Coming in for landing in a heavy cross wind

Insight

China delivered some more positive results in the last 24 hours.

https://soundcloud.com/user-291029717/chinese-slowdown-what-slowdown

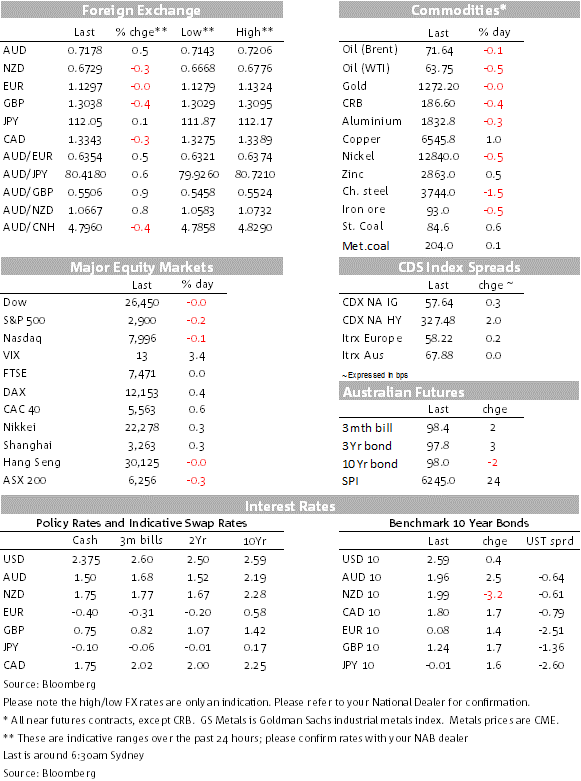

It’s again been a night of measured price action, equities higher in Europe, a mixed report across the US main boards, held back by lagging healthcare stocks amid talk in Washington about expanding Medicare. Across some of the reporting companies, Bank NY Mellon has taken a large hit after their results, Morgan Stanley is higher, as is PepsiCo. US Treasury yields are almost unchanged for the session. Among commodities, WTI is down 0.48%, copper is up 0.94%, while iron ore was down yesterday after the Brazilian authorities gave the green light to Vale to open one of its closed mines after the dam wall failures. Dalian iron ore futures were down 1.6% yesterday. Gold is little changed.

In FX land, it was a night of two parts in the limited price action seen, and certainly as far as the Aussie was concerned. Yesterday’s better than expected Chinese growth numbers – especially the large “overs” in industrial production with industrial production growth up to 8.5% (against 5.6% expected) saw AUD buyers re-emerge, again testing 0.72. But again, it’s failed to push on overnight.

This time it was softened by a better than expected US goods and services trade deficit that came in at $49.4bn against $53.4bn expected and also lower than last month’s $51.1bn shortfall. Notwithstanding support from higher aircraft exports (and some clouds over that), the report also revealed a smaller deficit with China for the opening two months of the year.

As a result of the lower trade deficit, the Atlanta Fed nudged up their estimate of GDPNow to 2.4% from 2.3%, raising their concurrent estimate of the net exports contribution to GDP growth from 0.2% pts to 0.5% pts. The partial offset came from a downgrade to non-residential fixed imports suggested by the US imports data.

The AUD is now been parked back around 0.7175 territory ahead of today’s further instalment on the health of the Australian labour market where NAB looks for better than expected employment, softened by a tick up in the unemployment rate. (See below for more detail on this.)

Other mainboard G10 currencies have been steady to lower against the USD, though the pull-back in Aussie and Kiwi have been the more notable, dips in the other on net marginal at most.

There was a small intra-day exception with some renewed support for the CAD after its March CPI report revealed higher than expected readings on two of its three core measures of inflation, but this move was short-lived and modest, overtaken by renewed support for the USD.

Following yesterday’s lower than expected NZ CPI (with steady to lower core factor model rates), UK core inflation was a tenth lower than expected at 1.8% while EZ core CPI was steady as expected at 0.8%.

Elsewhere, the Fed’s Beige Book described the US economy as performing at a ”slight to moderate” rate of expansion in March and early April. Businesses reported sluggish sales conditions for general retailers and auto dealers (tonight’s US Retail Sales will be pertinent), favourable tourism and also manufacturing, if laced with trade worries.

The US labour market was described as still tight with shortages of skills, but still no generalised wage pressures, while the ability of firms to pass on increased input costs to consumers as mixed. Business reported tariffs, freight costs, and rising wages as factors behind input costs increasing in the “modest-to-moderate” range. Most Districts reported stronger home sales.

The German Government revised down their forecast of German economic growth for this year to just 0.5%, down from 2.1% a year ago, the underperformance ascribed to auto emission standards, trade tensions, and the low level of the Rhine. With the Chinese economy again revealing a pick up, it’ll be interesting to see how this plays out for the export-exposed German economy. Positively, you’d expect.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.