Online retail sales growth slowed in May following a fairly strong April

Insight

After a year of credit spread tightening, investors are becoming more cautious and selective.

The current year has proved a challenging period for global corporate credit markets as a near continuous period of credit spread tightening that began in early 2016 came to an end. The end of the credit rally was precipitated by the same events that drove volatility in equity markets over the same period, namely the ‘tapertantrum’/rising bond yields of January and February, repeated again in September, overlain by rising Chinese-US trade tensions, European (specifically Italian and Brexit) concerns and Middle East political strains.

For credit markets specifically, the year has seen a relatively steady episode of widening spreads and in the process, have largely ignored several US (and to a lesser extent European) major equity market rallies. For the most part though, the spread widening has been orderly and continues to be seen as an appropriate reassessment of what had become overly tight credit spreads rather than a reflection of any material deterioration of credit fundamentals.

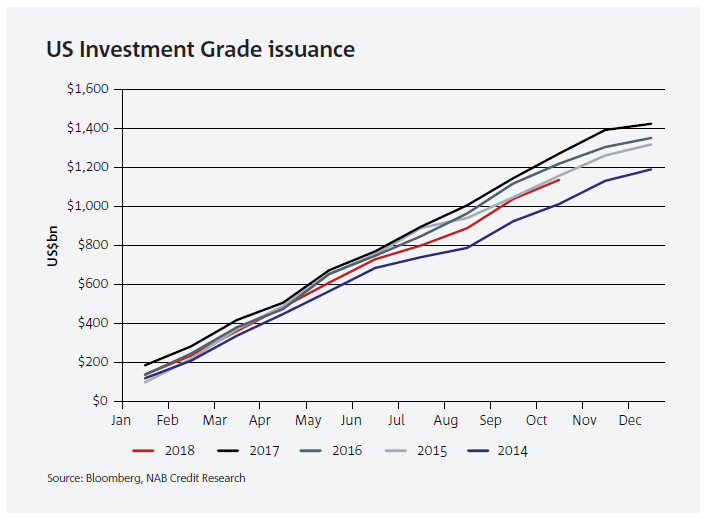

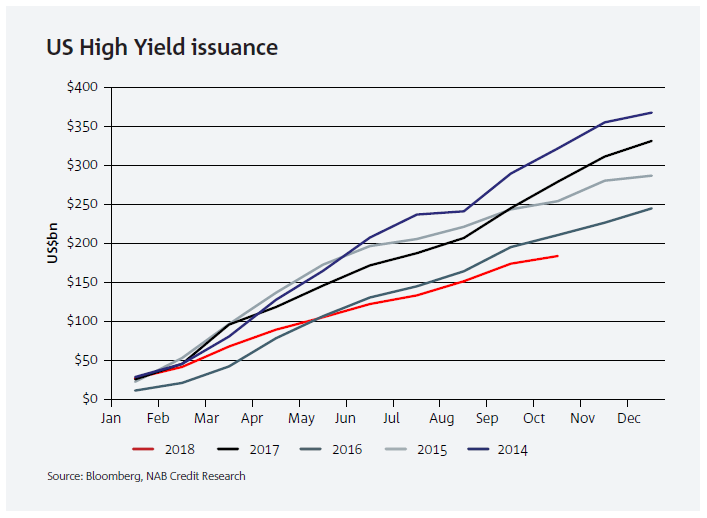

The volume of corporate bond issuance is also another measure partly reflective of investors’ risk appetite. As with corporate bond spreads, the primary bond market has also displayed a shift, moving from a pervasive mood of complacency — as indicated by heavy issuance volumes, thin (at times even negative) new issue concessions and light covenant protection — to now, an increasing degree of investor caution, discipline and selectiveness.

That has been most evident in the US High Yield (sub investment grade) market where issuance volumes are down 34% from the same period last year.

US and European IG issuance volumes are also short of last year’s volumes, but not nearly to the same degree as for the US High Yield market and are still within 5-year ranges.

What is also clear is that new deals will still attract sufficient investor interest, providing they are priced appropriately. There’s certainly no suggestion currently of any ‘capital strike’ to the degree seen during the three most recent market dislocation events of the GFC, the European debt crisis/US sovereign downgrade or the China currency devaluation events.

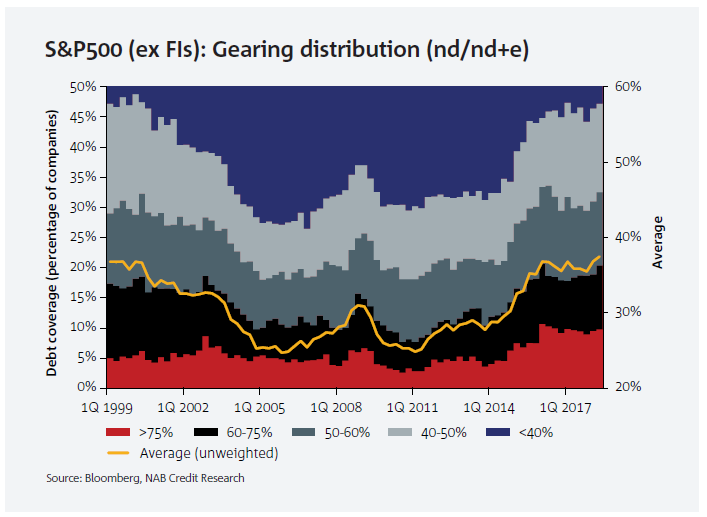

While the risk reassessment is generally attributed to broader macro-economic concerns over rising bond yields and Chinese-US trade tensions, there are also some more specific and fundamental corporate credit quality concerns that have been building for several years.

Australian corporate credit quality appears to be at cyclically strong levels (as evidenced, amongst many other measures, by very low current loan arrears and defaults) and European credit also appears to be on a recovering trend (albeit with plenty of bumps along the way). However, some indicators do point towards growing stress across corporate America. That principally reflects growing leverage, with many companies pursuing debt-funded shareholder distributions and M&A policies. For now, bank loan liquidity remains very high — the US Senior Loan Officer Opinion Survey for example is approaching its easiest level of the cycle range. But should liquidity tighten, stresses in time will progress to rising defaults.

Despite the concerns posed by rising US corporate leverage, liquidity in the US is likely to remain supported by expectations for reasonably solid US corporate profit growth (notwithstanding that will decline materially from the current high levels once the effects of the US tax cuts roll off from 1Q 2019).

For corporate credit spreads globally that means the outlook remains relatively supportive. Investors are unlikely to quickly return to the environment of deep complacency evident up until early this year and credit spreads are unlikely to return to the levels of that period. While Australian credit spreads could likewise remain under some gentle widening pressure, domestic issuers are robustly placed from a fundamental credit quality perspective.

Declines in Australian housing prices are probably the single largest risk in the minds of offshore investors and will likely be the key point of interest in the year ahead. House prices in Sydney and Melbourne have declined approximately 8% and 5% (respectively) from their late 2017 peaks. However, non-performing mortgage loans (90 days plus or impaired), while having increased somewhat over the past three years, remain very low by international standards (currently approximately 0.7% for the Australian Big 4 banks), while actual losses remain at very low levels.

Further, the strong house price rises registered over the past decade have now seen most loans with a low dynamic LVR (average is under 50%), and the credit quality of more recent loans has been strengthened by more stringent controls. As such, actual losses incurred by the Big 4 banks on their mortgage books remains extremely low. Likewise, the high level of broader corporate credit quality referred to earlier is reflected in corporate non- performing loans declining to extremely low levels, under 0.7% of exposures.

That strong asset quality positioning, together with an ‘undeniably strong’ capital position as mandated by the bank regulator, continues to see the Big 4 banks placed amongst the highest rated globally. Additionally, clarity now emerging on the bank regulator’s proposed TLAC policy is very likely to see that strong credit rating position maintained, as well as provide pricing support for senior unsecured bonds. Term bond issuance from the Big 4 banks (across all seniorities) is expected to increase in 2019 due to materially higher maturities, though under the bank regulators’ capital recommendations, T2 subordinated bond issuance may increase somewhat, at the expense of senior unsecured debt. Investors’ search for diversity outside of the banking sector combined with low issuance for an extended period of time has provided solid support for Australian non-FI corporate spreads. The solid credit fundamentals supporting many in the sector, together with low maturities in 2019 (and thus low refinancing requirements) is likely to see that dynamic continue.

This article was first published in 2019 Outlook Creating Opportunities. Read more articles from the magazine.

Speak to a specialist

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.