A major global investment fund is using NAB’s financial innovation for derivative portfolios to help incentivise sustainability goals in a new deal for the Australian market.

Article

Markets have bounced back a little even though the battle over oil seems to be getting worse.

https://soundcloud.com/user-291029717/waiting-waiting-waiting-on-stimulus-news?in=user-291029717/sets/the-morning-call

“Now that it’s raining more than ever; Know that we’ll still have each other; You can stand under my umbrella” , Rihanna 2007.

Markets were crying out for a co-ordinated response to COVID-19 headwinds and over the past 24 hours those prayers are closer to being answered. While details remain very thin, President Trump has flagged a fiscal response (late Monday), Italy has upped its €16bn package, Canada is set to unveil a package, Australia will unveil one on Thursday according to the AFR (see link), and the UK looks like it will unveil one in tonight’s budget. Supervisory authorities are also co-ordinating with the US Treasury convening a meeting with the Fed, and SEC to discuss the impact of the virus on markets. President Xi’s visit to Wuhan also added to the improved tone tone yesterday with China watchers taking this as a sign that Xi believes victory over the virus is within reach.

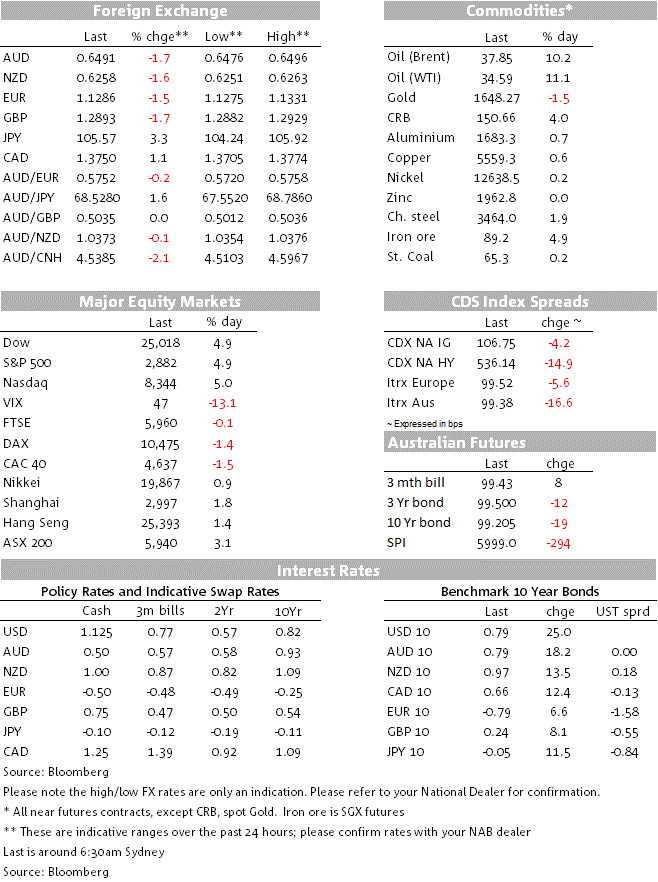

Stocks rallied hard, with the SP500 +4.9% to 2,882 after Monday’s -7.6% decline. There has been some intra-day volatility with the details of a US fiscal response still being formulated. President Trump is said to want a payrolls tax cut and support for the airline and cruise industries. Democrats have pushed back saying the answer is not another tax cut, but for measures to help those most affected by the virus such as paid sick leave and improved access to testing. Speaker Pelosi has said there will be ongoing conversation between Democrats and the Administration (see WSJ for details). Given the headwinds, it is likely a bi-partisan consensus will emerge, though the exact formulation of a package is yet to be determined. Despite a fiscal response, markets still price aggressive Fed easing with 72bps priced for the March 17-18 Fed meeting. Bonds sold off with US 10yr yields +25bps to 0.79%.

The USD surged with DXY +1.5% with broad-based gains. Risk haven currencies sold off with USD/JPY +3.2% to 105.46 and USD/CHF +1.5% to 0.9383. Other pairs saw similar moves with EUR -1.5%, GBP -1.6%, and NZD -1.6%. The AUD underperformed slightly, -1.8% to 0.6489. There was no driver for the underperformance apart from perhaps greater speculation around the RBA undertaking QE given recent backgrounding of journalists. The latest overnight was an MNI sources piece that said QE will be assessed in light of the government’s fiscal plans (to be published on Thursday) and that the Bank has no set formula on the quantity of bonds it could buy. It also notes the RBA is optimistic that Chinese production can ramp up quickly and limit disruptions to the domestic Australian supply chain. Markets continue to almost fully price an April rate cut to 0.25% (95% priced), while the terminal cash rate indicates markets expect a QE package to be announced by July 2020 (in QE programs overseas overnight cash rates have tended to trade towards the lower end of the target).

COVID-19 headlines continue to be on the negative side. Italy has expanded its lockdown to be nationwide, shutting schools for a month and introducing a curfew to close bars and restaurants at 6pm. Italian COVID-19 cases have now breached 10,000 and in the US, the CDC has reports the window for fully containing the virus has passed in some parts of the US. Small parts of the US are also now going under lockdown with NY deploying the National Guard in a three-square mile area of Westchester County. Should extensive lockdowns occur in the US, it is not hard to imagine a reversal of today’s moves. Markets accordingly are likely to remain volatile.

A preliminary read on the ANZ’s Business Outlook Survey for March painted a dire picture with a slump in confidence and activity indicators. The important own-activity indicator fell to a net -12.8%, a level consistent with an economic recession. We will also get credit card spending data for Feb from NZ today which will provide another indicator whether COVID-19 fears are weighing on the consumer. RBNZ Governor Orr also played down the prospect of imminent action, stating “time is on our side” and that “we don’t need a kneejerk” monetary policy reaction. Markets have accordingly slashed expectations of aggressive easing in March to 25bps rather than the 50bps that was being priced yesterday.

The US NFIB survey which largely pre-dated COVID-19 concerns in the US rose to 104.5 from 102.9.

The oil price rose sharply with WTI +11.3% to $34.65. There doesn’t appear to be catalyst apart from overall improved market sentiment and a notion that Monday’s moves were overdone. Saudi Arabia double-downed on its pledge to raise supply, saying it would supply more than 12.3m barrels a day in April, more than initially indicated last week. Russia also said it could raise production by another 0.5m barrels a day. US Shale drillers are said to be nervous given the low price with most explorers said to be going into “maintenance mode”. US production will likely start to fall given shale production requires new wells to be drilled to maintain output.

A busy day where two usually second-tier data pieces may give some insight into the extent of the likely slowdown in consumer spending. In NZ Credit Spending for February will be closely watched as will Consumer Confidence in Australia. RBA Deputy Governor Debelle also speaks, but it is unclear whether he will unveil anything significant in terms of policy. Markets will be tuned in for any Q&A that veers towards QE and other policy actions. Globally, most data is for January and thus is considered dated, while focus will continue on the size of flagged fiscal packages – note the UK has its budget tonight.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

A major global investment fund is using NAB’s financial innovation for derivative portfolios to help incentivise sustainability goals in a new deal for the Australian market.

Article

Price growth edges lower despite reasonable economy

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.