Online retail sales growth slowed in May following a fairly strong April

Insight

Bonds yields rose sharply again on Friday, with 10 year Treasuries reaching their highest level since February last year.

https://soundcloud.com/user-291029717/yields-higher-jabs-faster-inflation-expectations-lower?in=user-291029717/sets/the-morning-call

“D-J got us fallin’ in love again; Keep downing drinks like there’s; No tomorrow there’s just right; Now, now, now, now, now, now; Gonna set the roof on fire”, Usher feat Pitbull 2010

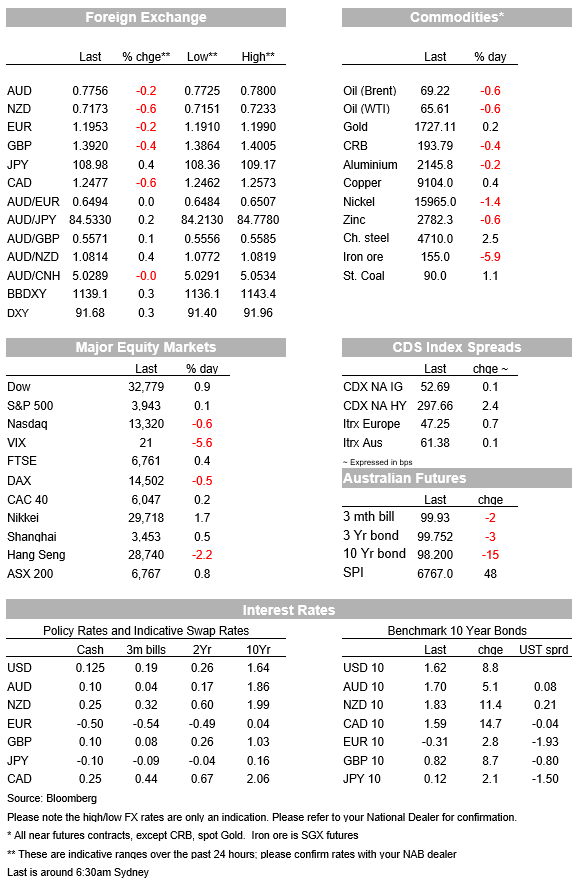

The bond market sold off sharply on Friday on no real news (technicals one driver) apart from the glow of the $1.9 trillion stimulus package being formally inked on Thursday and an acceleration in the US vaccine timeline. The US 10-year Treasury yield rose 8.8bps to 1.62% (intraday high 1.64%) and is at its highest level since February 2020. While the implied inflation breakeven initially rose (intra-day high of 2.30% and now 2.2765%), it was real yields which saw the greatest move with the 10yr TIP yield +10bps to -0.65%. The curve steepened with 2/10s +8bps to 147bps and the steepest in 5 ½ years. Australian bonds underperformed with the 10yr futures moving 11bps vs. the 8bps move in US 10s on Friday’s Sydney close.

Equities brushed off the rise in yields, instead continuing the cyclical rotation theme (NASDAQ -0.6%, but Russell 200 +0.6% and Dow +0.9%) with a better than expected Uni Michigan Consumer Sentiment print adding (83.0 v 78.5 expected). Over the week the smaller cap Russell 2000 is up 7.3%, outperforming the NASDAQ which is up 3.1%. Within the consumer sentiment index, inflation expectations were flat to lower – 1yr expectations 3.1% from 3.3% and 5-10yr unchanged at 2.7% – which was one catalyst for the reversal in the move in inflation breakevens early in the session.

The other positive driver for sentiment was President Biden flagging an acceleration of the vaccine rollout on Thursday evening. Biden is now saying by May all adults who want a vaccine will be able to get one. The latest CDC data show 14.5% of the population is now fully vaccinated and 27% have received at least one dose. The vaccination rates of those most vulnerable are higher with 35.0% of 65years+ having been fully vaccinated and 63.4% having received at least one dose.

Across the pond the vaccine rollout is progressing less quickly (apart from the UK). New virus cases are trending higher in Germany with the public health agency warning a third wave has already begun. Italy is imposing a near-national lockdown from Monday to the Easter weekend in an effort to curb the spread of the virus (shops will be closed, along with bars and restaurants). A delay to the EU’s rollout of vaccines could mean social distancing restrictions staying in place than for countries such as the US, UK and Israel. Nevertheless, such a delay is likely to be a matter of months given it is about vaccine supply, rather than several quarters with markets still able to price the other side of the pandemic given high vaccine efficacy. On vaccine supply, BioNTech is partnering with manufacturers to ramp up production, while a number of EU countries are reviewing the Astrazeneca vaccine (Ireland the latest).

In FX, the USD rebounded with higher yields supporting. The DXY rose 0.3% with the USD up against all G10 apart from CAD. The CAD was the star performer on Friday on the back of the exceptionally strong Canadian jobs figures. Employment growth was +259k v. 75k expected. Unemployment rate dropping from 9.4% to 8.2%. Canada’s 10-year bond yield increased 15bps on the day, with the market now pricing a better than even chance the Bank of Canada will raise its cash rate by March next year.

The EUR, which had been sitting just below 1.20 on Friday morning, fell 0.3% to around 1.1950. News that Italy was going to return to lockdown, amidst a resurgence in Covid-19 cases in the country, didn’t help sentiment towards the EUR. Elsewhere, the JPY fell 0.5%, with USD/JPY closing at its highest level since June, while GBP was down -0.3% with better than expected monthly GDP figures not helping (Jan GDP -2.9 vs. -4.9 expected).

The NZD underperformed on Friday, for no clearly identifiable reason, while the AUD largely tracked USD moves.

A big week this week domestically with Australian Employment on Thursday and Retail Sales on Friday. On employment NAB sees upside risks to the consensus based on very positive labour demand indictors. NAB expects 50k jobs in February (consensus 30k) and for the unemployment rate to fall two tenths to 6.2% from 6.4% (consensus 6.3%). Should employment print at 50k then employment would be just 0.1% below pre-pandemic levels (or just 14k jobs). There are also a few RBA pieces with the March Board Minutes on Tuesday as well as opening remarks from Governor Lowe at a conference today. Given Governor Lowe’s extensive speech last Wednesday where he pushed back against market pricing and emphasised the pursuit of maximum possible employment, we do not expect any new insights.

Offshore it is also a big week with the focal points being the trio of central bank meetings, FOMC, BoE and BoJ. There are also key data pieces including, NZ Q4 GDP, Chinese Activity Indicators, US Retail Sales, and the virus track in Europe with another wave evident and Italy going into lockdown for Easter:

The FOMC meeting will be the key focal point. While rates and guidance are expected to be unchanged, focus will be on the refreshed forecasts given the fiscal package and Treasury Secretary Yellen’s observation that full employment could be reached by mid-2022. Powell is also likely to be pressed on the recent rise in bond yields and whether the Fed would respond. Financial conditions still remain easy so it is likely he will maintain his line a few weeks ago. There will also be interest on whether the Fed extends the exemption of Treasuries and reserves from calculations of the Supplementary Leverage Ratio (this allowed banks to have more flexibility to use their balance sheet for activities such as lending). 65% of participants expecting a temporary exemption. An issue given the amount of Treasury supply hitting the market. That same survey also expects the first signals towards a QE taper to occur in the September 2021 meeting with the tapering to occur in Q1 2022 and all purchases to cease in H1 2023. That expectation is also important for Australia where the RBA appears committed to shadowing the moves by the Fed to ward of exchange rate appreciation pressures.

A very quiet start to the week domestically with most focus on Chinese activity indicators were base effects are likely to see some eye popping numbers data. Details below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.