NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

With markets having aggressively pushed Fed pricing into 2022, it is likely there is some thought that such a tightening will weigh on demand earlier.

https://soundcloud.com/user-291029717/wages-fuel-supply-chains-and-a-not-so-transitory-inflation-number?in=user-291029717/sets/the-morning-call

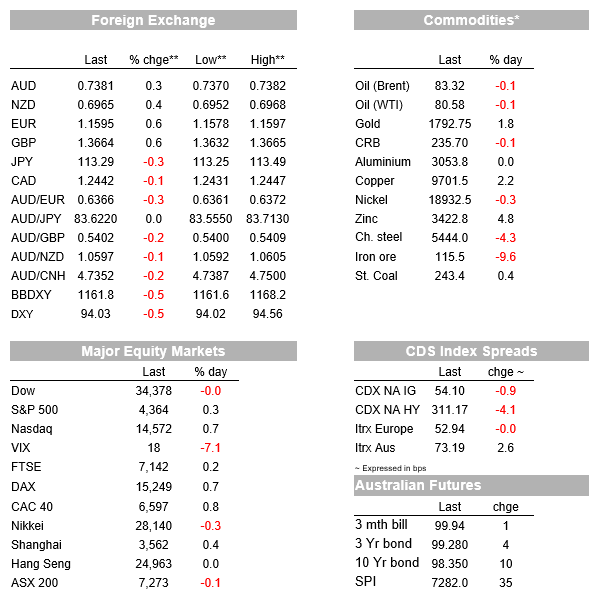

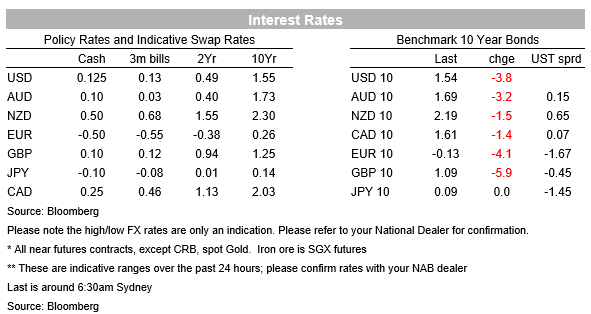

Yield curves flattened again overnight with the US 10yr yield down and the 2yr yield up. The 2s/10s curve fell 5.2bps to 118.2 and the 5s30s was also down a similar 5.6bps to 96.2 and is around the lowest level in two years. The move lower in the 10yr year yield was driven by the real yield which fell 6.7bps to -0.99%, while the 10yr implied inflation breakeven rose 3.1bps to 2.52%. With markets having aggressively pushed Fed pricing into 2022, it is likely there is some thought that such a tightening will weigh on demand earlier as well as the possibility of the Fed overdoing the hiking cycle. There was little reaction within rates to the US CPI release which was close to expectations (Core CPI 0.2% m/m vs. 0.2% expected), nor to the FOMC Minutes which pointed to a November taper announcement with actual tapering to occur from either mid-November or mid-December. As for the taper profile, the Minutes discussed a simple $15bn a month taper comprising $10bn Treasury and $5bn MBS ending in mid-2022 which participants generally endorsed as a template.

Equity markets were modestly higher in Europe (Eurostoxx50 +0.7%) while the S&P500 flipped between green and red to finish up 0.3%. The Q3 profit reporting season kicked off in the US with JP Morgan reporting and beating expectations at $3.74 per share against $3 expected, but seemingly underwhelming with its stock down -2.7%; financials underperformed given the flatter curve. Much of the beat came from lower loan loss provisions after the bank released $2.1bn in reserves (boosting earning by $0.52 a share and another boost came from a tax benefit worth $0.19 a share). Analysts noted with the Bank having released most of its reserves as well as exhausting tax benefits, earning will come from core activities where a flatter yield curve is generally seen as a headwind for banks. Tech stocks which are seen to benefit from low yields rose with the NASDAQ up 0.7%. The big names for the rest of this week in terms of reporting are BofA, Morgan Stanley and Citigroup on Thursday, followed by Goldmans on Friday.

In FX the USD took a breather with the DXY down some -0.5% after it hit a 12 month high the prior night. USD weakness has been broad-based, with losses against all the G10 currencies, despite the (slight) pickup in Fed rate hike expectations. Gains were led by EUR and GBP, both up 0.6%, while notably YEN underperformed with USD/Yen -0.3% and continues to sit above the 113 levels and near its highest levels since late 2018. The EU-UK standoff over the Northern Ireland Border does not appear to have yet impacted. Overnight the EU made an offer to reduce border checks on a wide range of goods going from the UK to Northern Ireland, however, Prime Minister Johnson’s government continues to push for a full renegotiation of the protocol. As for the AUD and NZD, they are both up around 0.3-0.4% with USD weakness being the main driver.

As for data, the FOMC Minutes and the US CPI figures were the focal point for markets, but on both counts were broadly as expected with little market reaction. The FOMC Minutes highlight that a November taper announcement is likely with tapering to being in either mid-November or mid-December. An example taper profile of $15bn a month made up of $10bn in Treasuries and $5bn in MBS was broadly endorsed as a framework with tapering to end by mid-2022 – relevant quotes were: “ a gradual tapering process that concluded around the middle of next year would likely be appropriate. Participants noted that if a decision to begin tapering purchases occurred at the next meeting, the process of tapering could commence with the monthly purchase calendars beginning in either mid-November or mid-December”.

As for the illustrative taper path: “The path featured monthly reductions in the pace of asset purchases, by $10 billion in the case of Treasury securities and $5 billion in the case of agency mortgage-backed securities (MBS). Participants generally commented that the illustrative path provided a straightforward and appropriate template that policymakers might follow… ”. The path finishing by mid-2022 is significant and opens the way to rate hikes in 2022 as the market is pricing and as the FOMC dot plot showed with participants split on a 2022 rate hike at 9 v. 9. Within the Minutes there was some discussion on the outlook for inflation with most of the risks seemingly pointing to the upside (“upside risks cited included the possibility that elevated levels of inflation would continue for longer than expected, especially if labor and other supply shortages proved more persistent than currently anticipated, or that longer-term inflation expectations might move above levels consistent with the Committee’s longer-term inflation objective of 2 percent.”). See FOMC Minutes for details.

As for the US CPI, Core CPI came in line with expectations at 0.2% m/m, while Headline CPI beat by a tenth at 0.4% m/m against 0.3% expected. Falls in used car prices (-0.7% m/m) and airfares (–6.4% m/m) offset higher rental inflation (+0.4% m/m) in the core category. The ‘shelter’ category, which covers rents and so-called owners’ equivalent rent and which has a hefty ~40% weighting in core inflation, is now running at an annual rate above 3%. Should the higher trend in rental inflation be sustained, then core inflation could lift with inflation pressures no longer entirely being in the “transitory” category. Reinforcing this message, other measures of core inflation were also higher, with median CPI moving up to 2.8% y/y while the trimmed mean measure, which cuts off outliers at both ends of the price spectrum, is now up to 3.5%, near its highest level since the early 1990s. Even renowned economist Paul Krugman, who has been fighting the “transitory” corner all year, acknowledged the broadening in inflationary pressures and bigger labour supply issues. It is no surprise then to see markets bringing forward hike expectations.

In other economic data, Chinese credit growth (so-called ‘aggregate financing’) was lower than expected in September amidst signs of a slowdown in the real estate sector as Evergrande teeters on the brink of default. The market remains wary about the Chinese growth outlook given risks to the real estate sector as well as the ongoing energy crisis in the country.

Finally in Australia, yesterday’s consumer sentiment figures pointed to activity lifting sharply as re-opening occurs in NSW, VIC and the ACT. Although headline consumer sentiment fell 1.5% m/m in October, sentiment lifted in Sydney (+1.2%) and Melbourne (+3.9%) ahead of re-opening with the fall in headline sentiment driven by regional areas. Unemployment expectations also fell a sharp 11.1% to the lowest levels since pre lockdown May 2021 which then was pointing to the unemployment rate falling sharply over the next six months. With unemployment expectations back to pre-lockdown levels, this suggests consumers expect a swift rebound in the labour market with the unemployment rate likely to resume its pre-lockdown trend relatively quickly. Interestingly there was also a sharp deterioration in dwelling sentiment which fell 13.8% to its lowest since April 2020. APRA’s macro-prudential tightening occurred mid-way during the survey week.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Read our NAB Markets Research disclaimer

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.