On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

Ahead of the all-important US CPI release tonight, US equities edged higher again overnight while the UST curve flattened driven by an uptick in front end yields. The USD is broadly weaker, but the AUD has been unable to perform.

Events Round-Up

AU: Westpac Consumer Conf Index, Jul: 81.2 vs. 79.2 prev.

AU: NAB Business Conditions, Jun: 9 vs 8 prev.

UK: ILO Unemployment Rate 3Mths, May: 4.0 vs. 3.8 exp.

CH: Agg Fin. ¥4.2trn vs ¥3.1 trn exp and 1.56tn prev.

CH: New Loans ¥3.05trn vs ¥2.3trn exp and ¥1.36trn prev,

GE: ZEW Survey Expectations, Jul: -14.7 vs. -10.6 exp.

US: NFIB Small Business Optimism, Jun: 91.0 vs. 89.9 exp.

Ahead of the all-important US CPI release tonight, US equities have edged higher again while the UST curve has flattened driven by an uptick in front end yields. The USD is broadly weaker, but the AUD has been unable to perform while GBP is stronger with solid wages growth data cementing expectations for a 50bps BoE hike. China Credit data beat expectations, however, details underwhelm.

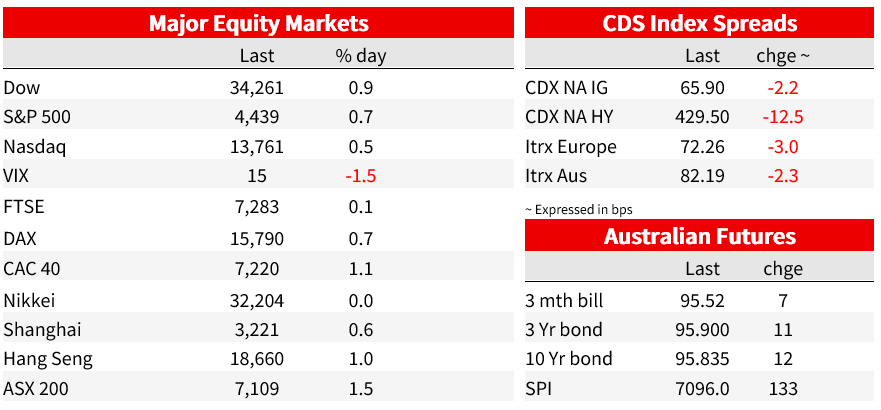

The S&P 500 closed the day 0.67% higher and the NASDAQ ended +0.55%. All 11 main S&P 500 sectors ended in the green with Energy and Utilities at the top of the performance table, up 2.2% and 1.24%. Helping Energy’s performance oil prices extended their recent gains supported by news of a drop in Russian output. According to Bloomberg, crude shipments through Russia’s western ports in the four weeks to July 9 dropped substantially below their average February level for the first time, after volumes surged during the intervening months. On company news, Buffett’s Berkshire Hathaway Energy agreed to buy Dominion Energy stake in a Maryland liquefied natural gas export project for $3.3bn while Microsoft won a court approval to move ahead with its $69bn deal to buy Activision Blizzard.

Earlier in the session the Stoxxx Europe 600 index closed 0.72% higher, notwithstanding another soft German survey. Following the weak Eurozone Sentix index of investor confidence earlier in the week, Germany’s ZEW index fell to -14.7 in July, from -8.5 in June, raising concerns about how durable Germany’s economic recovery will be. The ECB’s restrictive policy stance coupled with weaker global demand represent headwinds. German bund yields were little changed with the 10-year at 2.64%.

The NFIB was the only notable US data release overnight and it was yet another US economic release that beat expectations. The June NFIB index of small business optimism rose to 91.0 from 89.4, above the consensus, 89.9. The index has a notable sensitivity to US equity market’s performance and June was a good month for US equities. Overall sub-indices levels remain subdued, but details in the survey were encouraging with improvements in the general economic outlook, earnings trends, and expected sales.

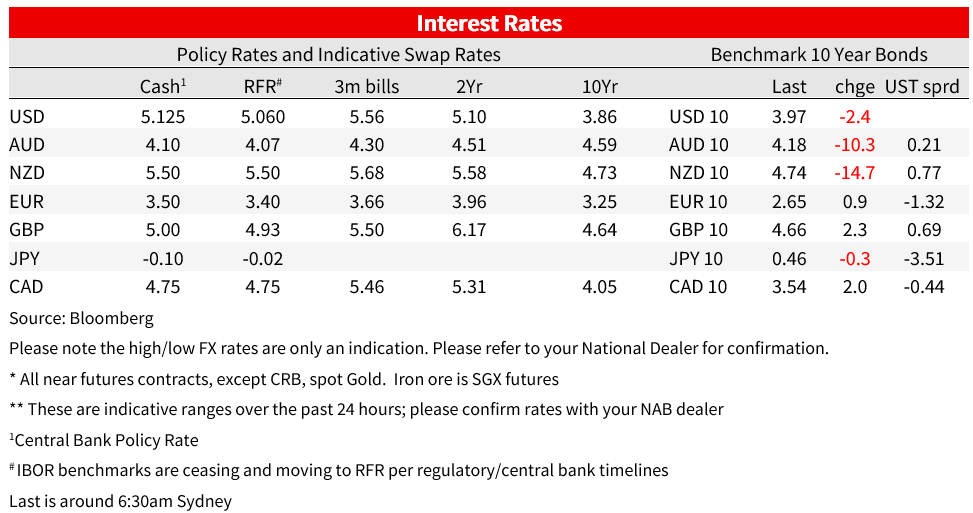

The UST curve flattened overnight with front end yields ticking a bit higher notwithstanding a solid 3y auction. The $40bn auction of 3-year Notes recorded a 2.88 bid-to-cover ratio compared to a 2.69 average ratio from the previous six auctions, stopping 0.2bp through the WI yield. The 2y Note ended the day 3bps higher at 4.894% while movements further out the curve were more subdued. The 10y Note now trades at 3.97%, 1.6bps lower compared to levels this time yesterday.

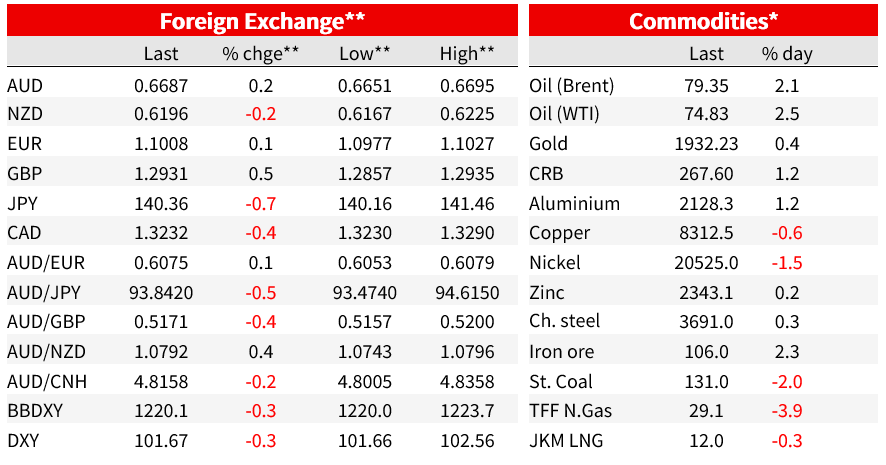

The USD lost a little bit of altitude again over the past 24 hours with JPY and European currencies outperforming while commodity linked currencies were mixed with the AUD little changed. JPY is up another 0.67% with USD/JPY now trading at ¥140.33 with the move lower in 10y UST yields (now sub 4%) the main driver. NOK has extended yesterday’s gains, up another 1% aided by higher oil prices and an increase in Norges Bank rate hike expectation. SEK (+0.88%) and CHF (+0.66%) are also higher while the euro is little changed, but still above 1.10 (1.1002 as I type).

GBP was the other mover overnight, up 0.5% and looking more comfortable above the 1.29 mark (now at 1.2933). Late yesterday the UK labour market data revealed strong wage growth with average weekly earnings excluding bonuses rising 7.3% firming expectations for a 50bps rate hike by the Bank of England (BOE) in early August. The unemployment rate was 0.2% higher than consensus expectations printing 4.0%.

Yet again the AUD has been unable to perform despite of the softer USD tone. The lack of RBA urgency to hike has been an ongoing AUD headwind while concerns over China’s economic outlook has been the other. On the latter, it is interesting to note the AUD (and CNH for that matter) showed little reaction to yesterday’s better than expected China loan and financing data as well as news of further support for China’s beleaguered property sector.

After late Monday’s announcement of a China loan relief plan for developers aimed at ensuring the delivery of homes that are under construction. Yesterday state-run financial newspapers reported the prospect of more property supportive policies, along with measures to boost business confidence. Late yesterday China credit and loan data also beat expectations. Aggregate financing, a broad measure of credit, was ¥4.2 trn well above the ¥.3.1trn expected by consensus. New loans data also beat, printing at ¥3,050bn vs ¥1,900bn forecast. That said, while better than expected is worth noting that bank loan growth still fell to its lowest in five months in June, while broad credit growth dropped to a record low.

Overall. China’s data and news flow along with market reaction highlight Beijing challenge, against a backdrop anaemic demand given a cautious Consumer and private investors, a meaningful fiscal spending announcement is what is needed for market to become more positive on China. Until then USD/CNY is unlikely to head sub 7 and the AUD/USD will struggle to head back above 70c.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

Firmer consumer and steady outlook

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.