Coming in for landing in a heavy cross wind

Insight

Coronavirus continues to cause concerns, hitting all asset classes overnight, including US and European equities.

https://soundcloud.com/user-291029717/virus-hits-equities-slower-growth-for-us-boe-on-hold

This is the end, my only friend, the end. It hurts to set you free. But you’ll never follow me – The Doors

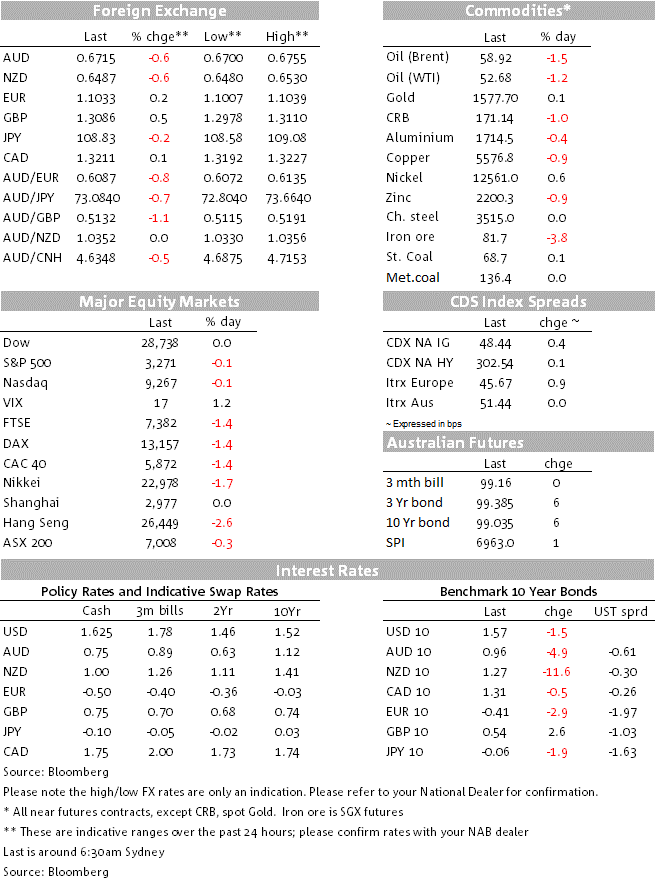

It seems ironic that on the day that the UK is finally set to legally end its 46-plus year membership of the European Union, Sterling sits at its best levels against the Australian dollar since the day of the June 2016 Referendum result. At around 0.5130, AUD/GBP is currently some 20% down on its post-referendum highs.

In truth, this is not a lot to do with judgement on the efficacies – or otherwise – of Brexit – as the fact the market was priced 50:50 for a Bank of England rate cut that the ‘Old Lady’ chose not to deliver, and by a more convincing 7-2 majority than the market had collectively reckoned on (6-3 or tighter). GBP gains post the BoE look to have had a positive contagion effect on EUR/USD, up a quarter of a percent to 1.1038 and meaning that the DXY index is 0.16% lower at 97.8 to currently sit slap bang in the middle of its October 2019-January 2020 range

EUR gains also look to owe something to some slightly better than expected Eurozone economic new overnight, specifically small rises in Economic and Industrial Confidence in the January EU Commission surveys and a dip in the unemployment rate to 7.4% from the (unchanged) 7.5% expected. Ahead of today’s Eurozone CPI (and Q4 GDP) figures, German HICP rose to 1.6% from 1.5%, versus 1.7% expected.

AUD and NZD are maintaining their status as the whipping boys for NCOv-related China and global economic and market angst, both 0.7% lower in the past 24 hours, AUD to a low of 0.6700 and NZD 0.6482, the latter its first time below 0.65 since December 3 last year. JPY and CHF continue to display their favoured safe-have characteristics, up 0.4% and 0.3% respectively against the greenback.

US GDP was the main economic event overnight, the Q4 read coming in at 2.1%, exactly the same as Q3 and versus the 2.0% official consensus but where the whisper number was a little shy of this, especially after the jump in the December trade deficit reported earlier in the week. The details show personal consumption rose at a 1.8% annual rates (payback for an unsustainably strong 3.2% Q3 rate) inventories subtracting 1.09%, offset by net exports, which added 1.48% pts. Housing investment added 0.21%pts, confirming this to one of the brightest sectors of the economy at present.

NCoV continue to plague markets, with the S&P500 down 0.5% and European stocks ending their day on average about 1.5% lower. Materials continues to be among the hardest hit S&P subsector (-1.25%) reflecting global growth concerns. Commodity prices continue to tumble, oil off between $1.00 (WTI) and $1.30 (Brent). Bloomberg reported that Saudi Arabia wants to bring forward the OPEC+ meeting from March to February – likely to endorse supply cuts to support oil prices – but this has been resisted by Russia so far. Base metals bar nickel are all lower (LMEX -0.7%) and Singapore iron ore futures down 3% to $81.50.

The World Health Organisation has just declared that the coronavirus constitutes a public health emergency of international concern, though it falls short of recommending limiting trade or people movement due to the virus outbreak. The announcement hasn’t added additional downward pressure to either US stock prices or bond yields. The latter sees 10-year Treasuries currently at 1.556%, down 2.7bps with the 3-month-10-year treasury cure re-inverting (-1bp) for the first time since October 11 2019.

RBA December Private Sector Credit (expected +0.2% m/m), PPI (11:30 AEDT)

China Official Jan PMIs @ 12:00 AEDT (manufacturing seen at 50.0 from 50.2, services 53.0 from 53.5, but presumably won’t pick up any of the early impact of the coronavirus)

ANZ NZ Consumer Confidence (8:00 AEDT)

Japan Tokyo Jan CPI, Dec unemployment and retail sales

Offshore tonight: EZ Q4 GDP (expected 0.2% q/q); EZ preliminary Jan CPI; US Dec PCE data, final UoM consumer sentiment

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.