This week we expand on the hot inflation reads seen in the NAB Business Survey and what this may mean for CPI pressures in Australia, particularly for Q3.

Analysis: Hot inflation in the NAB Business Survey, what does this mean for CPI

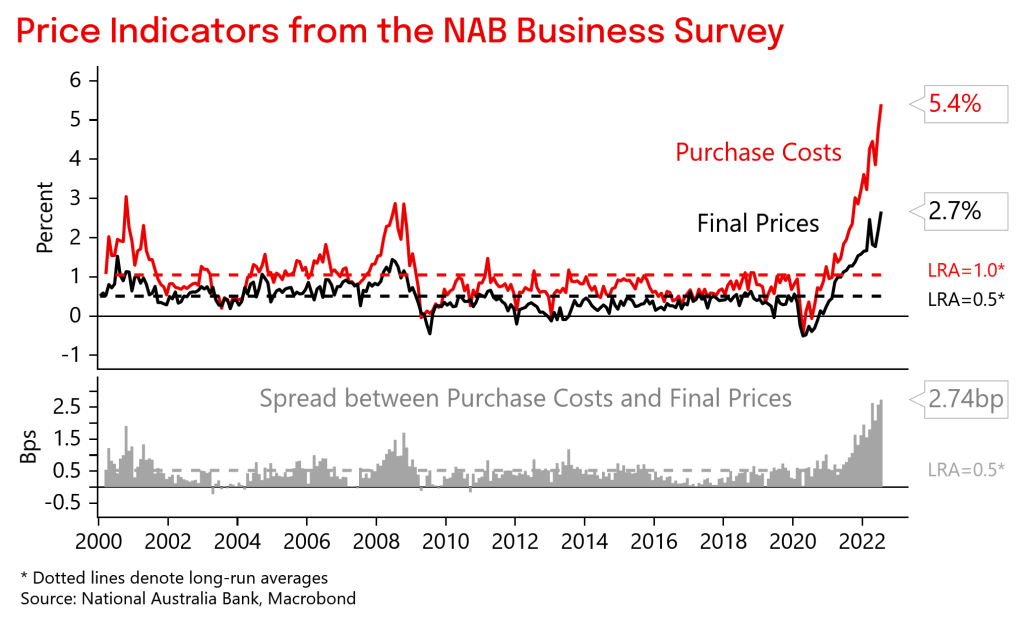

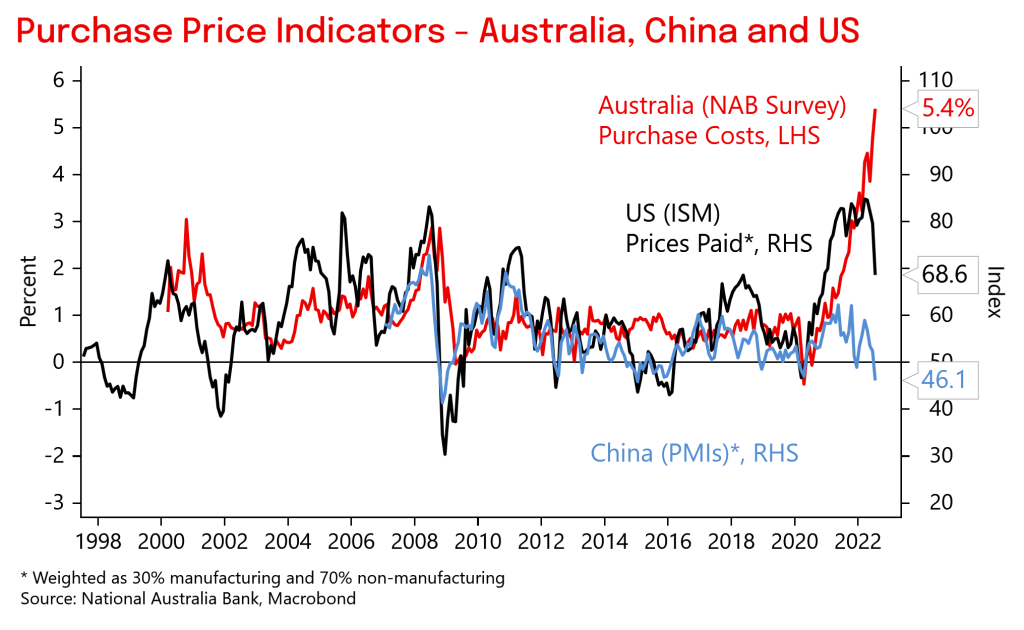

This week we expand on the hot inflation reads seen in the NAB Business Survey and what this may mean for CPI pressures in Australia, particularly for Q3. The July Business Survey reported purchase costs and final product prices at record highs with purchase costs growing at 5.4% quarterly, and product prices at 2.7%. Since early 2021 these cost indexes have run above their long-run averages of 1.0% and 0.5% respectively. In this note we delve into the industry trends and map this across to CPI.

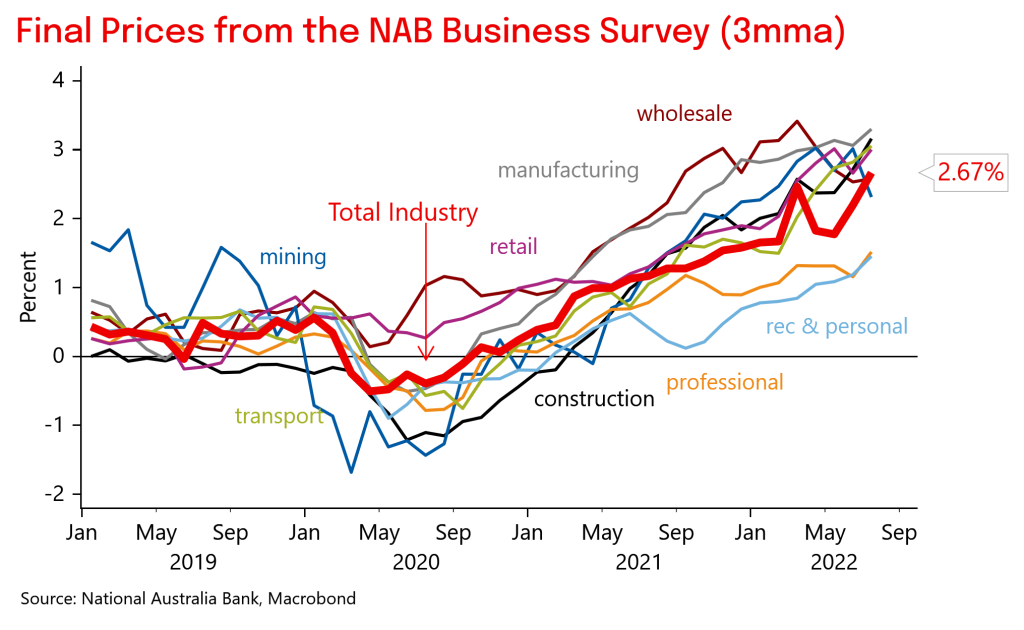

Looking at purchase costs and final product prices by industry reveals some interesting trends, as well as highlighting the broadening of inflation pressures across the economy from goods to services. (Note the broadening to services is being watched closely by the RBA given it is more sensitive to domestic labour costs):

Pandemic-related cost pressures first emerged in the manufacturing and wholesale sectors, and later in construction. These pressures at first reflected disruptions to global supply chains as unexpectedly strong goods demand faced into constrained supply amid COVID-health measures and limited services consumption opportunities and unprecedented stimulus.

Higher ‘upstream’ costs were passed on, reflected in the final product series in the NAB survey. At first, final product price rises were concentrated in manufacturing, wholesale and construction and did not immediately flow through to CPI.

From mid-2021 higher ‘upstream’ costs for goods flowed through to retailers who were able to pass on higher costs to consumers. This was initially seen in the CPI in the market goods category in H2 2021. Housing construction costs also rose strongly, and lifted CPI given its high weight.

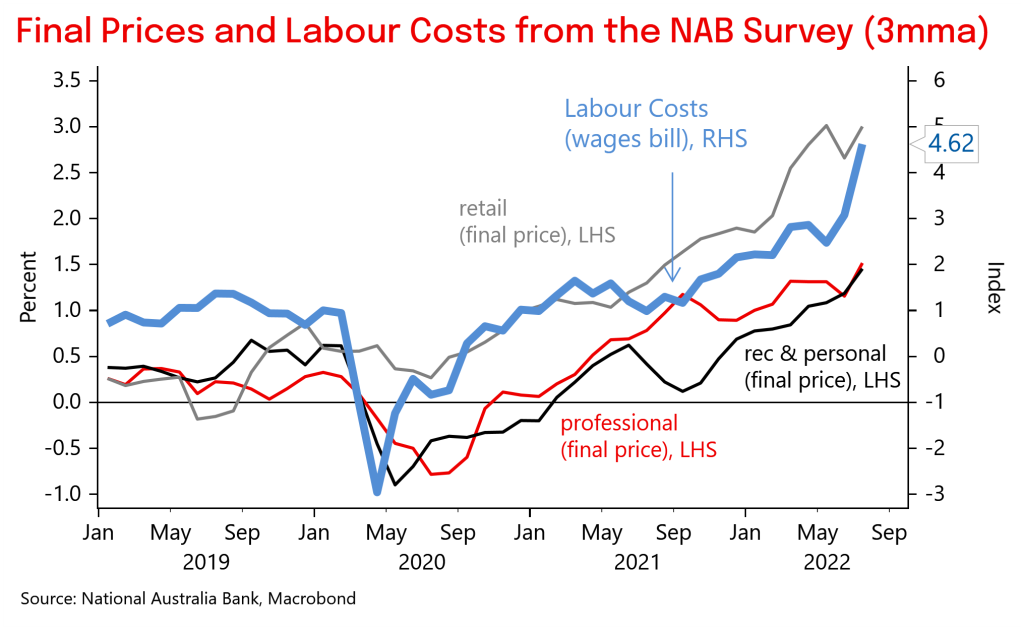

More recently, higher goods prices and increasing labour costs have begun to put pressure on the services sector with a notable lift in final product prices for recreation & personal services and professional services from Q1 2022. Inflation pressures have broadened across the economy alongside capacity constraints.

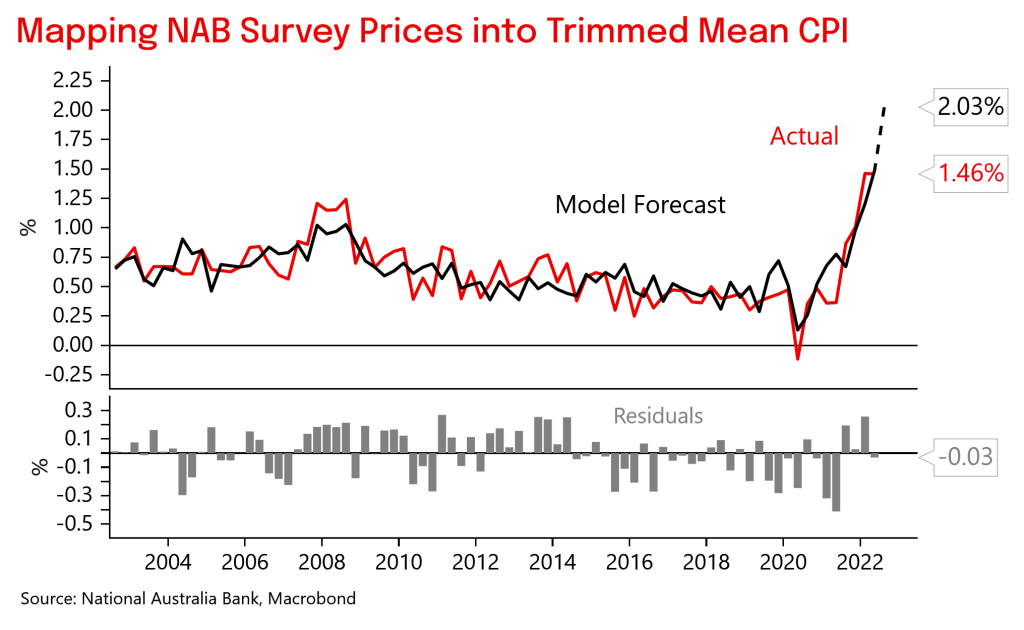

To help inform our view of CPI we have created a simple mapping equation from final product prices in certain industries in the survey to the RBA’s preferred trimmed mean measure. Depending on the assumption used for Q3 it suggests trimmed mean CPI could print anywhere from 1.5-2.0% q/q. If we assumed the inflation pressure seen in July continued in August and September, that would imply 2.0% q/q. If we assumed some volatility in the survey and some retracement, that would still point to 1.5%. Note for Q2 our mapping implied a 1.6% print, and trimmed mean CPI came in at 1.5%.

When should we expect some alleviation in price pressure? Offshore business surveys are suggesting inflation pressures are easing (from elevated levels). This aligns with some easing of global supply chain disruptions, easing in freight rates, and oil prices falling back from their highs. At turning points, Australia generally lags these trends by 4-5 months. Outside of these global influences, the labour market remains tight with the RBA likely to continue to hike rates into mildly restrictive territory.

Chart 1: Price indications from the NAB Business Survey have lifted strongly

Chart 2: Final prices for consumer sectors lifted from 2021

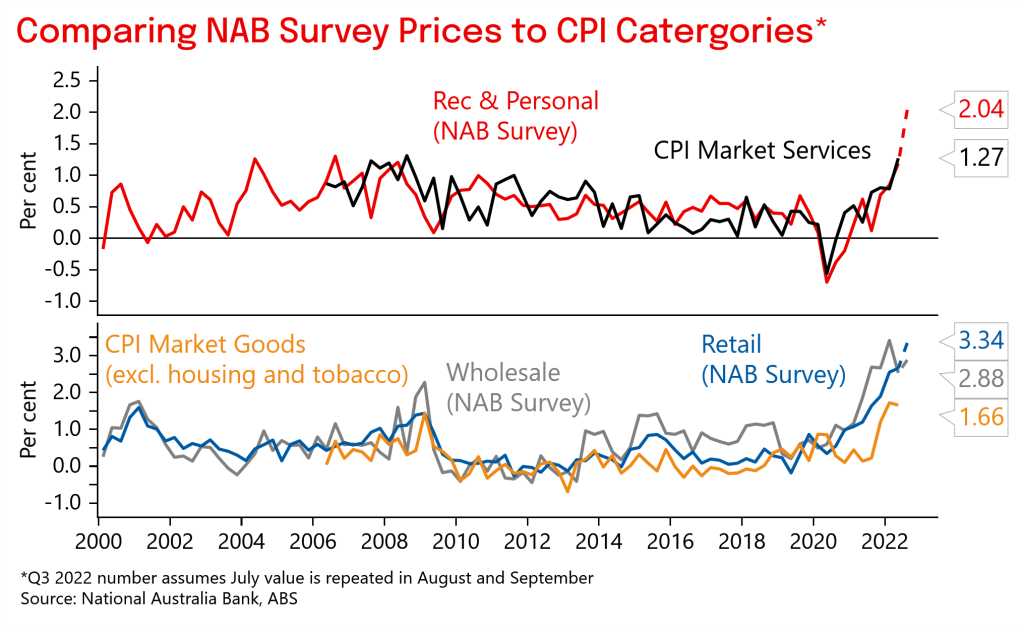

Chart 3: Certain industry final prices map well into CPI

Chart 4: Mapping NAB Business Survey prices to CPI point to another very strong CPI print

Chart 5: Final prices also correlated with the lift in labour costs

Chart 6: Upstream price pressures look to be easing globally and is likely to be seen in Australia with a lag based on historical relationships

Authors:

Brody Viney

Senior Economist

Group Economics

National Australia Bank Limited