On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

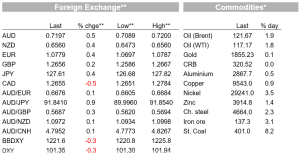

Brent oil recorded its 8-consecutive day of price increases, supported by expectations of a China reopening in addition to the expected EU Russian oil ban.

https://soundcloud.com/user-291029717/german-inflation-concerns-but-equity-markets-refuse-to-freak-out?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

European equities start the new week with a positive tone while US equity futures eke out small gains on Memorial Day. Inflation concerns lift core global bond yields as German inflation prints a new record high and oil prices extend recent gains, US Treasury futures fall implying a 10y UST yield above 2.80%. USD extends decline with commodity linked FX leading the charge, AUD trades to an overnight high of 0.72 and now trades just below the figure.

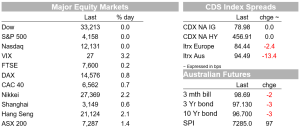

After opening higher, European equities managed to close on the green led by gains in consumer discretionary (+1.96%) and IT sectors (1.5%). European banks also traded with a positive tone after global regulators agreed to start treating the euro area as one market in determining capital requirements for its top lenders (regional banks closed 1.47% higher). The Stoxx 600 index ended day +0.59%, its fourth consecutive day of positive returns. US equities futures followed a similar pattern to European equities, eking out small gains on Memorial Day. The S&P 500 mini closed 0.52% higher while the NASDAQ 100 mini was 1.043%.

Equities showed little concern to rising inflationary pressures. Germany recorded another record high inflation print at 8.7%yoy, surpassing expectations for the headline reading to climb from 7.8% to 8.1%. Energy and food were the main culprit for the larger than expected increase in prices, amping the pressure on the ECB to remove its ultra-easy monetary policy. The Bank meets on June 9, next week Thursday, with the market widely expecting an end to the Bank’s QE programme, the big question is how quickly the Governing Council decides to move away from its negative deposit rate policy (by 25bps or 50bps hikes) and how high it will go before looking to pause. Tonight, we get the Eurozone CPI reading (more below) and after the stronger than expected German inflation numbers, money markets have increased ECB rate hike expectations by 4 bps to 114bps by the end of the year with the deposit rate seen at + 0.557% by the mid December ECB meeting.

Overnight, German Finance Minister Lindner called the fight against inflation his top priority and he reiterated government plans to restore constitutional limits on net borrowing from next year, suggesting that the 2023 finance plan will be “fundamentally different” to recent budgets.

Meanwhile in Brussels, the European Commission is still struggling to find an agreement over a proposed ban on Russian oil imports . The two-day summit still has another day to go and expectations are for a water-down agreement to be reached, although Hungary is still opposing the move. The rising cost of living is making it difficult for EU countries to agree on a ban, a Russian oil ban inevitably implies a cost for EU countries with Russia retaliation also a concern.

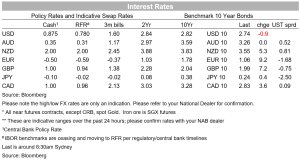

European rates surged higher as the state-by-state German inflation data were released, seeing Germany’s 2-year rate up 11bps on the day to 0.43% and the 10-year rate up 9bps to 1.05%. Other European rates show similar increases. The UST market was closed overnight as the US commemorates Memorial Day, but UST Futures traded during the European session with the decline in price implying a move in 10y UST yields above 2.80%.

Sticking with the inflation dynamics, Fed Governor Waller was speaking overnight and true to his hawkish form he said that he supported more 50bps hikes “for several meetings” and not taking these off the table until “I see inflation coming down closer to our 2% target”. He supported a policy rate above neutral by the end of this year, and he said his plan for hikes was roughly in line with market pricing, which sees the Fed Funds rate at about 2.75% in December.

Oil prices have extended their recent rise, with Brent oil recording its 8-consecutive day of price increases, up 1.9% over the past 24 hours to $121.67 . In addition to the expected EU Russian oil ban, oil prices have been supported by expectations of a China reopening. China reported the fewest new Covid-19 cases in almost three months, only 122 cases were reported across the country on Sunday, the fewest since March 3. The decline in cases supports the authorities’ intentions to relax some of the restriction imposed, specially in Shanghai and Beijing. Tomorrow, Shanghai will lift lockdown measures for residents in low-risk areas, allowing them to leave and enter their compounds freely with bus and subway services scheduled to reopen in an orderly manner. Good news, but China’s reopening strategy is only gradual and still very much susceptible to a new virus outbreak. Omicron is very infectious and until China finds a solution to it vaccine dilemma, the risk of new lockdowns will remain elevated.

Moving onto currencies, the USD has extended its decline, down for a third day in a row (~0.31%) in both BBDXY and DXY measures . Commodity linked currencies have been the outperformers over the past 24 hours with NOK at the top of the leader board, +0.74% with the AUD extending its gains overnight (0.5%), briefly trading at 72c before easing a few pips, the aussie now trades at 0.7196. The NZD has pushed up to about 0.6560, up 0.4% from Friday’s close, but not much progress from yesterday’s NZ close, now at 0.6554. The strong German CPI data helped fuel further gains in the euro, the union currency gained 0.5% from last week’s close and now trades at to 1.0779, while the risk-on backdrop with higher global rates has seen JPY the weakest performer, with USD/JPY up 0.3% to 127.60.

Coming Up

Read our NAB Markets Research disclaimer. For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

Firmer consumer and steady outlook

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.