NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

It’s not beyond the realm of possibility that the RBA could cut interest rates today.

https://soundcloud.com/user-291029717/wil-the-rba-cut-rates-today

You said we’re through before, You walked out on me before… You gotta tell me you’re coming back to me – Rolling Stones

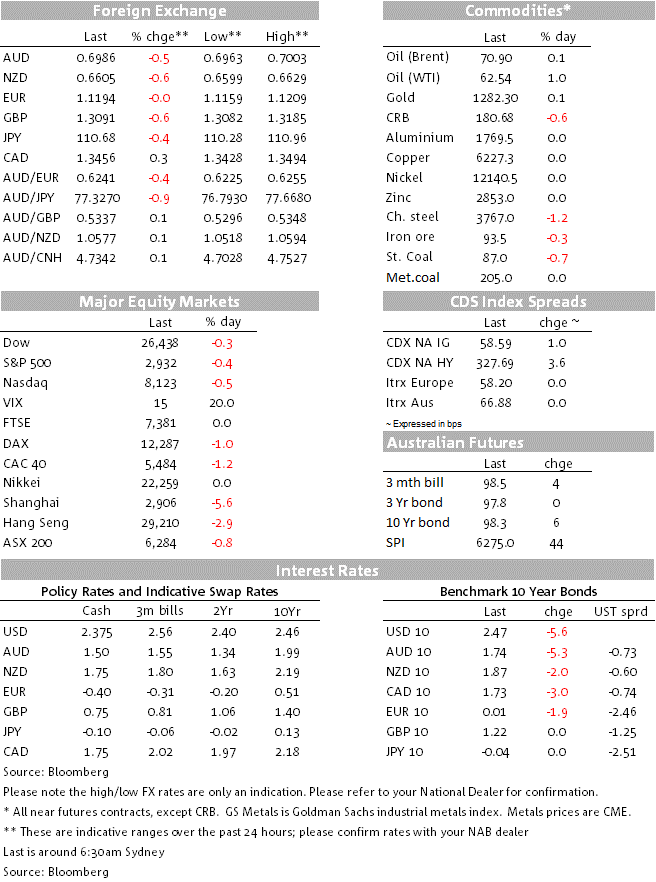

Yesterday’s reaction to President Trump’s tweets threatening to lift China trade tariffs triggered a massive sell-off in Asian equities which continued into the European session, but after sharp drop at the open, US equities have edged their way back up helped along by news reports that China’s trade delegation is still heading to the US. Oil prices have staged a big recovery and UST yields are a few bps lower across the curve. GBP and NZD are the G10 underperformers while AUD is just below 70c ahead of RBA today.

So after a blood bath in Asia with the Shenzhen Composite closing an eye watering -7.38% and the Shanghai Composite -5.58%, the European session opened with a similar risk off tone and it was only after the US open that equities began to recover. After speculation China trade delegation was going to cancel its US visit during the Asia session, China’s foreign ministry confirmed officials were still planning to travel to the US this week for the next round of talks. Importantly, however, during the overnight session it was unclear whether Chief negotiator Vice Premier Vice Premier Liu, will get on the plane. The S&P 500 closed -0.45% and the NASDAQ was 0.5% lower, both recovering smartly from an initial drop of just over 1.5%.

As suggested in our daily yesterday Bloomberg reported overnight that Trump’s tweets were instigated by China’s attempt to renegotiate agreed component of the trade deal. According to the report China back tracked on its agreement to make changes to laws aimed at ending the enforcement of US companies seeking to do business in the country to reveal proprietary technologies and other intellectual property.

Speaking to the media a few minutes ago, US Trade Representative Robert Lighthizer confirmed China’s delegation will visit Washington as planned and that Vice Premier Liu is expected to be part of the delegation. In the same media briefing US Secretary Steve Mnuchin said that the US isn’t willing to re-negotiate previous commitments and Lighthzer added that the US will look to increase China tariffs on Friday…unless of course China agrees to make those law changes.

Initial reaction to this breaking news has been somewhat mixed. UST yields have gapped lower (10y UST now at 2.469%), NZD is a few bps higher (0.6613) and AUD is a few bps lower (0.6991). The fact that Vice Premier Liu is heading to Washington is positive, but if China doesn’t agree to the alluded law changes above, the US will go ahead with lifting tariffs on Friday. Either way the end of the week look set to be a volatile one for risk assets.

Back to the overnight price action, commodity prices were generally weaker, although oil prices have staged a strong comeback. Brent crude plunged below $69 a barrel, down over 3%, but has recovered strongly to be up 0.8% for the session to $71.05, after reports that the US has dispatched an aircraft carrier strike group and bomber force to the Middle East.

GBP is on the soft side as the market reins in some optimism that the Conservatives and Labour will do a Brexit deal. PM May is directing new clauses to be written into the Withdrawal Agreement Bill that would provide for a customs union-style arrangement, as preferred by Labour. John McDonnell, Labour’s Treasury spokesman, poured cold water on the idea that the talks are close to success, suggest Sunday that May’s leaks of confidential talks were in “bad faith” and that he didn’t trust her. GBP is edging downwards and is currently down 0.6% for the day and now trades just under the 1.31 mark.

European data printed mostly on the positive side, but mixed currents have kept the Euro essentially unchanged at 1.12. EZ March Retail Sales beat expectations at +1.9%yoy vs 1.8% exp., EZ May Sentiment index +5.3% ( 1.2 exp. and -0.3 prev.) along with a series of final Service PMIs printing mostly a little higher than their flash estimates.

The CAD staged a decent recovery overnight after trading to a session high of 1.3494 ( now at 1.3448) following comments from BoC Governor Poloz noting that housing remains solid and growth should return to the sector later this year. The move higher in oil prices probably didn’t hurt either.

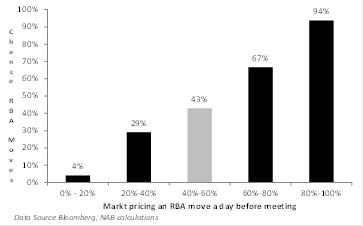

Based on yesterday’s closing IB (30 days Inter Bank cash rate futures) levels, the market is pricing a 45% chance that the RBA will cut the cash rate today by 25bps to 1.25%, but working out what the historical probabilities tell us about today’s decision is highly sensitive to how one asks the question. Looking back at history (since Aug 2003) if pricing for a move is below 50% then there is a very low probability (7%) the RBA will go today. But asked differently if pricing expectations are between 40% and 60% then the probability of an RBA cut surges to 43%. What about the AUD/USD? If pricing for a rate cut is below 50% and the RBA cuts then the probability the AUD/USD ends the day lower is 100%, but if the RBA doesn’t cut then there is around a 50% chance the AUD/USD ends the day lower. In the latter case , what the RBA says will matter too i.e if the Bank doesn’t cut but introduces an explicit easing bias, then the AUD is likely to end the day lower – assuming no major external factors such as a positive US-China trade news.

NAB’s view is that the RBA will cut rates over the next few months, but we narrowly favour rates remaining on hold this month with the Bank adopting a clear easing bias instead. The May interest rate decision will discuss the RBA’s revised outlook, which will be detailed in the Statement on Monetary Policy on Friday. The risk of a May cut stems from weak inflation data and on Friday’s Statement on Monetary Policy we expect the RBA to downgrade its forecasts for growth, inflation and, to a lesser extent, unemployment.

CH: Caixin PMI services, Apr: 54.5 vs. 54.4 prev

We expect soft AU retail sales print today, lifting only 0.1% in March (mkt: 0.2% m/m) after last month’s strong 0.8% gain. A pull-back in department store sales after strong growth in February, plus some decline in food sales due to lower fruit and vegetable prices, is expected to drag on total sales.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.