We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Last week was a volatile one, but markets enthusiasm stemming from the hope of a vaccine led the charge, with some shifting of focus on equity markets.

https://soundcloud.com/user-291029717/vaccine-vs-infections-the-only-news-that-seems-to-matter?in=user-291029717/sets/the-morning-call

One step closer to knowing, One step closer to knowing – U2

Last week we came one (big) step closer to knowing whether there will be a suitably effective covid-19 vaccine(s) ready for mass roll-out in 2021, and on Saturday morning our time President Trump came a step closer to admitting he might have lost the election. The latter came after Georgia was called by the media for Joe Biden – albeit a manual recount is underway – the first time Democrats have won the state since 1992. In any event, Georgia wasn’t critical in the way Florida was in 2000 and means that with all states now called, Biden has 306 Electoral College votes to Trump’s 232 (almost identical to the 2016 outcome in Trump’s favour – 304 versus 227 for Clinton with 7 ‘others’). President Trump said on Friday evening that “This administration will not be going to a lockdown. Hopefully the . . . Whatever happens in the future, who knows which administration it will be, I guess time will tell.” Since then though, POTUS has been busy tweeting and shows no signs of conceding (e.g., “He only won in the eyes of the FAKE NEWS MEDIA. I concede NOTHING! We have a long way to go. This was a RIGGED election.”

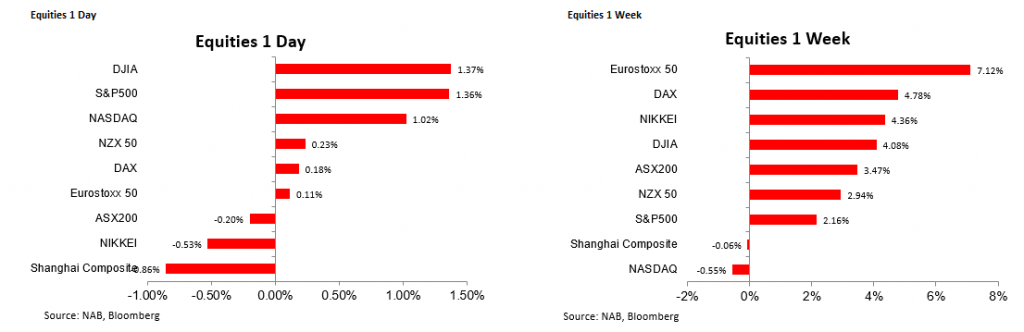

After a shaky end to Thursday, the latter driven by sharply higher covid infections rates – which reached around 180,00 on Friday – and news of impending new social distancing measures across swathe of America including potential school closures in New York (not yet confirmed), stay at home orders in Chicago, and similar in numerous other states or districts across north America. Friday saw gains of at least 1% in the major US indices, the Dow, S&P500 and Russell 2000 all doing better than the NASDAQ, so suggesting some further rotation out of what are now dubbed ‘stay at home’ technology stocks (of which Amazon and Netflix are among those at the vanguard) . Both the smaller cap Russell 2000 and the S&P500 made record closing highs.

Anticipation of more good news on the vaccine front this week (e.g. Moderna issuing results similar to last week’s Pfizer/BioNTech news, and a potential Emergency Use Authorisation (EUA) request from the latter, together with the some positive corporate earnings results (CISCO, Disney) carried the day Friday, and the vaccine news the entire week where the S&P ended up over 2% but the NASDAQ down more than 0.5% (to be the worst performing major index globally, the Shanghai Composite was the on other index showing a sown week, and then by just -0.06%).

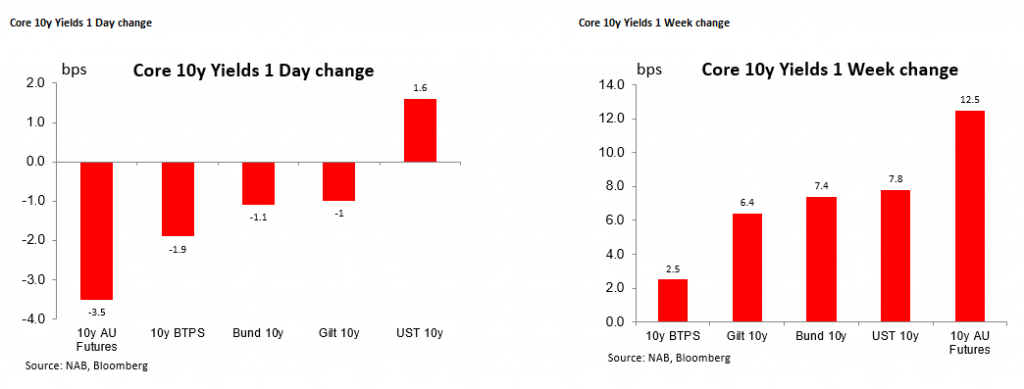

Bond market had a volatile week but benchmark 10-year yield globally were all higher on the week albeit back from Tuesday’s Pfizer-BioNTech-induced highs when 10-year treasuries hit 0.97%. The prospect of a world getting back to some semblance of normality later next year was the key diver; certainly there was no good reason for optimism regarding a near-term fiscal support bill being passed in the US, or any suggestion that if the Fed is going to be anything in the weeks or months ahead, it will be anything other than to further ease policy (e.g. by skewing its QE-bind purchases to longer duration bonds).

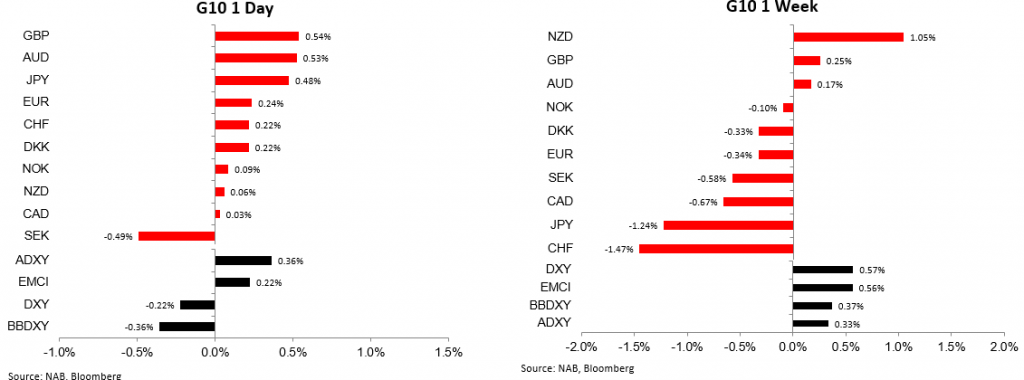

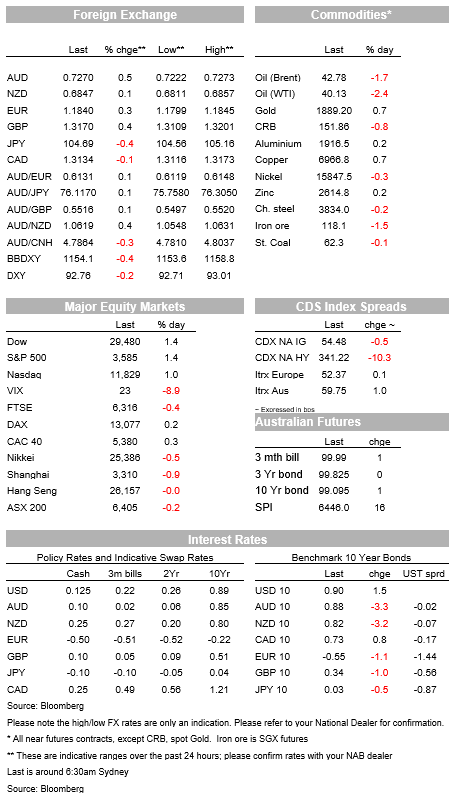

In FX Friday saw a reversion to the familiar spectacle of the USD easing back alongside improvement in risk sentiment and higher equities, though on the week the USD was a touch stronger despite it being an up-week for stocks. The BBDXY dollar index was 0.4% lower Friday and the narrow DXY index own 0.2%, weakness in the latter led by gains of 0.5% for both GBP and JPY, the former following news that UK PM Boris Johnson’s top policy adviser Dominic Cummings – the architect of the 206 Brexit referendum outcome – was exiting the stage (immediately, we learned later Friday).

This latter news was seen as potentially removing one obstacle to the UK side making the concessions necessary to tie up a UK-EU trade deal – if not as early as this Thursdays EU Summit. UK trade negotiator David Frost at the weekend was having none of this though. AUD also added back 0.5% on Friday to be one of the best performing G10 pairs. On the week, BBDXY was up 0.4% and DXY 0.6%, both its was nevertheless still a (small) up week for AUD/USD (0.2% to 0.7270).

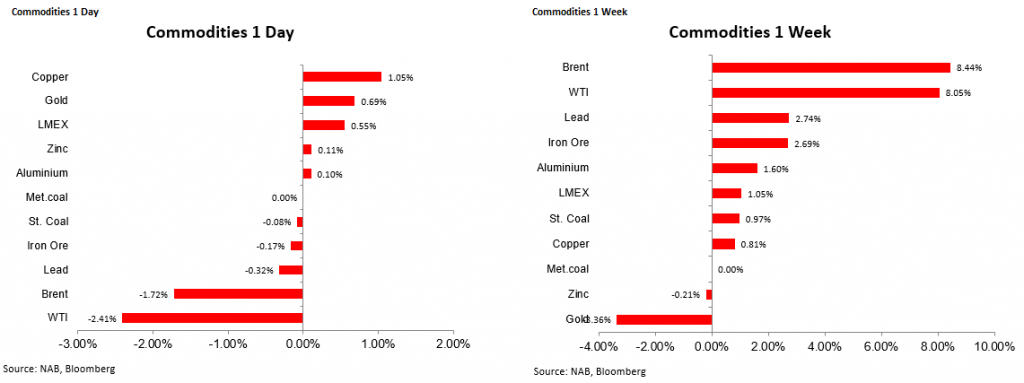

The commodity story last week was mostly about oil, both WTI and Brent benchmarks up over 8%, much of the rally being driven by anticipation of better demand side characteristics next year if a vaccine does indeed become widely available. Industrial metals also benefited from this line of thinking. Gold was a causality of the better performance by equities but modestly stronger USD, off over 3%.

Finally, economic data of note Friday was US producer prices, where final demand PPI came in at 0.3% m/m against 0.2% expected for 0.5% y/y up from 0.4%, with the core (ex-food and energy) reading 0.1% m/m below the 0.2% expected for 1.1% y/y down from 1.2%, and the University of Michigan preliminary November Consumer Sentiment Index. The latter fell to 77.0 from 82.8, the fall reportedly led by reduce confidence among Republican supporters (amongst Democrats, confidence was little changed).

Economic data of note Friday was US producer prices, where final demand PPI came in at 0.3% m/m against 0.2% expected for 0.5% y/y up from 0.4%, with the core (ex-food and energy) reading 0.1% m/m below the 0.2% expected for 1.1% y/y down from 1.2%, and the University of Michigan preliminary November Consumer Sentiment Index. The latter fell to 77.0 from 82.8, the fall reportedly led by reduce confidence among Republican supporters (amongst Democrats, confidence was little changed).

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.