Online retail sales growth slowed in May following a fairly strong April

Insight

The markets reacted sharply to weaker than expected payrolls data from the United States.

https://soundcloud.com/user-291029717/weak-jobs-data-trade-tensions-and-a-brexit-to-nowhere

Take your pick from US equities, US bonds yields or the Aussie dollar with respect to today’s title (oh and give me Tom Waits’ version (who penned it of course) over Rod Stewart any day.

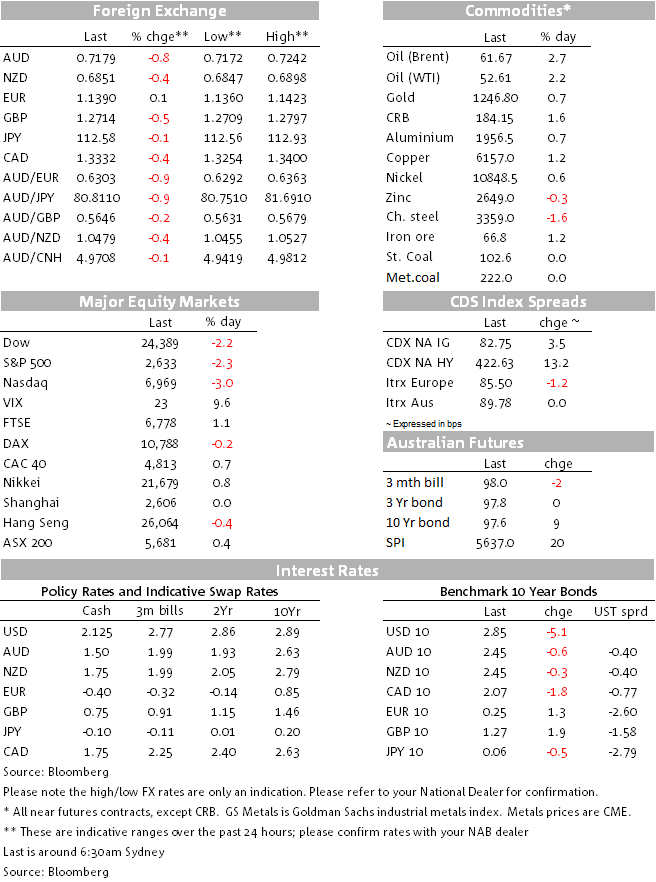

Weaker than expected US payrolls (+154k) still-benign earnings growth (3.1%) and an unchanged 3.7% unemployment initially drove US bonds yields and the US dollar lower Friday (while a much stronger than expected Canadian labour market report and, later, higher oil prices drove Canadian Dollar outperformance against all other G10 currencies). Progressive weakening in US stocks throughout the session – NASDAQ ending -3% – ensured that bond yields stayed down, while the USD drew support from its safe have attributes (VIX +2 to 23) to end just 0.1% lower (DXY), pushing the Aussie back down in the process.

The Huawei ‘affair’ – that over the weekend has seen China summon the US ambassador – related worries about the fate of Sino-US trade talks, concerns about growth now both in the US and the rest of the world, is plaguing stocks at a time when year-end book closings are now effectively no more than two weeks away. Lael Brainard is the last FOMC official to weigh in the comments that are consistent with the notion that while a December rate hike is still pretty much a done deal, but that thereafter data-dependency takes over from the ‘auto-pilot’ that has been running the Fed show for the last couple of years.

In sharp contrast to Thursday when US stocks recoupled almost all of their +/-3% intra-day losses, it was pretty much one-way traffic down for US indices on Friday and which all closed near the lows – S&P and Dow down by about 2.25% and the NASDAQ by just over 3%.

So the ‘Huawei affair and what it means for the tech. sector in particular and more broadly the fate of trade talks after last weekend’s Trump-Xi bromance, is weighing heavily on technology stocks.

Broader growth concerns (US and, increasingly, concerns over what signs of weaker global growth means for US growth and corporate earnings) are leaving few sectors untouched. Ironically, home builders were one of the least worse performing sectors Friday despite the fact that housing is about the only sector of the economy to show any obvious weakness just at the moment. The impact of lower bond yields on mortgage rates and hence housing affordability is the reason.

Incidentally, the Atlanta Fed’s latest GDPNow estimate, post payrolls, is down to 2.38% from 2.7% and below the current market consensus – though note this is really doing no more than suggest growth is coming back closer to trend after unsustainably strong growth in the last couple of quarters. We should also note that consumer confidence remain increasingly strong, printing an unchanged 97.5 in Friday’s preliminary University of Michigan December reading.

NADAQ has been the worst performing major index globally on the week, off almost 5%. Shanghai and the recently underperforming ASX are the only indices up on the week:

Very mixed FX performance Friday, CAD and NOK the winners on the OPEC+ production news and higher prices, but this not benefiting AUD where risk aversion dominated after the mid-week domestic data-related hit. This also saw NZD weaker. AUD/USD made a low of 0.7198 (versus 0.7192 on Thursday) and ended in NY at 0.7208, NZD at 0.6859.

AUD has restarted the week near 0.7175, so almost half a percent down, following Saturday’s China trade numbers for November. These show both sharply weaker exports and imports (imports 3.1% yr/yr down from 21.4% in October and 14% expected, exports +5.4% y/y from 15.6% and 9.4% expected. Weak imports means the trade surplus blew out to $44.7bn from $34bn in October.

The bilateral balance with the US printed a new record surplus of $35.6bn. So proof positive that numbers prior to November have been heavily distorted by front loading ahead of US tariffs and China’s retaliation to them, while the US numbers tells you that the world’s largest economy has a lot more trouble sourcing alternative supplies from outside China than the world’s second largest economy does from outside the United States.

GBP lost 0.4% ahead of what promises to be a tumultuous week ahead for Brexit developments. On the week, NOK is the clear winner and the AUD the biggest loser (the latter also seeing a two-cent hi/lo range, already extended this morning).

The dollar is overall lower but is still comfortably ensconced inside prevailing ranges, drawing safe haven support as well as from a view that even if the Fed is now close to hitting the pause button on further rates rise, the timing of monetary tightening elsewhere in the world risks being pushed out alongside. Whatever is happening to the US economy at present, it is still far and away the least ugly duckling.

Treasuries yields initially recovered from the immediate post-payroll release slide but then proceeded to leak lower as stocks wilted. 2s and 10s both finished the session 4.6bps lower and pretty much on the lows of the session. Most of the decline in 10s was in real yields, break-evens off only 0.5bps and presumably held up by the bounce in oil on the OPEC news. On the week the 2/10s curve is about 7bps flatter ending at 13.5bps (back from an intra-week low of about 10bps). AU 10s have matched the decline in USTs on the week, while European yields have.

Supporting the bond market rally were comments from Fed Governor Lael Brainard said that the U.S. economic momentum is strong and a gradual approach to interest-rate increases remains appropriate “for now” (significant in so far as of late Brainard has been suggesting that gradual rate rises should continue through 2019.

“The gradual path of increases in the federal funds rate has served us well by giving us time to assess the effects of policy as we have proceeded,’’ Brainard said Friday at a conference at the Peterson Institute for International Economics in Washington. “That approach remains appropriate in the near term, although the policy path increasingly will depend on how the outlook evolves.”

Notwithstanding mounting US and global growth concerns and re-elevated trade worries post the Huawei CFO arrest, the combination of a slightly softer USD and Friday’s OPEC+ agreement to reduce oil production by 1.2mn barrels a day, made for a positive day and week for most commodities, led by oil. The exception though has been base metals, with the LMEX index lower on the day and week. Dr Copper is the worse perming commodity on the week, -1.0% and perhaps the best expression of these global growth concerns:

Germany October industrial production -0.5% (+0.3%E)

US November non-farm payrolls 155k (198kE, 250kP revised from 237k, 2 month net revisions -11k)

US November unemployment 3.7% (3.7%E, 3.7%P)

US November average hourly earnings 0.2% (0.3%E, 0.1%P revised from 0.2%); yr/yr 3.1%, unchanged as expected.

US consumer credit $25.38bn ($15bn E, 11.57bn P)

University of Michigan preliminary December consumer sentiment 97.5 (97.0E, 97.5P)

5-10 year inflation expectations 2.4% down from 2.6%, back to its lowest since December 2016 when it (briefly) 2.3%

Canada November employment 94.1k (10.0k E, 11.12k P) Full/part time split 89.9/4.1k

Canada unemployment 5.6% (5.8%E, 5.8%P)

Canada hourly ages 1.5%y/yr (1.8%E, 1.9%P)

China November trade: exports 5.4% y/y in USD terms (15.6%P 9.4%E)

China November trade: imports 3.1% y/y (21.4%P, 14.0%E).

China November trade balance $ 44.7bn ($34.4bnE, $34.01bnP).

CoreLogic’s weekend auction reports shows a preliminary capital cities clearance rate of 45.3% vs. last week’s final 41.3%, Melbourne cleared a preliminary 46.1% (final 42.7% last weekend) and Sydney 48.1% (41.6% final).

Today starts early with Chris Kent (RBA Assistant Governor, Financial Markets) speaking at a Bloomberg function in Sydney at 08:35 AEDT. 11:30 brings details of October Home Loans.

Offshore, final Japan GDP is at 10:50, expected to be revised to -0.5% from -0.3% on weaker investment data. In the northern hemisphere, we get Italian industrial production (Germany was weak on Friday) UK trade, industrial production and construction output and in US, JOLTS (job openings).

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.