Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

Ordinarily these numbers would be a cause for optimism in the markets, yet concerns of the impact of the coronavirus are having the opposite impact.

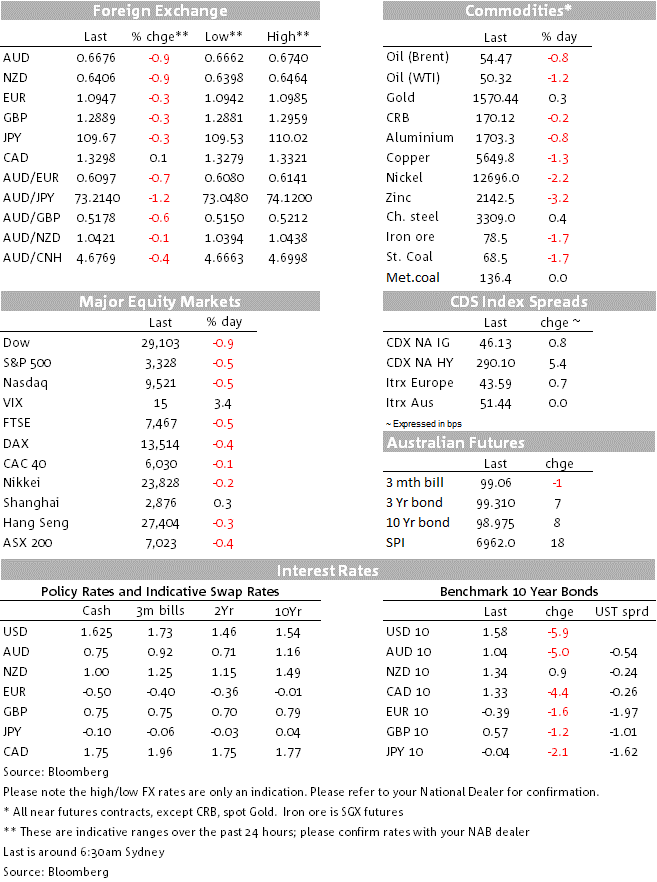

Coronavirus fears reignited on Friday, taking the gloss of what was a strong US Payrolls report. Bonds rallied with US 10yr yields falling -5.9bps to 1.58%, while markets extended pricing for Fed rate cuts with 1.5 rate cuts priced by the end of 2020 from 1.3 on Thursday. FX saw havens bid with USD/JPY -0.3% to 109.66, while the USD hit a new 2020 high with the DXY +0.2% to 98.70. Woeful European industrial production figures also highlighted the US’ continued relative outperformance and Europe’s trade exposure to China – EUR and GBP both fell -0.3%.

The AUD (-0.9%) and NZD (-0.8%) underperformed, both being China and global growth proxies, with the AUD hitting its lowest level since 2009 at 0.6662. As we open the AUD is currently trading at 0.6675 and with little domestic data scheduled, will be buffeted by global headlines. As for the Coronavirus itself, 813 people have now died with the death toll now exceeding SARS (which resulted in 774 deaths). The implied mortality rate at around 2% though remains considerably lower and this week will be closely watched to see whether recent containment measures have been effective – note the virus has an incubation period of 2-14 days with extensive lockdown implemented in China in late January. We will be watching the pace of new infections closely. Markets also assessing the economic impact of containment measures with many cities and provinces in lockdown until at least February 17.

A strong US payrolls print had little impact on markets, suggesting the coronavirus was the predominant force on markets. Payrolls rose 225k, well above the 165k consensus, though the whisper into the report was for a strong number given the ADP numbers earlier in the week. While the unemployment rate did rise a tenth to 3.6%, this came from a rise in the participation rate which rose two-tenths to 63.4%. Wages growth was also stronger than expected at 3.1% y/y against the 3.0% consensus. One soft bit out of the report were the benchmark revisions to the level of payrolls which was revised down by 514k at March 2019. As a result the pace of payrolls growth did not accelerate when President Trump was elected – though the pace of Payrolls growth has of course remained strong over the past few years.

US relative outperformance continued with weak industrial production figures out of Europe. German industrial production fell -3.5% m/m in December and is down -6.8% y/y compared to -3.7% expected. The figures out of France also disappointed, falling -3.2% y/y against +1.2% expected. Weak factory orders earlier last week also suggests little prospect of an industrial recovery in the short-run. The figures may also mean a downward revision to Eurozone GDP growth which grew by just 0.1% q/q in December (note Europe gets a second read on Q4 GDP on Friday). Europe is heavily exposed to global trade with German exports making up around 47% of German GDP.

Its no surprise then to see EUR and GBP weaker, both down by around -0.3%. Given Europe’s high trade exposure, EUR may weaken further should Coronavirus or global growth fears intensify.

One surprising move, or lack of a move has been USD/YEN. While it did fall -0.3% on Friday, it had until then been relatively stable despite Coronavirus scares. The Nikkei Asian Review reports speculation of Japanese authorities selling the yen, using cash from the Government Pension Investment Fund in a piece titled “Japan’s pension whale suspected of harpooning the yen” (see link for details).

RBA’s Lowe on Friday reiterated he was willing to be patient if there continues to be sufficient progress in meeting the bank’s inflation and full employment objectives. The time frame to meet those objectives has seemingly lengthened with Governor Lowe becoming concerned again on financial stability and the potential that lower rates may lead to a pick-up in already high household debt. Interestingly, Dr Lowe also noted the bank had estimated the cash rate would need to be cut by 300-400bps to return inflation to the 2.5% mid-point over the next couple of years given the flatter Phillips curve. Markets though are more sceptical, especially in light of the potential of the coronavirus to impact. As one well-connected RBA whisper wrote on the weekend, the RBA has taken a cautious view and has “essentially excluded the virus [from its outlook] but fully aware that the virus could dramatically change it”. Markets currently do not fully price a rate cut until September, though are 50% priced by around May. NAB continues to see the RBA cutting rate twice this year.

It’s a quiet start to the week with no data scheduled for Australia. There is also little in terms of global events with only the Chinese CPI/PPI of note, while Japan has the EcoWatchers survey and the Fed’s Harker speaks later tonight.

Further out in the week the highlight out of the US is Fed Chair Powell’s testimony to congress on Tuesday (House) and Wednesday (Senate). Likely dovish Fed Governor Nominee hearings are also on Thursday with Waller and Shelton appearing. Datawise the US also has the CPI (Wednesday) and Retail Sales (Friday) scheduled, while focus will continue on politics with the New Hampshire Primary on Tuesday – all focus on Sanders and Buttigieg who topped the Iowa Causses and on Biden who unperformed.

For Australia, it is a fairly quiet week with the NAB Business Survey for January on Tuesday and Housing Finance figures.

In NZ the RBNZ meeting on Wednesday will be watched closely for the RBNZ and my colleagues at BNZ note that the market is likely to sustain its easing bias view of the RBNZ given it will have to acknowledge mounting risks from the coronavirus, despite a strong labour market and firming inflationary undercurrents.

Finally in Europe, a second-read on Q4 GDP on Friday may see downward revisions given the woeful industrial production figures on Friday.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

Conditions ease as slow growth weighs on firms

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.