within a tight 0.6410-0.6430 range and currently sits near the bottom of that. The only data release of note was the NZ Performance of Services Index, which pushed higher to a slightly above-average level. This was a relief coming hot on the heels of the manufacturing PMI falling below the important 50 mark.

EUR and GBP are little changed, while USD/JPY is up 0.2% to ¥106.60, a pretty insignificant move in the context of higher global rates and equity markets. Lastly CAD has been the weakest, even against a backdrop of a 2% gain in oil prices, with USD/CAD up 0.4% to 1.3325.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.