Online retail sales growth slowed in May following a fairly strong April

Insight

The NAB Quarterly Business Survey provides valuable insight into Australian business, and offers a more in-depth probe into the conditions facing Australian business than the monthly survey, and also provides extra information about how firms perceive the outlook for their respective industries.

Australia’s non-mining recovery remains on track according to the June quarter NAB Business Survey.

Leading indicators also suggest the outlook remains positive, although momentum has eased a little. Despite that, firms are continuing to suggest quite strong investment intentions for the next 12 months, consistent with the steady rise in capacity utilisation rates, while near-term employment intentions improved and longer-term employment intentions remained relatively solid. Inflation measures in the Survey remained subdued, which may point to another soft CPI outcome for Q2, while inflation expectations for the next 3 months point to a continuation of this trend.

The NAB Quarterly Business Survey provides valuable insight into Australian business, and offers a more in-depth probe into the conditions facing Australian business than the monthly survey, and also provides extra information about how firms perceive the outlook for their respective industries.

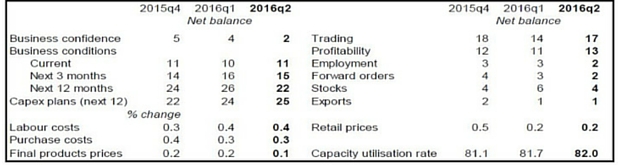

Business conditions improved a little further in the June quarter, rising 1 point to +11 index points, which is well above the long-run average – largely supported by very high trading conditions and profits. According to NAB Group Chief Economist Alan Oster, “firms were still reporting business conditions consistent with an ongoing recovery in the non-mining sector”. “There was a slight moderation in business confidence, but given the build-up of economic and political uncertainties since the start of the year, this is still a good result”, said Mr Oster. “Additionally, the Monthly NAB Business Survey actually suggested business confidence lifted towards the end of the quarter.”

While these outcomes do not differ hugely from the monthly Survey, new information in this survey relates to how firms perceive the outlook facing their business and the economy. According to Mr Oster, “firms are still quite upbeat about the outlook, albeit not as much as they were last quarter. Firms’ expectations for business conditions in 3 and 12 months’ time were pared back a little, but are still quite positive. Optimism about the outlook should bode well for the labour market and business investment going forward.”

Other leading indicators were again quite good, although some appear to have lost momentum. An increase in capacity utilisation could have a positive effect on firms’ investment and employment decision (at least for non-mining sectors). Indeed, capex plans for the next 12 months strengthened, while near-term employment intentions improved and longer-term employment intentions remained relatively solid. However, firms are still suggesting that the availability of labour is not a major constraint on output at the moment, consistent with subdued labour cost measures. Firms however continue to report that weak customer demand is the main constraint on increasing employment.

There remain tentative signs that the non-mining recovery is becoming broader based, with the spread between conditions in the best and worse industries narrowing over the past 12 months. “This is important because we are likely to see impetus from areas such as housing construction start to wane in the medium-term”, said Mr Oster. However, the June monthly survey did suggest that retail conditions have started to weaken – consistent with reports of soft retail orders and margins in this survey. Business conditions reported by residential construction firms are starting to moderate, while confidence is looking soft. The survey takes a closer look at construction, as well as personal services firms, given their importance to the non-mining recovery.

The Survey is also continuing to show very moderate inflation pressures, which is also working to keep wage pressures contained. Firms expect both their own prices and labour cost growth to ease a little further in the coming quarter. According to Mr Oster, “the outlook for business activity in this Survey should make the RBA reasonably comfortable, but the inflation picture raises the possibility of an August cut”.

For full analysis, download report:

More from NAB:

Online retail sales growth slowed in May following a fairly strong April

Insight

Sally Auld, NAB Group Chief Economist, shares her insights on the economy

Webinar

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.