A private sector improvement to support growth

Insight

The markets slipped momentarily into risk-off as the number of COVID-19 infections jumped in volume, but concern slipped back a little as it became clear that the way cases were being measured had changed.

https://soundcloud.com/user-291029717/virus-worries-uk-chancellor-quits-euro-falls-further?in=user-291029717/sets/the-morning-call

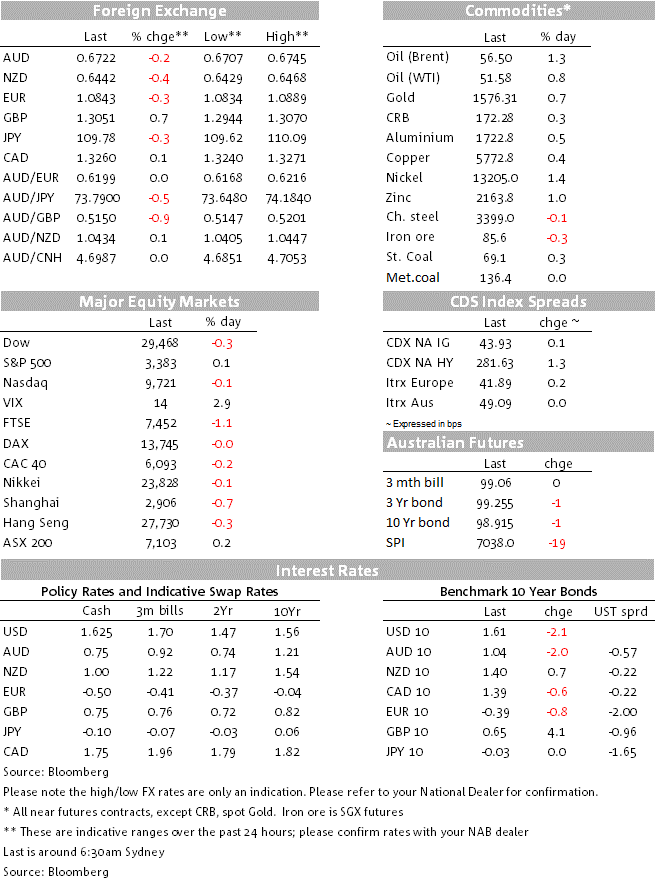

Anyone who spent their formative years in the UK and most Friday night’s in the pub will have memories of this late night, low budget, often surreal and invariably mindless magazine TV show, fronted by Antoine de Caine’s and Jean Paul Gaultier (yes him). A colleague in the NAB dealing room was reminiscing about it yesterday for reasons unbeknown, and looking at the overnight FX screens this morning it seemed an appropriate title for today’s missive. EUR/USD has fallen to its lowest levels since 24 April 2017 and sits perilously close to the bottom of 1.0825-1.0865 potential support zone we identified in our latest Global FX Strategist published on Tuesday. AUD/EUR has nudged back above 0.62 for the first time in three weeks despite AUD being one of the hardest hit currencies by all this year’s virus news. AUD/USD itself is about 10 pips down on this time yesterday at 0.6725.

There hasn’t been any significant ‘new news’ to drive the Euro lower. Indeed it isn’t Thursday’s worse performing G10 currency, NOK, SEK and NZD all a touch weaker having suffered more from the abrupt U-turn in risk sentiment after yesterday morning’s news of sharply higher COVID-19 infection rates in Hubei province reported under new – less stringent – diagnostic methodologies. Though on a ‘like-for like’ basis, the increase was reported to be 1,508 vs.1,638 the day before, the 14,840 Feb 12 figure representing the accumulation of many days’ worth of cases not previously classified as COVID-19, the news nevertheless played to suspicions that the true number of cases is dramatically higher than officially reported and that it is going to take longer than just a few weeks before business can return to anything like normal in China, including international travel bans for Chinese nationals imposed by various countries.

The Australian this morning reports on a survey of more than 16,000 Chinese students stranded in China by the travel ban which found nearly a third of them (32 per cent) would enrol in another country if they were prevented from studying in Australia in the first semester of this year. The paper notes that if all of the roughly 100,000 Chinese students who are expected to study in Australian universities this year have to postpone their study in the first semester, universities face losing up to $2bn. subscriber link

And the scraps of news we have had weren’t negative, unemployment in mainland France reported to have fallen to 8.1% from 8.5% (ILO basis) and the European Commission maintaining its Euro-area growth forecast at 1.2% for both 2020 and 2021. These numbers don’t though look to have factored in the likely headwinds from COVID-19 or sees those as transitory (either that or we’ll see a big after-the-fact downgrade in the next Spring forecasts in three months’ time).Also, and quite unbelievably, the Commission has revised up its growth forecast for Germany to 1.1% in 2020/21 vs 1.0%. France is seen at 1.1% and 1.2%, down from 1.3% and 1.2% (0.2% down in 2020) and Italy also lower at +0.3% and 0.6% down from +0.4% and 0.7%

The bigger news overnight has been a significant boost to all things GBP following a UK Cabinet reshuffle in which Chancellor Sajid Javid has resigned. The news here is that Javid quit due to requests from PM Johnson and others that would have meant significant changes to the Treasury department (i.e. removal of several advisers) – changes which Javid evidently would not accept. He is replaced by ‘rising star’ Rishi Sunak (a Goldman Sachs alumni) and which has market speculating that the new Chancellor will be friendlier towards fiscal expansion. Sunak’s voting history in Parliament suggests that his views are more aligned to Johnson’s than Javid’s were, and he is a supporter of corporate tax cuts, lower capital gains taxes and increased infrastructure investment. GBP/USD is over cent higher at 1.3055 and AUD/GBP almost one per cent lower near 0.5150. UK gilts yields have bucked the trend of lower yields elsewhere with the 10 year up 4bps versus falls averaging 1bp for 10 year treasuries and German Bunds. The US Treasury has just successfully sold 30 year bond at about 1bps below the pre-auction market yield.

US equity markets are narrowly mixed into the last hour of NYSE trade, the Dow currently -0.3% while the S&P500 is +0.1% and the NASDAQ -0.1%. The Dow has been hit in particular by a 5% fall in CISCO, who while meeting or beating its revenue and earnings estimate for the quarter, warned of falling orders and so lower future quarters’ revenue.

US data saw January CPI come in 0.1% below expectations in headline terms at 0.1% but 0.2% as expected for core (ex food and energy), keeping the yr/yr rate steady at 2.3% (core CPI runs about 0.5% above the Fed’s preferred PCE deflator inflation measure). Also, weekly jobless claims remained low at 205k vs. 203k the week before.

Mexico has just cut rates, by 0.25% to 7.0%, a move universally expected and the 4h Emerging Market country (I think) to either cut rates or otherwise ease monetary policy (Singapore) since the COVID-19 outbreak.

NZ BusinessNZ manufacturing PMI (08:45 AEDT) – has it lurched down further after falling below 50 in December?

Tonight Germany Q4 GDP (estimate 0.1% q/q); EZ Q4 GDP (estimate 0.1%) will confirm the soft end to 2019 and which presages a likely soft, virus-impacted Q1 2020.

US Jan Retail Sales (expected 0.3% in both ex-auto and ex-auto and gasoline terms); Industrial Production (seen -0.2%); and the Feb preliminary UoM Consumer Sentiment index (forecast at 99.4 from 99.8.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

A private sector improvement to support growth

Insight

Online retail sales growth accelerated 1.1% in April

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.