Coming in for landing in a heavy cross wind

Insight

In Australia yesterday, WPI wages data showed less wages pressure than feared. WPI grew 0.8% q/q and 3.3% y/y, 0.2ppts below the market consensus and RBA expectations.

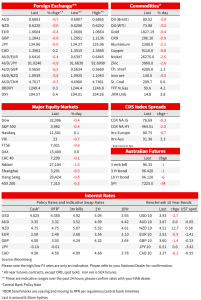

US yields a few bps lower across the curve, though a selloff led by the front end following the minutes have seen the decline in yields pared in the past hour or two. Equities swung into the red from modest gains after the release of the Minutes, which confirmed all participants anticipated ongoing increases in the months ahead. Elsewhere, the AUD underperformed, down 0.7% to 0.6803 and RBA pricing was pared a little after softer-than-expected wages data yesterday. That stands in contrast to news from Japan that large automakers are delivering faster wage gains.

Out at 6am was the FOMC minutes. With Bullard and Mester revealing they favoured 50bp at the end of last week, more widespread agitation for a larger rise at the first meeting of 2023 was a risk, but it did not eventuate. Instead, “almost all participants” favoured the 25bp move, and only ‘a few’ favouring or ‘could have supported’ a larger move. The slower pace of hikes “ would allow for appropriate risk management as the Committee assessed the extent of further tightening needed.” That’s not to say the Minutes read as dovish, and indeed US yields and fed terminal pricing are a little higher after their release.

Consistent with the chorus of Fed messaging, there is more to do. “All participants continued to anticipate that ongoing increases in the target range” and “a number of participants observed that a policy stance that proved to be insufficiently restrictive could halt recent progress.” Participants will also be in no rush to retreat from restrictive settings, “ Participants observed that a restrictive policy stance would need to be maintained until the incoming data provided confidence that inflation was on a sustained downward path to 2%.”. Also of note is the absence of any mention of ‘disinflation’ in the Minutes, which contrasts Powell’s press conference where he noted many times that the disinflationary process was underway. Earlier, Bullard in a CNBC interview said “I think we are going to have to get north of 5%. Right now I’m still at 5.375%” in line with his other recent commentary.

US equities are currently in negative territory. after the S&P500 ranged from a loss of around 0.4% to a gain of around 0.4%, and back to a 0.4% loss after the reaction to the minutes.

US yields were lower over the past 24 hours despite a modest selloff following the Minutes. The US 2yr is 3bp lower from around the highs of 4.73% reached yesterday, its highest since November. That is after a 3bp pop higher out of the minutes. The curve had steepened ahead of the minutes, though a larger reaction in the front end on the Minutes reiteration of the higher-for-longer messaging sees the 2yr and 10yr both down around 3bp. The 10yr is now around 3.92% after pushing to new post-October high near 3.97% intraday. There were small moves in yields in Europe, with 10yr Bund and Gilt yields each down 1bp.

In FX markets, the dollar is 0.3% higher on the DXY. The AUD was 0.7% lower, the worst G10 performer on the day and now sits around 0.6804, the lowest it’s been since January. That contrasts the NZD, which was flat against the dollar over the past 24 hours, the diverging fortunes among the antipodeans attributable to the softer wages print in Australia and the firm hand of the RBNZ in New Zealand yesterday (more below). The only currency in the green against the greenback was the yen, up 0.1%, with USD/JPY at 134.92 after trading higher against the backdrop of rising yields and USD strength in recent weeks.

In Japan, the longevity of current YCC policy remains subject to speculation. The Japanese 10yr yield pushed above the 0.5% ceiling for the second day, reaching 0.505%. The BoJ said it would buy ¥300 billion of five-to-10 year notes and ¥100 billion of 10-to-25 year debt on top of the standing offer to buy 10-year notes at a fixed yield of 0.5%. Former BoJ Board member Makato Sakuri said a March move was unlikely and that the earliest timing incoming Governor Ueda may move is around the middle of this year, after confirming a virtuous cycle between wage growth and inflation. With a lift in wages pivotal for the sustainable lift in inflation the BoJ seeks, there were positive signs from large automakers. Toyota and Honda agreed to union demands for higher wages, the former not disclosing the amount but noting it was the largest hike in two decades and Honda disclosing a 5% lift in wages, the largest increase in base pay in three decades.

Yesterday, the RBNZ raised the OCR by 50bps to 4.75% as widely anticipated and there was only a minor tweak to the projected track, with the peak still assumed to be 5.5% but taking slightly longer to get there. The RBNZ will rightly try to look-through the near-term inflationary impact of Cyclone Gabrielle and suggested that it didn’t materially alter the outlook for monetary policy. Our BNZ colleagues detected a slight softening of tone through the minutes compared to November, reflecting the fact that policy was now more overtly contractionary. Market reaction was muted by the lack of genuine surprise in the announcement.

In other economic news, Germany’s IFO business survey showed a fifth consecutive monthly improvement in expectations, rising a couple of points to 88.5. But the index remains at a historically subdued levels despite the more than 10 point rebound from the September trough and the current conditions component dipped slightly to 93.9 form 94.1 and not seeing the actual activity uplift apparent in yesterday’s PMIs.

In Australia yesterday, WPI wages data showed less wages pressure than feared. WPI grew 0.8% q/q and 3.3% y/y, 0.2ppts below the market consensus and RBA expectations. The slower-than-expected rise in base wages takes some of the heat out of the spectre of price-wage persistence that could know the economy off the path to a soft landing but won’t dissuade the RBA from more hikes in the near term (see our write up of the data here AUS: WPI pressures not as bad as feared but RBA still has work to do). Australian yields were heading higher into the release but bounced lower on the data. 3yr futures implied yields dropped from an intraday high of 3.82% to as low as 3.54% in the hours after before settling around 3.58% and little changed on the day. Terminal RBA pricing came in around 5bp to 4.22% from 4.27%.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.