NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Many believe the RBA didn’t go far enough on Monday, buying up a $1 billion of bond purchases in the face of sharply rising bond yields.

https://soundcloud.com/user-291029717/will-the-rba-play-catch-up?in=user-291029717/sets/the-morning-call

“Just a man and his will to survive; So many times it happens too fast; You change your passion for glory; Don’t lose your grip on the dreams of the past; You must fight just to keep them alive”, Survivor 1982

Central banks are taking a mixed view of the rise in yields with the Fed’s Powell overnight tacitly endorsing market moves, while it seems the RBA is preparing to come out swinging to defend the 3yr target and reinforce guidance of rates being on hold until at least 2024 (see AFR article ). One wonders if RBA Governor Lowe has Rocky Balboa in mind as he eats his cornflakes this morning and how much of the April 2024 bond he is willing to own (more on that below). As for the Fed, Chair Powell noted the run up in yields was “a statement of confidence” in the outlook, echoing the remarks by his colleague Kaplan on Monday of “would not be surprised if Treasury yields rise as growth outlook improves.

Looking at market reaction, Chair Powell has managed to tread that fine line of endorsing market moves, but not adding to them by re-iterating his dovish stance. Powell’s prepared remarks noted that noted “the economy is a long way from our employment and inflation goals, and it is likely to take some time for substantial further progress to be achieved”. QE will continue at its current pace “until substantial further progress has been made toward our goals ”. Concerns around inflation were also tempered with Powell noting that “for some of the sectors that have been most adversely affected by the pandemic, prices remain particularly soft”. (see Semiannual Monetary Policy Report to the Congress). In the Q&A he gave the tacit endorsement to the move in yields (“In a way, it’s a statement on confidence on the part of markets that we will have a robust and ultimately complete recovery”).

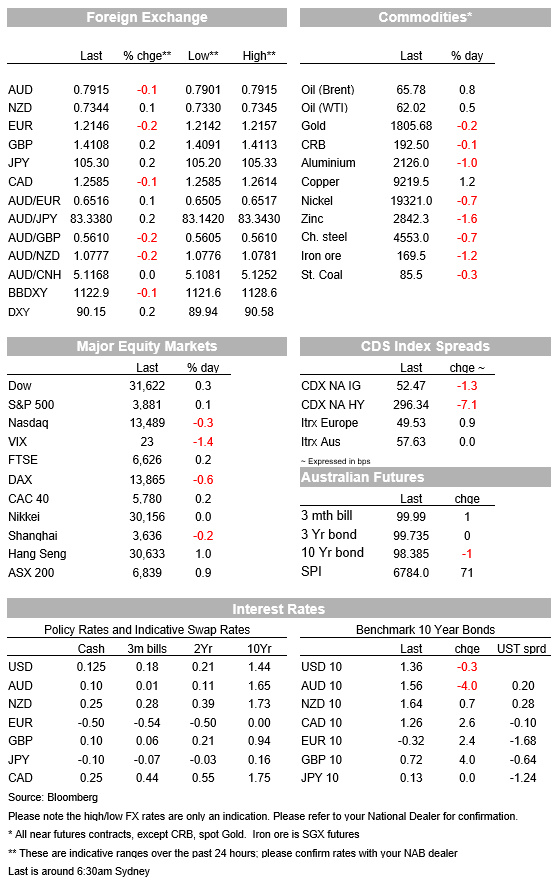

Yields accordingly mostly consolidated their recent moves with the US 10yr -0.5bps to 1.36%.

Equities are paring losses into the final hours of trade, with the S&P500 eking into the green +0.1% with a clear tilt in sector performance towards financials (+0.5%) and energy (+1.8%). Interestingly small caps are underperforming with the Russell 2000 -1.0%.

FX has been fairly muted in response with the USD DXY +0.2% with EUR -0.2%. GBP continues to outperform, +0.2% to 1.4108. The AUD is little changed at -0.1% to 0.7911, while commodity prices remain supportive to a move above 0.80 and beyond as our FX strategists forecast – note copper overnight was up 1.2%

Focus has started to return to the US $1.9 trillion stimulus package with a vote in the House expected by the end of the week. Budget reconciliation looks like the only way to pass with centrist Republican Senator Susan Collins not expecting a single Republican vote for the stimulus package.

There was little in the way of other data overnight. The US Conference Board Consumer Confidence Index was broadly expected at 91.3 v 90.0 expected. UK unemployment was also as expected at 5.1%, though with larger than expected falls in employment (-114k v. -30k expected).

Finally, the Australian government’s majority in the lower house has been reduced following the resignation of one member (Craig Kelly). The government now has 76 MPs out of 151, but after supplying the speaker has just 75 votes. The AFR reports the government has signed an agreement with a crossbench MP (Bob Katter). Reduced government numbers increases the chances of an election occurring in 2021.

All focus on central banks and the recent moves in yields. Domestically the AFR’s Kehoe writes the RBA is set to come out swinging today in QE, while across the Ditch the RBNZ meets. There is also plenty of central bank talk, including from BoE Governor Bailey and the Fed’s Powell, Clarida and Brainard. Details below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.