Online retail sales growth slowed in May following a fairly strong April

Insight

Bond yields have risen slightly ahead of Jerome Powell’s talk today - will he give a strong hint a rate cut is coming? And will Philip Lowe from the RBA be doing the same?

https://soundcloud.com/user-291029717/powell-and-lowe-will-they-both-hint-at-rate-cuts-today?in=user-291029717/sets/the-morning-call

I’ve been waiting all night for you to tell me what you want – Rudimenatl

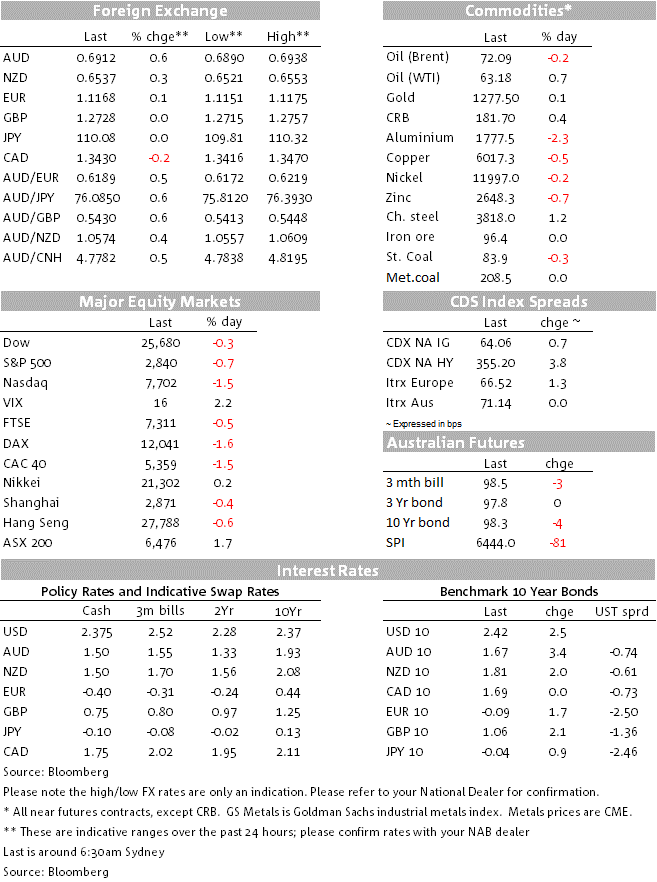

IT shares have led the declines in European and US equities indices following news that Google and other major companies will suspend business and supply to Chinese telecoms as a result of the US decisions to restrict/ban Huawei and ZTE Corp from selling their equipment in the US. China has continued to threatened retaliation, but no news on that front. Currencies have an uneventful night, AUD is the outperformer retaining most of its post-election wins and UST yields are higher ahead of Fed Chair Powell speech this morning.

The equity board is a sea of red with major European and US equity indices opening the new week with hefty declines. IT shares are the big underperformers ( Euro Stoxx 50 sub-index -3.10% while the S&P 500 sub-index is -1.75%) reflecting investors’ concerns over supply chain disruptions following Google, Broadcom, Qualcom, Intel and Xilinx announcements to suspend business or stop supply to Huawei and fellow Chinese telecommunications company ZTE. The decision of course is a consequence of last decision by the US to restrict/ban these Chines telcos from selling their equipment in the US.

Meanwhile, Chinese officials have continued to warn the US that China is now forced to even the score, although we continue to be none the wiser on what that will entail. Overnight China’s envoy to the EU said “Chinese companies’ legitimate rights and interests are being undermined” adding that there would be a “necessary response”. Blomberg also noted that yesterday President Xi Jinping visited a rare-earths facility sparking speculation the materials could be the next pawn move by China given the US relies on China for about 80% of such imports.

Despite the falls in equity markets, global bond yields have ticked up overnight. The 10 year Treasury yield is 2bps higher, to 2.41%, while the 10 year German bund yield is up a similar amount, to -0.09%. Germany will auction a new 10y Bund tomorrow, so a supply story could be at play while the market may also be wary of Fed Chair Powell speech at 9am Sydney time.

As for other Fed speakers, since the FOMC meeting we are now starting to see a bit more divergence in views. Speaking overnight, Atlanta Fed President Bostic signalled a neutral stance saying “if you ask me how the scales are, I don’t feel like for me they are tilted more to the cut than to the hike…I think we are pretty much in balance.’’ Meanwhile, true to his dovish lining, Fed’s Bullard (voter) noted that “with the economy booming the way it is in the US, inflation should be at 2% or even above.” But “We are not seeing that” concluding then “If this (1.6% core inflation) turns out to be persistent, I’ll get more aggressive in pushing the FOMC to lower rate in reaction and try to re-center inflation expectations at 2%”.

So while equities show a risk off tone and core yields start the week higher, movement in currency markets have been more subdued. The USD is little changed in index terms with DXY continuing to find the air vary thin above 98. The AUD is the outperformer (+0.54% and now trading at 0.6908) retaining most of its post-election wins. Yesterday, banks led the gains in the S&P/ASX200, suggesting the market was concerned over the potential impact from Labour policies on capital gains tax in the housing market while changes to franking credit were also a concern. The coalition win has no removed these uncertainties pointing to the prospects of an improvement in business conditions and confidence. As for RBA rate cut expectations, following the election news over the weekend, we have seen a small wind back on pricing for a June rate cut to 70% from 80% while a full pricing of a follow up rate cut has now been pushed out from November to February next year.

RBA events today are going to be the big test for the AUD. This morning we get the May RBA Board minutes and Governor Lowe speaks in Brisbane at 1.10pm Sydney. The Governor’s speech is titled the Economic Outlook and Monetary Policy and our expectations are for the Governor to emphasise the Bank’s easing bias and pave the way for a cut in June. Early in May at its policy meeting, the Bank noted that “a further improvement in the labour market was likely to be needed for inflation to be consistent with the target”. Last week labour force data provided further evidence that the economy is weaker than the RBA had expected. The unemployment rate has risen from an eight-year low of 4.9% in February to 5.2% in April and although employment has remained strong, other measures point to increased spare capacity over recent months suggesting a potential for the unemployment rate to rise further. Thus in our view RBA conditions for a rate cut have now been met.

Central Bank speakers is the theme today with Fed Chair Powell Atlanta speech at 9am ahead RBA Governor Lowe speech at 1.10 pm (all Sydney times) the major highlights

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.