Confidence and Conditions Lift

Insight

There isn’t an immense amount of confidence about how quickly economies will recover.

https://soundcloud.com/user-291029717/wait-and-see?in=user-291029717/sets/the-morning-call

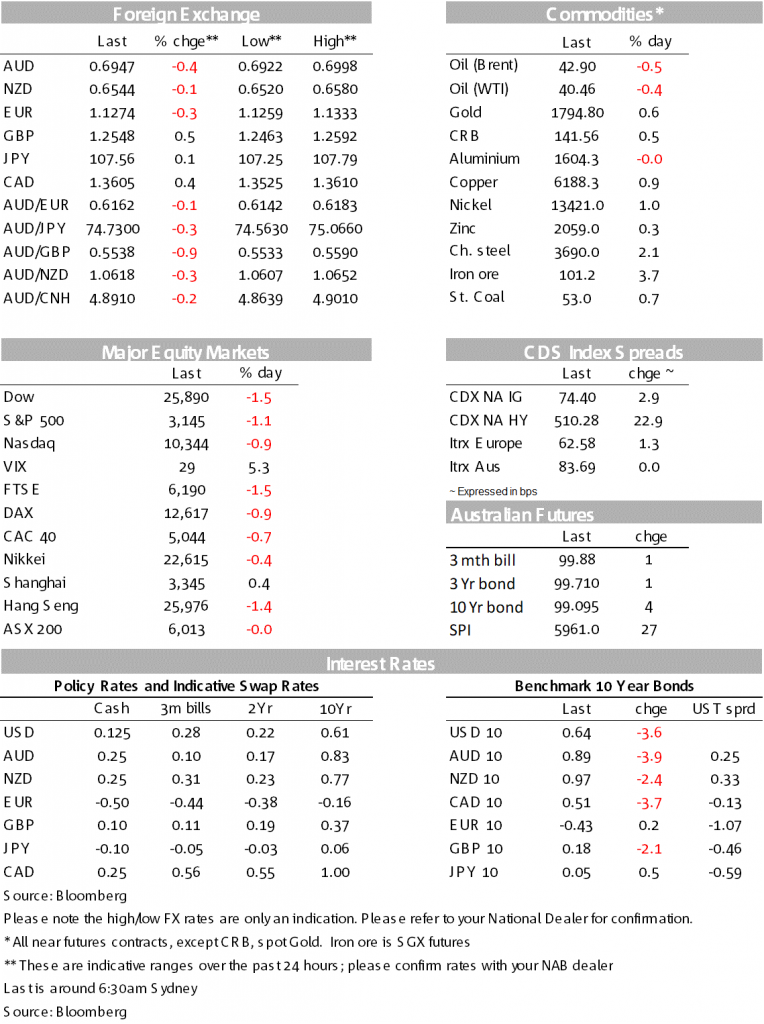

Risk appetite softened led by questions over the pace of the recovery with Fed officials observing high-frequency data is “levelling off”. Moves mostly consolidation within ranges with stocks down (S&P500 -1.1%), the USD rebounding (DXY +0.2%) and the AUD (-0.4%) underperforming on the Melbourne lockdown and sabre rattling from China.

“All my life; You stood by me; When no one else was ever behind me; All these lights; They can’t blind me; With your love, nobody can drag me down” One Direction, 2015

Risk sentiment softened overnight with questions being asked about the pace of the recovery. Those questioned were initially driven by the Fed’s Bostic in an FT interview who said he was seeing a “levelling off” in economic activity in terms of business openings and mobility and that “we’re watching this very closely…” (see FT for details). The Fed’s Mester reinforced those comments later in the session, stating “over the past week or so, there’s been some levelling off, and I think it’s probably due to the increase in cases” (see CNBC). While questions are being asked about the pace of recovery, the moves overall are far from risk-off and looks more like consolidation with markets still largely in “wait and see mode” ahead of the upcoming earning season later in July.

Virus news remains mixed with lockdowns re-imposed in Melbourne, but in the US rising hospitalisation rates are so far not translating into a pick-up in deaths. Some US analysts are tentatively concluding that if healthcare systems are proving resilient, then do we need as severe restrictions? It will be important to watch the number of US deaths in coming weeks and whether greater questions will be asked about the extent of necessary restrictions (in the US at least). Also in virus news, the US has allocated more funds towards vaccine development with Novavax awarded a $1.6bn contract.

Market moves were relatively modest even with the softening in risk sentiment. Equities fell with the S&P500 -1.1%. Highlighting the uncertainty over the pace of the recovery, stocks most exposed to re-opening underperformed overnight with airline stocks -5.0%. The USD rebounded with DXY +0.2%. The AUD underperformed, down -0.4% on a tougher than expected Melbourne lockdown (6 weeks as opposed to the initially speculated 4 weeks) and more sabre rattling from China. There was no impact from yesterday’s as expected RBA meeting. A Global Times Editorial warned the “Australian economy will have a bitter pill to swallow over possible HK immigration offer” (see Global Times). Similar soundings were given to the UK over its decision to begin phasing out Huawei equipment in the UK’s 5G telecommunications networks as soon as this year. Despite that, GBP outperformed overnight with Cable +0.6% as a surprise informal dinner occurred between UK and EU negotiators last night – details though are yet to emerge. Yields edged lower with the US 10yr -3.6bps to 0.64%.

With only German Factory Orders and US JOLTS of note. German Factory orders rose, though disappointed expectations with a rise of 7.8% against 11.1% expected and is currently -19.3% y/y. Also in Europe, the European Commission’s latest forecast for bloc were downgraded to a -8.3% contraction, against a prior expectation of -7.4%. The rebound in 2021 was also pared back to +5.8% from +6.1%. Officials noted “The economic impact of the lockdown is more severe than we initially expected. We continue to navigate in stormy waters and face many risks, including another major wave of infections”.

Job openings for May were 5.4m against expectations of 4.5m, though openings are still down -23% since Feb. It is also worth noting openings increased the most in sectors that are now seeing a rolling over in activity – including in accommodation and food services, and retail and construction. The ratio of openings-to-unemployed was 26%, indicating it may take some time for unemployment to fall.

There’s some talk that Melbourne’s 6 week lockdown may see changes to the government’s Economic Statement that was planned for 23 July which includes the next phases of the JobKeeper and JobSeeker Supplement schemes (both schemes currently expiring at the end of September). One hint of where we could go is the announcement by banks that they will extend repayment holidays where necessary, by up to four months. The initial six month repayment holiday was due to expire come end September. As of mid-June 1 in 14 mortgages were on repayment holidays, though recently around 20% of those had started repayments. The AFR also notes superannuation withdrawals are also on the rise with total withdrawal approvals now $27bn as at Jul 5 (equating to 2.4m people), with a sharp acceleration in withdrawals over the past seven days as round two (the second lot of $10,000) of the withdrawal is made available. Note total withdrawals are likely to exceed the $29.5bn forecast by Treasury.

Quiet day with no data scheduled domestically. In virus news, Metropolitan Melbourne’s 6-week lockdown starts from 1.59pm on Wednesday 8 July, midnight tonight. Offshore it is also quiet:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Confidence and Conditions Lift

Insight

Online retail sales growth slowed in May following a fairly strong April

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.