NAB specialists and clients from across the bank’s Fund Sponsors, Strategic Investors and Alternative Assets (FSA) business gathered over lunch recently to share career stories and advice on promoting greater diversity and inclusion.

After having moved briefly into bear market territory the previous Friday, last Friday saw the S&P500 up by its largest weekly gain so far this year.

https://soundcloud.com/user-291029717/a-piggy-bank-backed-recovery?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

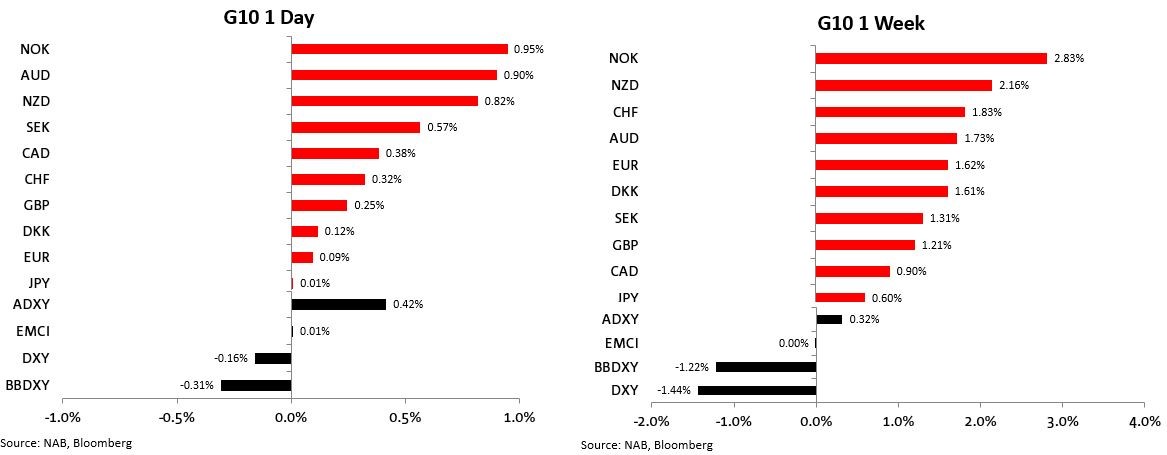

After having moved briefly into bear market territory the previous Friday, last Friday saw the S&P500 up by 2.5% to bring the rise for the week to a 6.6% – its largest weekly gain so far this year. US PCE inflation data no higher than expected, and Personal Spending figures no lower than expected, proved to be a risk-friendly combination that helped keep the nascent equity rally running in conjunction with some easing in US recession fears. Together with further minor slippage in longer dated Treasury yields, downward pressure on the US dollar was maintained to leave the DXY 1.4% weaker on the week. The flipside of which was AUD/USD adding another 0.8% for a 1.7% weekly gain, to its best level since May 5.

The coming week will see market activity curtailed by the US Memorial Day holiday on Monday and the two-day UK holiday on Thursday and Friday for the Queen’s platinum jubilee, but it is an important one for data, including latest China PMIs, US ISMs and payrolls, plus Australia Q1 GDP.

There were no surprises in Friday’s various US economic data release, but that in itself was interpreted favourably by equity market investors. In particular, markets liked the April core PCE deflator coming in at 0.3% on the month , the third successive 0.3% print (at least to one decimal place – March was 0.33% and April 0.34%). Falls were seen, in particular, in used car and apparel prices. This puts the annualised rate in the three months to April at 4.3%, the lowest in six months and off a peak of 6.3%. Core PCE deflator base effects should remain favourable in both May and June, given rises of 0.6% and 0.5% in May and June 2021 respectively.

Markets also chose to like the fact that Personal Consumption Expenditure rose by 0.9% in nominal terms (0.8% expected) and by 0.7% in real terms (as expected) . With Personal Income only up 0.4%, households are continuing to draw down savings to maintain spending, indeed the Household savings rate of 4.4% is now the lowest since 2008, but the stock of ‘excess’ savings accumulated during the pandemic thanks to large fiscal transfers combined with an inability spend on services are still huge at $2.2tn. This is more than 10% of GDP and suggests that if there is to be a significant slowdown in the US economy or outright recession, it is unlikely to be this year.

The disconnect between what US conumers say and what they do remains stark, the final May University of Michigan Consumer Sentiment Index lowered io 58.4 from the preliminary 59.1 – a new post-March 2009 low. The 5-10 year Inflation Expectations read stuck at the 3.0% preliminary level.

There were no central bank comments of note on Friday (but plenty to look forward to this week). In Russia/Ukraine news, Bloomberg late Friday reported that some EU leaders are leaning toward a deal that would ban Russian seaborne oil while temporarily sparing deliveries through a key pipeline to give landlocked Hungary more time to reduce its dependence on Russian oil. Bloomberg says EU governments are discussing a plan with the European Council and European Commission that would make shipments of oil through the giant Druzhba pipeline exempt for a limited period of time from a broader ban on oil deliveries to the bloc, according to people familiar the matter.

Meanwhile, the leaders of France and Germany have urged Russia’s Vladimir Putin to hold “direct [and] serious negotiations” with Ukraine’s president, the German chancellor’s office said. Emmanuel Macron and Olaf Scholz spoke to Mr Putin by phone for 80 minutes. The pair “insisted on an immediate ceasefire and a withdrawal of Russian troops”, the chancellor’s office said. Russia’s leader said Moscow was open to resuming dialogue with Kyiv, according to the Kremlin. It did not mention the possibility of direct talks between Mr Putin and his Ukrainian counterpart, Volodymyr Zelensky. The Ukrainian president earlier said he was not “eager” for talks but added they would likely be necessary to end the conflict (BBC reporting).

With all three main US equity indices posting gains in excess of 6% last week led by a 6.8% rise for the NASDAQ, there was clear outperformance versus Europe (Eurostoxx 50 +4.2%) and Australia (ASX200 +0.5%) while China was the worst performing amid ongoing economic malaise due to lockdowns (CSI 300 -1.9%).

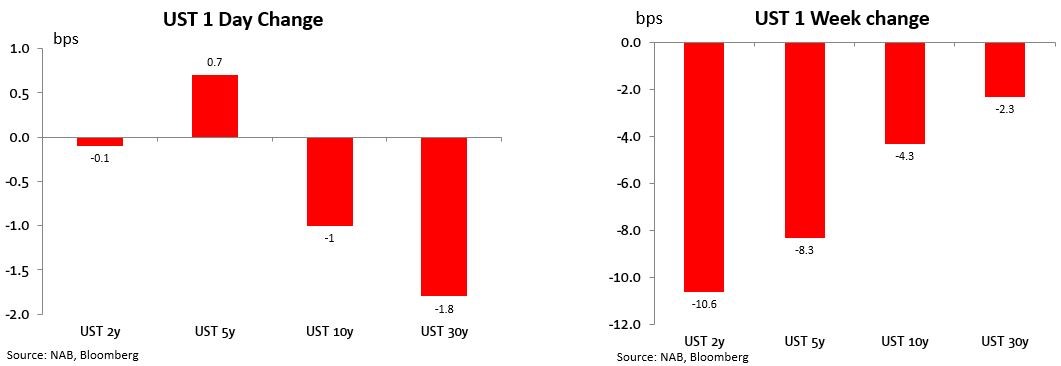

US bonds hardly moved Friday, 2s unchanged and 10s -1bps, but over the week 2s lost 10.6bps and 10s 4.3bps. Hopes, naïve or otherwise, for a pause in the Fed tightening cycle as early as September inspired in part by comments from the Fed’s Bostic on Monday, continue to resonate, having also gained some succour from the subsequent FOMC Minutes. Indeed, over the week, money markets have reduced their pricing for additional Fed rate rises by end-2022 rate from 193bps (pre-Bostic) to 180bps. This though still implies rate rises at every remaining Fed meeting of 2022, including 50bps hikes in both June and July and at least 25bps at each of the remaining three

FX Markets saw the US dollar sell-off continue Friday with gains led by NOK in what was another good day for oil prices and the risk-sensitive AUD and NZD, all up by more than 0.8%. The DXY lost 0.16% to its lowest since 22 April (down 1.4% on the week) and the broader Bloomberg BBDXY index by 0.3% (lowest since 5 April and 1.2% lower on the week). The AUD/USD close of 0.7162 is to its highest since 5 May and means the pair has now retraced more than 38.2% of the entire early-April through mid-May decline. A 50% retracement would be to around 0.7250.

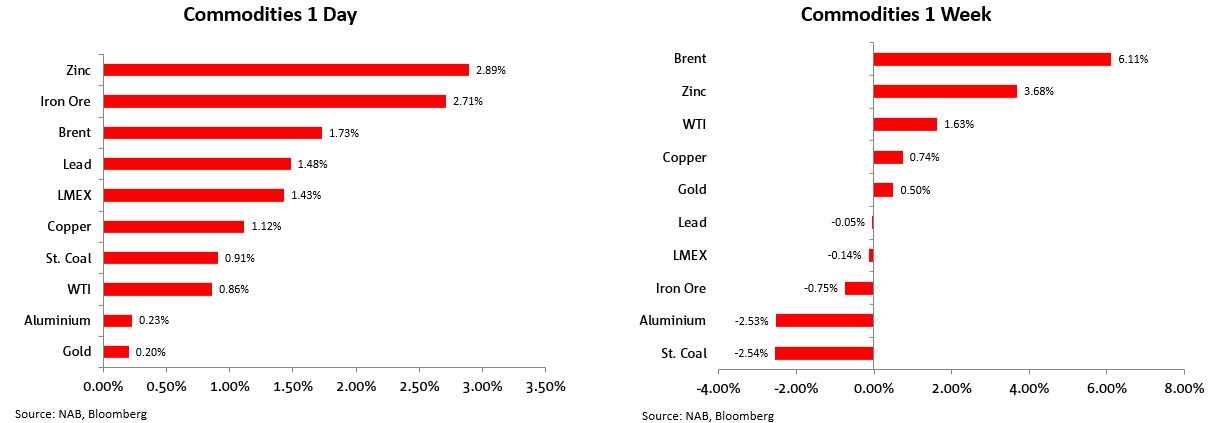

Commodities had a good day across the board Friday led by zinc (2.9%) iron ore (2.7%) and Brent crude (1.7%) though on the week it was a more mixed picture, e.g. iron ore was actually down slightly, aluminium and steaming coal more so, while Brent crude was up more than 6%.

Read our NAB Markets Research disclaimer. For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB specialists and clients from across the bank’s Fund Sponsors, Strategic Investors and Alternative Assets (FSA) business gathered over lunch recently to share career stories and advice on promoting greater diversity and inclusion.

Hybrid issuance is becoming an ever more relevant funding instrument and capital management tool for corporate issuers today, attracting strong investor demand, write Tabitha Chang and Stefan Visser from the NAB Capital Markets Origination team.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.