Coming in for landing in a heavy cross wind

Insight

Markets turned sharply to a risk-off mood at the end of last week, on the realisation that vaccine roll outs will take longer than hoped whilst infections are growing.

https://soundcloud.com/user-291029717/vaccine-delays-throw-dampener-on-recovery-timelines?in=user-291029717/sets/the-morning-call

There was one negative covid-19 news story after another on Friday and which equity investors ultimately couldn’t ignore. These ranged from the announced lockdown of parts of Kowloon (for the first time during the pandemic) as well as Malaysian holiday resorts; record high daily new case numbers in some countries, Mexico for one; reports that the new UK covid variant was not only more infection but, PM Johnson said, perhaps a third more deadly that the original strain; and in the EU, widespread dismay being expressed by political leaders that Astra Zeneca (and also Pfizer) were not going to be able to deliver vaccine doses in coming weeks anywhere close to the numbers they had contracted to supply with various governments.

Just now, John Hopkins University has just reported that US case numbers have exceeded 25 million, while UK Health Secretary Matt Hancock has been out saying that the vaccines currently being rolled out may not be as effective against the newer, more virulent strains of the virus and that UK quarantine rules may have to change to be hotel not home based (er, hello?).

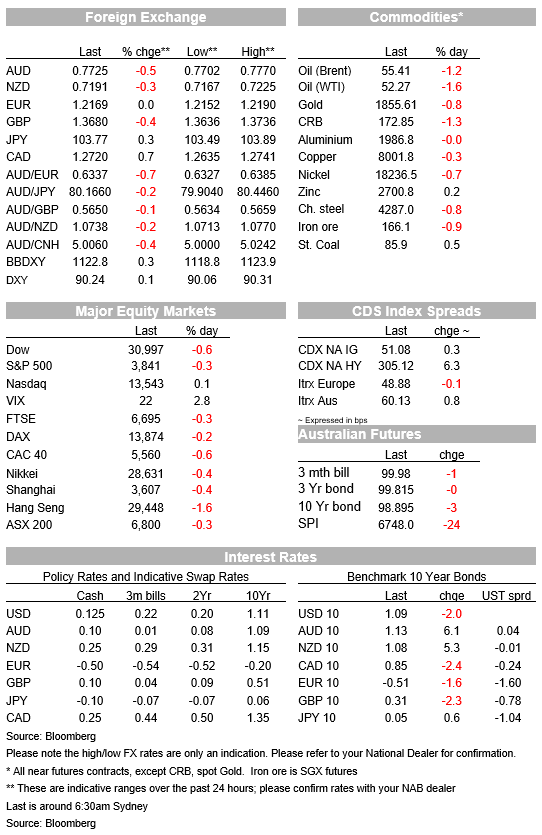

The highlights of which were the various ‘flash’ PMIs in Europe and the US, were quite mixed, but where the starkest contrast was between a much sharper fall than expected in the UK service sector from the latest lockdowns (38.8 from 49.4) but stronger than expected US numbers for both manufacturing and services and which were both up by at least two points on December. The pan-EZ numbers showed much smaller rises for both manufacturing and services, albeit both a tad better than expected. See below for a full summary below. The most noticeable market impact of all this was significant underperformance by the UK stock market relative to elsewhere (e.g. FTSE -1.5%) while Sterling suffered alongside the more cyclical/commodity currencies.

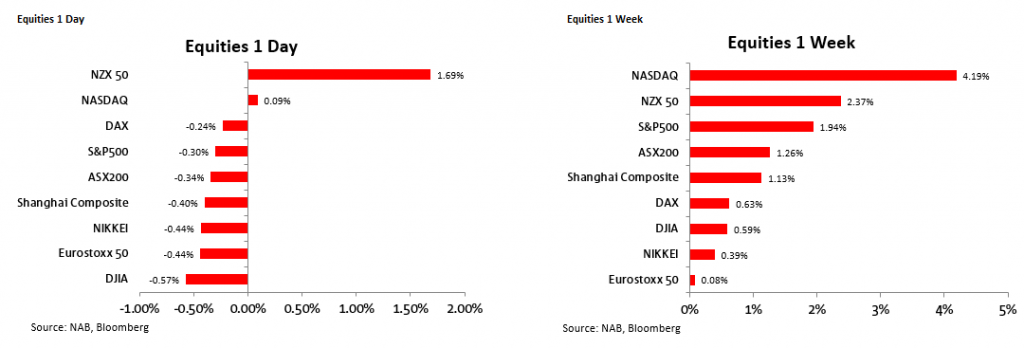

NASDAQ was the only US index not to end in the red Friday, albeit it was up less than 0.1%, with the technology sector again displaying ‘defensive’ qualities amid the negative covid news backdrop. In sharp contrast, the domestically focussed and smaller-cap Russell 2000 was down almost 3%, while the S&P 500 ended 0.3%. On the week though, the S&P ended nearly 2% higher and the NASDAQ up more than 4%.

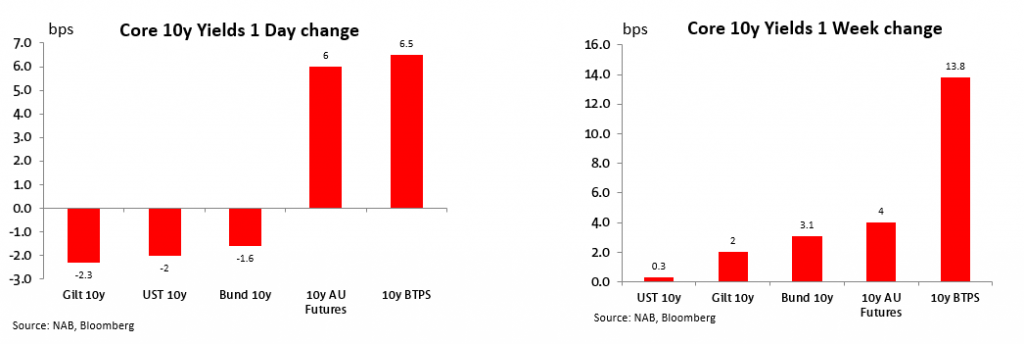

There was significant differentiation across countries Friday. US, German and UK Government benchmark yields were all close to 2bps lower at 10-years, while Italian bonds significantly underperformed on both the day and week, despite Italian PM Conte surviving a no-confidence vote but one consequence of which, some commentators suggest, will be looser than otherwise fiscal policy in order to keep the government intact with the support of other, more left leaning minor parties.

Australian bonds also significantly underperformed, with the AU-US 10-year spread up from -0.5bp to 2bps by the local close, and where our bond traders suggest one factor was contagion from the sharp (11bps) back-up in New Zealand 10-year yields following their much stronger than expected Q4 CPI print. This came in at 0.5% on the quarter (1.4% y/y) against 0.2%/1.1% expected, with the RBNZ’s favoured sectoral factor model of core inflation rising – unusually – to 1.8% from 1.7%. Australia’s CPI is on Wednesday.

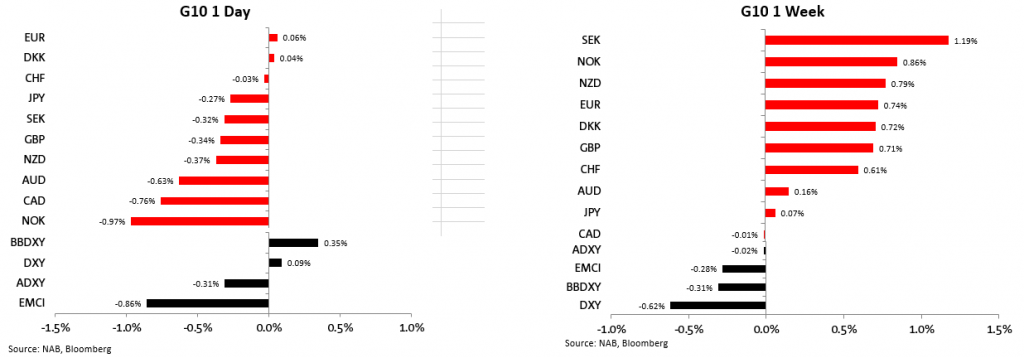

The EUR was the only major currency to buck the trend of a strengthening USD in association with the negative risk tone, ending up 0.06% and as a result limiting the rise in the EUR-centric DXY index to 0.12% against 0.35% for the broader BBDXY. EUR/USD rose early on in the European session, seemingly liking the fact the flash PMI data weren’t worse than they were, and didn’t seem to suffer much on the above negative EU vaccine roll-out news. A stronger EUR/GBP following the UK PMI data also may have helped.

The biggest casualties against a stronger USD Friday were the usual suspects, namely NZD, AUD, CAD and NOK, losses ranging from 0.4% (NZD) to 1.0% (NOK). On AUD, the weaker than expected preliminary December retail sales report (-4.2% against -1.5% expected) compounded the pressure coming from weaker equity markets.

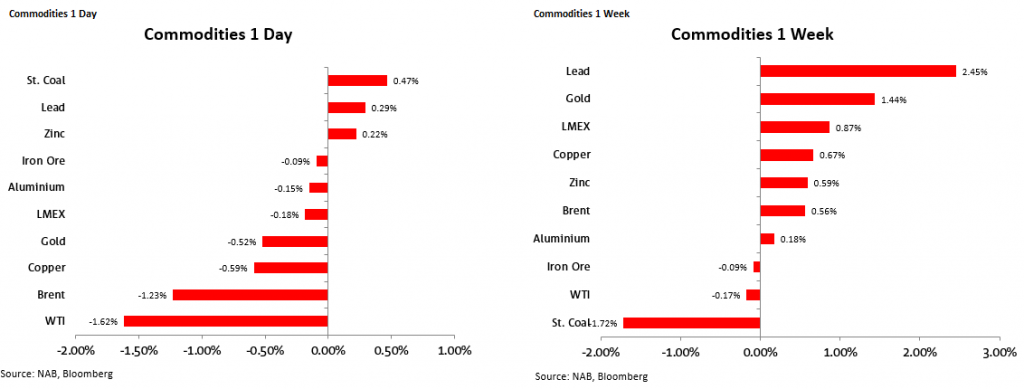

Oil suffered in conjunction with a firmer USD and risk off tone broader market tone, little impacted so far by Executive Orders from President Biden at the end of last week, namely the (widely heralded) cancellation of the Keystone XL pipeline that would have carried crude oil from the tar sands of Canada to Texas, and that only top Biden appointees can sign off on drilling permits for the first 60 days of his Presidency. Plus, according to a Bloomberg source story, that this week Biden will go even further and suspend the sale of oil and gas leases on federal lands (from where the US currently sources 10% of its supplies).

France Manufacturing PMI 51.5 from 51.1 (50.5E)

France Services PMI 46.5 from 48.4 (49.1E)

Germany Manufacturing PMI 57.0 from 58.3 (57.2E)

Germany Services PMI 46.8 from 47.0 (45.0E)

EZ Manufacturing PMI 54.7 from 55.2 (54.4E)

EZ Services PMI 45.0 from 46.4 (44.5E)

UK Manufacturing PMI 52.9 from 57.5 (53.6E)

UK Services PMI 38.8 from 49.4 (45.0)

UK Retail ex-auto fuel +0.4% m/m vs -2.6% (1.0%E)

US Markit Manufacturing PMI 59.1 from 57.1 (56.5E)

US Markit Services PMI 57.5 from 54.8 (53.4E)

US Existing Home Sales 0.7% from -2.5% (-1.9%E)

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.