NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

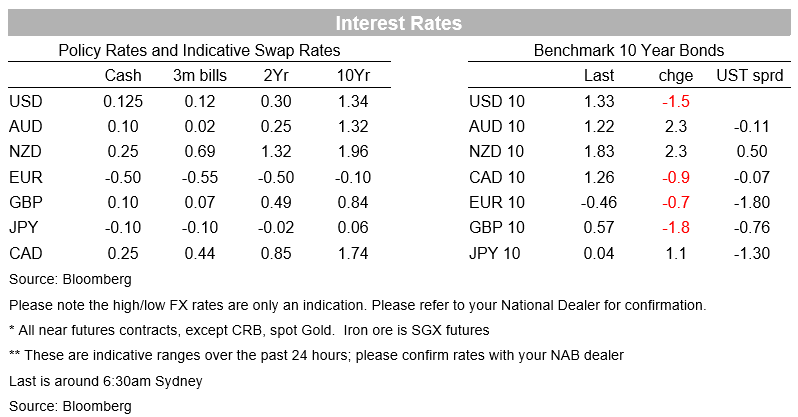

US inflation moderates, taking the pressure down a notch and playing into the Fed’s transitory narrative. It’s no surprise to see yields and the USD lower in the wake. The US 10yr fell 1.5bps to 1.33%, though CPI was the catalyst for a larger fall after it reached an intra-day high of 1.3743%.

https://soundcloud.com/user-291029717/inflation-the-way-the-fed-wanted-it?in=user-291029717/sets/the-morning-call

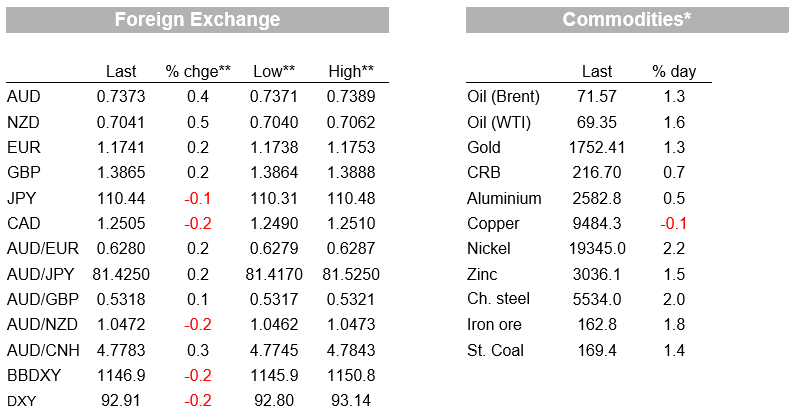

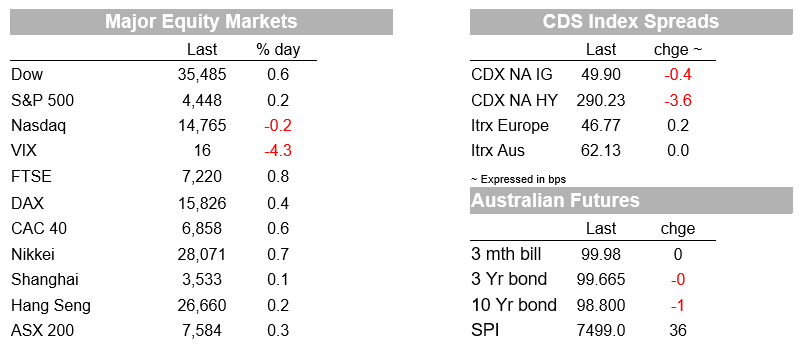

US inflation moderates, taking the pressure down a notch and playing into the Fed’s transitory narrative. It’s no surprise then to see yields and the USD lower in the wake. The US 10yr fell 1.5bps to 1.33%, though CPI was the catalyst for a larger fall after it reached an intra-day high of 1.3743%. Soon after the CPI figures, a strong 10yr bond auction for $41bn also saw yields fall intraday to 1.30% with indirect-bidder demand at 77.2%, a proxy for foreign demand the highest on record, and seeing primarily dealers scrambling for bonds. Alongside the fall in yields the USD fell 0.2% with broad-based falls against most pairs with EUR +0.2%, GBP +0.2% and USD/Yen -0.1%. Commodity linked currencies rose with the AUD (+0.4%) and NZD (+0.5%) outperforming with most commodities lifting (Brent 1.3%). Equities lifted with the S&P500 +0.2% to another record high. Easing inflation pressures plays to the Fed’s transitory narrative and likely means the Fed won’t feel the need to aggressively tighten policy, which was starting to shape up as a risk.

First to the US CPI report. After a string of upward surprises, core inflation moderated in July at 0.3% m/m vs. 0.4% expected and 0.9% previously (the annual rate was 4.3% y/y). There was much less price pressure from the “re-opening” components that have driven the recent sharp rise in inflation with used cars +0.2% m/m (after 10.2% last month), airline fares -0.1% m/m (after 2.7% last month), though lodging away from home still rose strongly at 6.0% m/m (after 7.0% last month). Much of the re-opening pressure has now abated with lodging away from home and airfare prices back to their pre-pandemic levels, while used car values which leads used car prices have dipped for two consecutive months according to Manheim (see Manheim for details ). The WSJ journal also notes that US carrier Southwest Airlines has seen a slowdown in bookings and rise in trip cancellations this month, which may also have the potential to ease some travel and accommodation price pressures.

Fed speak has been very heavy over the past couple of days, reinforcing that we should expect a taper announcement at an upcoming Fed meeting (September, November or December). The Fed’s George, a known hawk and a 2022 voter, argued for reducing policy stimulus now: “today’s tight economy…certainly does not call for a tight monetary policy, but it does signal that the time has come to dial back the settings” and that “I support bringing asset purchases to an end under these condition”. The Fed’s Kaplan also again argued for a tapering announcement to occur at September and actual tapering to occur in October (“It would be my view that if the economy unfolds between now and our September meeting…if it unfolds the way I expect, I would be in favour of announcing a plan at the September meeting and beginning tapering in October,”). Barkin was more moderate, but even he said “we will get there in the next few months”.

With tapering likely, market focus will shift to the form of tapering to help inform on the likely rate hike path. While no details of that were given yesterday, Bullard said yesterday he was in favour of a relatively quick tapering profile that ended in March 2022, with Bostic also this week in favour of a relatively fast tapering profile. Should such an implied taper profile be realised, then the possibility of rate hikes in H2 2022 is very real. While it is tempting to discount the hawkish voices in the FOMC, it is worth noting that in 2022 the Fed tilts hawkish with all four rotating Fed presidents coming from the hawkish side (Bullard, Mester, Rosengren, George), while at least one Governor (Waller) is also hawkish, meaning 5/11 voting FOMC members in 2022 will be leaning hawkish. The next two key events for the bond market to focus on will be Fed Chair Powell’s keynote speech at the Jackson Hole symposium later this month and the next payrolls report early September.

In other news, China’s Aggregate Financing Figures was weaker than expected, as previously flagged by China’s Securities Journal on Friday. Aggregate Financing was 1060 vs. 1700 expected, while credit growth overall was its slowest since February 2020 at 10.7% y/y. The Securities Journal piece hinted that credit growth would pickup on the back of further easing and it is widely expected the PBoC will ease policy further. Earlier in the week, the PBoC reiterated that it would guide loans to grow “reasonably” and ensure the pace of credit expansion matches nominal economic growth. Also in China, the banking and insurance watchdog is stepping up scrutiny of the nation’s insurance technology platforms, widening the regulatory crackdown that has encompassed technology, education and gaming firms with the potential to impact investor sentiment again.

Finally, the next round of US infrastructure stimulus is slowly progressing after the US Senate passed a $3.5 trillion budget framework , which incorporates a wide range of social policies. The odds of the package passing the House in its current form are small, with a number of Democrats opposed to many facets of the package and this is likely to be another drawn out process. Meanwhile oil prices dipped after the White House called on OPEC to boost oil production, saying that the cartel’s planned supply increases would not fully offset previous production cuts. Brent crude fell by nearly $2 to just above USD69, but has since more than recovered, now up closer to USD71.50, up 1.3% for the day.

A very quiet day ahead with only UK Q2 GDP of note. Elsewhere Europe has Industrial Production and the US the usual Jobless Claims and PPI. Details below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.