We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Janet Yellen shrugged off concerns about the Biden stimulus package unleashing inflation on the US economy.

https://soundcloud.com/user-291029717/yellen-denies-great-inflation-expectations?in=user-291029717/sets/the-morning-call

“Give me everything tonight; For all we know, we might not get tomorrow; Let’s do it tonight; Don’t care what they say; Or the games they play; Nothing is enough”, Pitbull, Ne-Yo, Afrojack and Nayer 2011

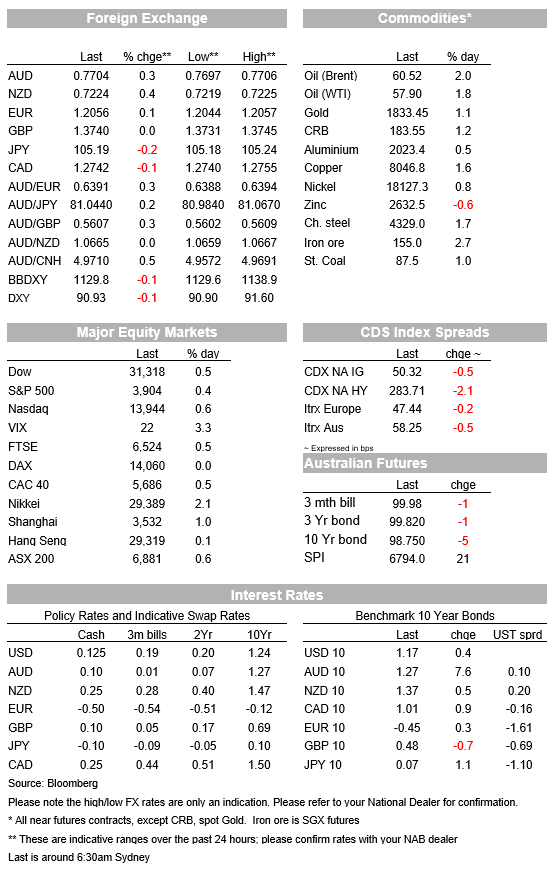

Reflation on the back of US fiscal stimulus and positive vaccine news remains the major theme for markets. Treasury Secretary Yellen on Sunday night said if the $1.9 trillion stimulus plan is approved, the US could be back to full employment by the end of 2022 instead of 2025 (see full CNN interview here ). Yellen played down inflation concerns that have been aired by a number of economists and overnight the Fed’s Barkin was the first official Fed member to push back on such concerns – note Chair Powell speaks on Wednesday (see FT link here ). There was little other news or data overnight. The S&P500 is up 0.4%, while the small cap Russell 2000 is up 1.8%. Yields consolidated moves after hitting an overnight high of 1.1981%, currently 1.16%. The retracement in the ultra-long end has been greater with the 30yr yield briefly breaching 2%, now down 6bps to 1.94%. The USD DXY was little moved (DXY -0.1%), while commodity currencies outperformed with the AUD +0.4% to 0.7001.

US fiscal stimulus news was not new overnight, but reinforced the US Administration to push forward with the $1.9 trillion package despite recent criticism of the size of the package by a number of high-profile economists including Summers. Treasury Secretary Yellen emphasised that if the package is approved the US could return to full employment by 2022 and that without additional stimulus, it could take until 2025 to see unemployment back below 4% based on CBO projections. The Fed’s Barkin also pushed back on suggestions that the stimulus could see an outbreak of inflation, noting that strong disinflationary forces such as globalisation and technology will keep prices subdued, while short-term price increases would only become inflationary if businesses were unable to increase production – unlikely given services sectors should rebound once re-opening begins. Signs are start to emerge of re-opening with New York City restaurants being allowed to reopen indoor dining at 25% capacity from February 12.

In FX only mostly moderate moves were seen given the lack of news flow or data. The USD (DXY) was down -0.1% with GBP (0.0%) and EUR (+0.1%) little changed. Commodity currencies outperformed with AUD +0.5% and NZD +0.4%.

Vaccine news was positive with the US CDC reporting that 10% of the US population has now received at least one vaccine dose – or more than 32m people. While the AstraZeneca vaccine appears to have some efficacy issues with the South African virus strain, other vaccine types appear to be effective including the J&J and the Pfizer/BioNTech vaccine.

Former ECB President Draghi is poised to become PM after two formerly anti-euro parties (The League and Five Star) signalled they would be willing to support him in a national unity government. Italian bonds continue to rally with the 10yr BTP yield -2.6bps to 0.51%. German 10yr yields were little changed (-0.3bps) at -0.45%.

Bitcoin hit a high of $44,795 overnight (currently trading at 43,113, +14% overnight) after news of Tesla saying it has purchased $1.5bn worth of bitcoin and expects to begin accepting payment in crypto for its products. Elon Musk seems to have an affinity for crypto currencies after having recently tweeted about Dogecoin. There are also signs of retail money flowing into crypto with a Reddit group called SatoshiStreetBets (similar to WallStreetBets).

WA’s budget surplus is nearly $1bn more than expected at $3.1bn. The boost came from iron ore with revenue projections revised higher by $2.3bn. WA heads to the polls on March 13.

Domestic focus on the NAB Business Survey in what is a quiet day for data. Offshore there will likely be passing interest in NZ’s inflation expectations, while China’s Aggregate Financing Figures are due any day from today. Details below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.