Online retail sales growth slowed in May following a fairly strong April

Insight

Negativity on the state of the global economy has managed to overshadow positive earning results from US companies.

https://soundcloud.com/user-291029717/speculation-determinism-and-pessimism

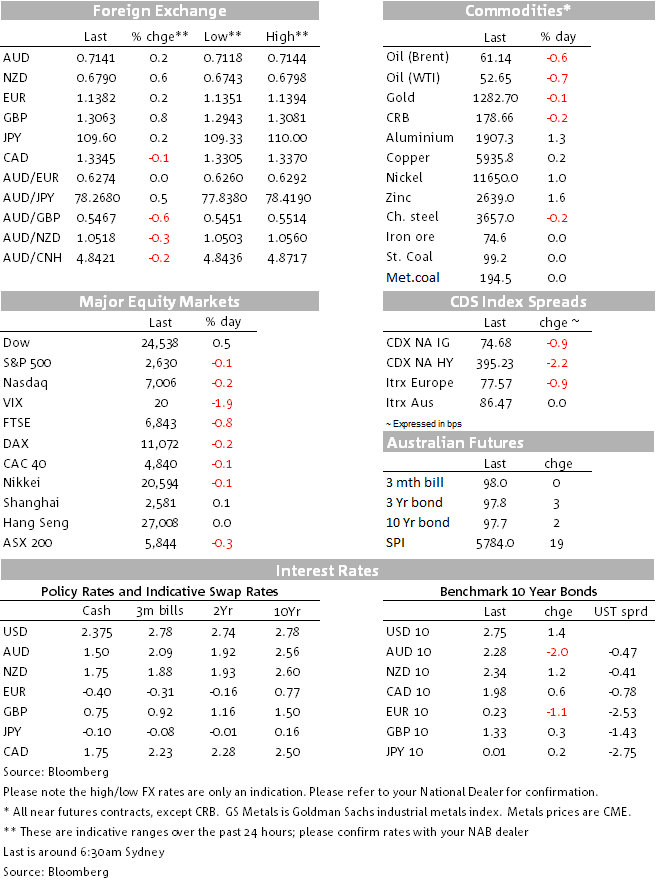

The US dollar is weaker (and AUD a little stronger) from where we left off yesterday, thanks largely to gains for GBP and which has dragged EUR along for at least part of the ride. US stocks have tuned negative having earlier been buoyed by positive earnings results from the likes of IBM and Procter & Gamble (Ford and Texas Instruments report shortly). US bond yields are little moved. A big day ahead with local labour market data and French, German and pan Eurozone PMIs tonight followed by the ECB. Will Mr. Draghi change his tune?

As for the ongoing government shutdown, President Trump and newly installed House leader Nancy Pelosi may not have spoken for well over a week now, but there are reports that the Democrat side may be moving towards a proposal that would offer $5.7bn worth of funding for border security (if not $5.9bn worth of explicit ‘wall’ funding, in which case the prospects for an end to the government shutdown in the coming week or two might not be completely hopeless. In the meantime the chair of the President’s Council of Economic Advisers, Kevin Hassett, has been out warning that Q1 GDP could be zero if the shutdown doesn’t end soon, but talks of a ‘humongous’ rebound as and when it does.

FX markets becoming more convinced that the ‘worse’ that might happen on Brexit is that Theresa May’s previously doomed Withdrawal Agreement might actually get overt the line if the ‘hard Brexiteers’ in her government become convinced that the alternative is an extension of the Article 50 timeline, a second referendum and potentially no Brexit. GBP/USD is up 0.9% on this time yesterday (AUD/GBP -0.35%) and the best performing G10 currency.

A stronger pound has meant that EUR/USD is up, but by only 0.25%, maintaining its status as a ‘low beta’ GBP. Whether these gains can survive the EZ PMI data and ECB tonight of course remains to be seen.

GBP gains are followed by the NZD, after yesterday’s Q4 CPI numbers showed an acceleration in annual inflation rates on most core measures and a particularly large jump in the ‘non tradeables’ component that represents domestically generated inflation. This saw the market-implied odds of the RBNZ cutting rates this year significantly reduced – albeit not eliminated. The data is also seen to have reduced the risk of a downside surprises in next week’s equivalent Australian data (where NAB is at 0.3% on the headline print). This in turn may be one reason, along with overall US dollar weakness, why AUD is about 0.2% up on this time yesterday.

JPY is slightly weaker and where BoJ’s Governor Kuroda was arguing last night that there are still plenty of unconventional policy measures the bank could deploy to achieve its inflation target. Markets aren’t convinced though and despite the BoJ’s inflation forecast downgrades yesterday, the JPY is stronger than where it sat prior to yesterday’s (unchanged) BoJ meeting outcome.

The CAD is the other underperformer, follow weaker than expected retail sales numbers (-0.9% headline, -0.6% ex-autos) with household goods spending particularly weak. The latter chimes with a subsequent Bloomberg TV interview with BoC Governor Stephen Poloz in Davos in which he highlighted the current weakness of the housing market. While still saying higher rates will be needed in so far as policy is seen to be well below ‘neutral’, he revealed himself to be in no hurry whatsoever to contemplate the next move up in the 1.75% o/n lending rate.

With an hour of trading to go, US equity indices are mixed – Dow up 0.6%, NASDAQ down 0.2% and the S&P little changed. Gains earlier in the session followed good earnings reports from IBM, United Technologies and Procter & Gamble, but looking at the S&P sub-sectors, Energy and Materials are both off more than 1% and in which respect we’d note than oil prices turned lower as the US session progressed.

Texas Instruments and Ford both report soon after the 8:00 AEDT NYSE close. Ford downgraded its 2018 earnings guidance last week recall and its stock fell by about 5%, so this presumably will cushion any further fall-out from a poor earnings report today?

Not much to say about bonds. 10-year Treasury yields were as high as 2.78% earlier in the New York session but have slipped to 2.735% as stocks turned over (2.75% now). The 2-year yield is currently at 2.59%, where we left it yesterday evening.

WTI and Brent crudes are both currently off about 35 vents or 0.6%, precious metals are narrowly mixed (gold down $2) but base metals are all higher led by a 1.4% rise in aluminium (copper up a lesser 0.3%). Iron ore futures and both coals are unchanged.

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.